Balancer DeFi Protocol: BAL, AMMs, V3 and the Shutdown

Balancer was one of the most architecturally ambitious automated market makers in DeFi. Four of the most respected security firms in the industry audited it: OpenZeppelin, Trail of Bits, Certora, and ABDK. A single November weekend still wiped out $128M and ended the corporate entity behind the protocol. The protocol still trades, technically, because the contracts are immutable and live on-chain. What follows is the story most outside-DeFi coverage of "another crypto hack" missed: what Balancer actually was, why V3 was supposed to be different, how the V2 Composable Stable Pools broke, and what it means for BAL holders and liquidity providers now that the labs running development have wound down.

What Balancer Was: AMMs, Liquidity Pools, and Portfolios

Balancer is one of the more architecturally distinct projects in the DeFi space. The pitch was never "another Uniswap." It was closer to "Vanguard for modern DeFi." Fernando Martinelli and Mike McDonald launched the V1 protocol in March 2020 with an unusual proposition. It was a decentralized exchange built around automated index-style portfolios. The AMM kept asset weights at their target ratios through arbitrage trades on existing pools, rather than through a fund manager rebalancing every quarter. Any user could provide liquidity, contribute liquidity to a pool, or simply use the protocol to swap tokens. If a pool was 60% ETH, 20% WBTC, 20% USDC and ETH ran 30% in a week, arbitrageurs would sell ETH into the pool until weights restored. The LP earned trading fees instead of paying management fees. That was the original Balancer insight, and most of the technical complexity flowed from it.

The pool architecture allowed up to eight tokens per pool with custom weights: 50/50, 80/20, 25/25/25/25, anything that summed to one. Mathematically the invariant was a generalization of the constant product formula (xy = k) to a geometric mean across N assets. From there the team built outward across pool types. Weighted pools came first, then smart pools, stable pools tuned for like-priced assets, and composable stable pools that nested LP tokens. Boosted pools earned yield from idle deposits in Aave. Managed pools allowed delegated parameter control. Liquidity bootstrapping pools (LBPs) handled token launches. Common pairings included WETH, DAI, USDC and yield-bearing assets like wstETH and osETH. Slippage on small swaps in weighted pools tracks closely with concentrated-liquidity DEXs because the same number of assets distributed across more tokens still routes well through Balancer's path optimizer.

Balancer is one of the few liquidity protocols on Ethereum blockchain where total value locked across pools is routed through smart contracts rather than centralized order books, with LP token balances tracked on-chain via a single-vault dapp interface. LPs earn fees in proportion to their share of the pool, and pool profitability depends more on volume than on emissions.

LBPs turned out to be a real moat. Copper Launch and later Fjord Foundry built their entire fair-launch businesses on top of Balancer, raising a cumulative $750M+ for projects with the dutch-auction-style price discovery LBPs enable. Long after the headline TVL numbers stopped favoring Balancer, LBPs continued to bring fees in. The pool architecture was the technical achievement; LBPs were the durable product.

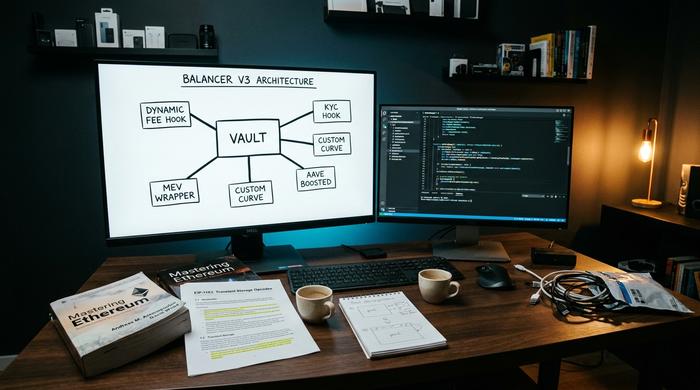

Balancer V3: Hooks and Programmable Liquidity Pools

V3 was the architectural rethink. It launched on December 11, 2024 with an Aave integration ready at day one and a single core thesis: V2's monolithic vault could not keep up with how fast AMM design was evolving. Move custom logic out of pool contracts and into hooks, the V3 team argued, and third parties can extend the protocol without waiting on a Balancer Labs release cycle. The architecture mirrored what Uniswap V4 hooks shipped around the same window, with each project arguing it got there first.

