FICA Tax Meaning: Federal Insurance Contributions Act 2025 - 2026

Almost every US paycheck has a line called FICA that takes 7.65% of gross pay and offers no obvious explanation of where the money goes. The deduction is automatic, the math is fixed, and most workers never look at it twice. FICA is short for Federal Insurance Contributions, and the money it withholds funds Social Security and Medicare, together, the most successful US anti-poverty program ever built, supporting roughly 67 million Americans every month.

The FICA meaning matters for one practical reason. Understanding the meaning of FICA pays off because it applies to your taxable wages, shows up on every federal payroll, and produces a different total FICA outcome at every income bracket. This guide walks through the federal payroll tax mechanics, plus a wrinkle most explainers skip: how the rules apply when wages are paid in cryptocurrency, when stablecoin payroll providers handle settlement, and when a self-employed crypto freelancer crosses the Additional Medicare Tax threshold with no employer withholding.

How FICA Tax Works: The Federal Insurance Contributions Act

Here is the strange thing about FICA. It is not really a tax, despite what your paystub calls it. FICA is a forced contribution to two federal trust funds, codified at 26 U.S.C. §§ 3101 through 3128. Congress wrote it into the Social Security Act of 1935. Medicare got bolted on through the Social Security Amendments of 1965. The framing has consequences. You cannot deduct FICA on a federal return. You cannot wipe it with tax credits. You cannot get it back if you die before drawing benefits.

Three legally distinct trust funds receive the money. The Old Age and Survivors Insurance trust pays retirement and survivor checks. The Disability Insurance trust covers SSDI. Together they form OASDI, which is what the SSA calls Social Security in its own paperwork. The Hospital Insurance trust funds Medicare Part A. Medicare Parts B and D, despite the same brand on the cover, are not FICA-funded. They run mostly on general revenue and beneficiary premiums. That detail matters when politicians talk about "Medicare cuts," because the FICA-funded portion of Medicare coverage is a smaller slice than the headline number suggests. The total tax payment from every covered worker, employer and employee combined, is what eventually pays out as social security and medicare benefits.

The trust fund clock is the part nobody wants to talk about. The Social Security Trustees' 2026 report projects OASI runs dry in 2033 if Congress does nothing, with incoming FICA receipts then covering roughly 77% of scheduled benefits. The Congressional Budget Office, in its February 2026 baseline, puts the depletion at fiscal year 2032. Neither projection assumes the program disappears. Both assume benefits automatically shrink to whatever FICA receipts can sustain. That is a political problem dressed as an actuarial one, but it does shape the policy conversation.

FICA Tax Rate 2026: How Employer and Employee Split

The headline FICA tax rate of 7.65% is half the real number. The employer matches every dollar an employee contributes, so the combined burden on each job is 15.3% of covered wages. Labor economists generally agree that workers bear both halves in the long run through suppressed wages; in a parallel universe without FICA, gross pay would be roughly 7.65% higher. The legal incidence and the economic incidence diverge.