In practice, V3 hooks let pool creators wire in things V2 could never support cleanly: dynamic swap fee logic that responds to volatility, custom curves for specific asset pairs, KYC layers for permissioned pools, MEV-protection wrappers. Transient accounting via EIP-1153 made multi-step flows in a single transaction cheaper. The 100x developer-onboarding ergonomics target was marketing language, but the underlying point, that V2's complexity had become a moat against new pool types, was real. V3 is fully permissionless: anyone can add liquidity, deploy a pool, or build on top, and pool managers retain meaningful control over parameters. The result aimed to streamline how new AMM designs reach mainnet on Ethereum and beyond, and to optimize the developer-facing surface that V2 made painful.

By May 2026, V3 TVL had reached $70.3M, with 7-day volume of $161.5M and annualized fees around $3.17M. V2 still held $34.3M and produced roughly $2.91M in fees. Combined Balancer TVL of about $104M put the protocol at roughly 1/32nd the size of Uniswap, which sat around $3.3 to $3.5B at the same time. V3 was live across seven chains including a $14.7M deployment on Monad. By the standards of a brand-new architecture launching into a slow market, V3 was working. By the standards of a top-tier AMM, it was small.

BAL Token, veBAL Governance, and Liquidity Provision

The Balancer token (BAL) was meant to be DeFi's version of equity, protocol ownership distributed to liquidity providers through emissions rather than to outside investors through a sale. Hold BAL tokens, vote on governance, accrue a share of the fees the protocol generated. Lock them as 80/20 BAL/WETH BPT for up to a year and you got veBAL, the Curve-inspired vote-escrowed version with boosted yields and gauge voting power over where future emissions flowed. The governance vote process ran through Snapshot, with veBAL holders carrying most of the weight.

The math worked on paper. In practice, BAL collapsed. Maximum supply is 96.15M, circulating supply 69.79M (72.58%). The May 2026 price sits at $0.148, market cap roughly $10.37M, 24-hour volume $1.33M, market-cap-to-TVL ratio around 0.091, extremely depressed by any DeFi yardstick. Against the May 2021 all-time high of $74.77, BAL is down 99.8%. Aura Finance, the veBAL aggregator that ran much of the gauge-war infrastructure, still holds about $32.1M in Ethereum TVL but is operating in a smaller and smaller pond.

Pre-shutdown emissions ran at roughly 3.78M BAL per year. The March 2026 governance proposal cut that to zero and redirected a $3.6M treasury chunk into a BAL buyback. Holders read it correctly: the era of BAL as an emissions-driven yield asset had ended.

The $128M Vulnerability: Inside the Balancer Hack

The hack is the central event in the Balancer story. On November 3, 2025, an attacker drained $128.64M from Balancer V2 Composable Stable Pools, mostly on Ethereum (about $100M) with additional losses on Base, Polygon, and Arbitrum. BlockSec confirmed the figure within hours. Two forked deployments, Beets on Sonic and Beethoven on Optimism, took collateral damage; at least 27 other Balancer V2 forks were left exposed and unpatched in the immediate aftermath.

The mechanism, stripped of jargon, was an invariant manipulation. Composable Stable Pools track a mathematical invariant, a number that should stay constant during normal trading and only changes when liquidity is added or removed. A rounding bug in how the invariant was recalculated, combined with an access-control gap that let an attacker call a function it should not have been able to call directly, opened the door. The attacker deployed counterfeit tokens crafted to interact with the buggy math, manipulated the pool's view of its own state, and pulled real assets out at a favorable exchange rate. They then spawned new contracts and kept the attack running across multiple chains rather than executing it as a single transaction.

The brutal fact is that Composable Stable Pools were audited by four of the most respected firms in the industry, OpenZeppelin, Trail of Bits, Certora, and ABDK, and the vulnerability still went undetected. Real-time on-chain analytics platforms like Etherscan and DeBank were the first venues where users tracked the exploit; centralized exchanges had no exposure to the underlying smart contracts. Modern DeFi cryptocurrency users browsing via MetaMask through a browser-extension UX saw the same flow that ordinary users did, with no warning until pools were paused. The Balancer team confirmed within hours that V3 was unaffected because it used a different invariant calculation pattern. The wider context was harsh: 2025 year-to-date crypto-hack losses had already crossed $2.2B at the time, and Balancer had its own history (a 2020 STA deflationary-token attack of roughly $520k and an August 2023 incident of about $2.1M) that should have made everyone more paranoid. The number that mattered, in the end, was $128M on a single weekend.

Balancer Labs Shutdown: BAL Tokenomics Reset

Three weeks after the hack, on March 24, 2026, Balancer Labs announced the corporate entity behind the protocol would wind down. CoinDesk and The Defiant carried the announcement; the Labs team confirmed it on the governance forum the same week. The Defiant's coverage focused on the parallel BAL tokenomics proposal that cut emissions to zero and redirected $3.6M into a buyback fund.

The distinction matters more than most readers realize. Balancer Labs, the company, is not Balancer, the protocol. The contracts are immutable code deployed on Ethereum and several other chains; they keep executing swaps as long as someone calls them, with or without an engineering team paid to maintain the front end. What the shutdown actually killed was the dedicated dev funding, the active security response capability, and the marketing apparatus. The protocol entered the same "maintenance mode by community" status that several Curve-adjacent forks have lived in for years.

The reasoning was straightforward enough. BAL price had collapsed; the emissions paid out in BAL were costing the protocol more than they were buying in growth. With the hack damaging trust and TVL bleeding, the math no longer worked. veBAL gauge-vote dynamics remain unresolved as of May 2026, and Aura's role in directing what little BAL still flows is more important than ever, though Aura itself is operating against a shrinking total emissions pool.

Balancer vs Uniswap: Liquidity, Portfolio Pools, Risk

The honest comparison is uncomfortable. Uniswap V4 shipped hooks at roughly the same time Balancer V3 did, and Uniswap went in with about 32 times the TVL. Balancer's differentiation was always pool architecture, weighted pools, custom multi-asset combinations, programmable parameters that Uniswap V2 and V3 never matched. The differentiation was real. It never translated into durable market share.

Where the two diverged most meaningfully: Uniswap V3 introduced concentrated liquidity, letting LPs allocate capital efficiency to specific price ranges; Balancer kept its weighted-pool model, which is easier for portfolio LPs and worse for tight-spread market makers. The Balancer liquidity provider profile skewed toward passive multi-asset allocators rather than active rebalancers. Pool managers can set the swap fee anywhere from 0.0001% to 10%; Uniswap defaults to a small number of fee tiers. Impermanent loss profiles differ accordingly, weighted pools dilute IL across the number of assets, while concentrated positions amplify it. User experience for an average LP on Balancer was historically rougher than on Uniswap, and that gap mattered more than the math. The single-vault efficiency of V2 was technically elegant and conserved gas across composite operations, but never won the volume race. The one Balancer-original product that retained meaningful share was the LBP, still used by Copper Launch and Fjord Foundry. Beyond that, the comparison favored Uniswap.

What This Means for Balancer Liquidity Providers

For an LP holding Balancer positions today, the practical question is what actually changed. Short answer: the contracts still execute, the swaps still settle, but the development pace will slow and the security response will be community-led rather than Labs-led. Aave V3 integration on V3 remains functional. Aura Finance still aggregates veBAL governance and continues to vote on gauges, though over a smaller emissions pool now that the buyback proposal is reshaping economics.

The 27 unfixed Balancer V2 forks remain a contagion-risk surface. Anyone holding meaningful positions on a Balancer fork deployment should treat the same rounding-bug pattern as live until the fork team confirms a patch. BAL holders should expect minimal emission incentives going forward, with treasury redirected toward the $3.6M buyback rather than into LP yield. The Balancer liquidity that remains is more concentrated in a smaller set of pools, and the protocol's voice in the broader DeFi narrative has gone quiet.

What Balancer Leaves Behind for Modern DeFi

Balancer's story is a microcosm of mid-tier DeFi in the 2025-2026 window. Ambitious architecture, four-firm audit history, real product innovation in LBPs, and still a $128M smart-contract failure that ended the corporate sponsor. The protocol survives in zombie mode while V3, on a separate codebase, continues to attract a small but real set of LPs. The era of Balancer-as-Uniswap-challenger ended on a November weekend; what remains is a code repository, a community, and a set of immutable contracts that will execute trades as long as someone keeps paying gas to call them.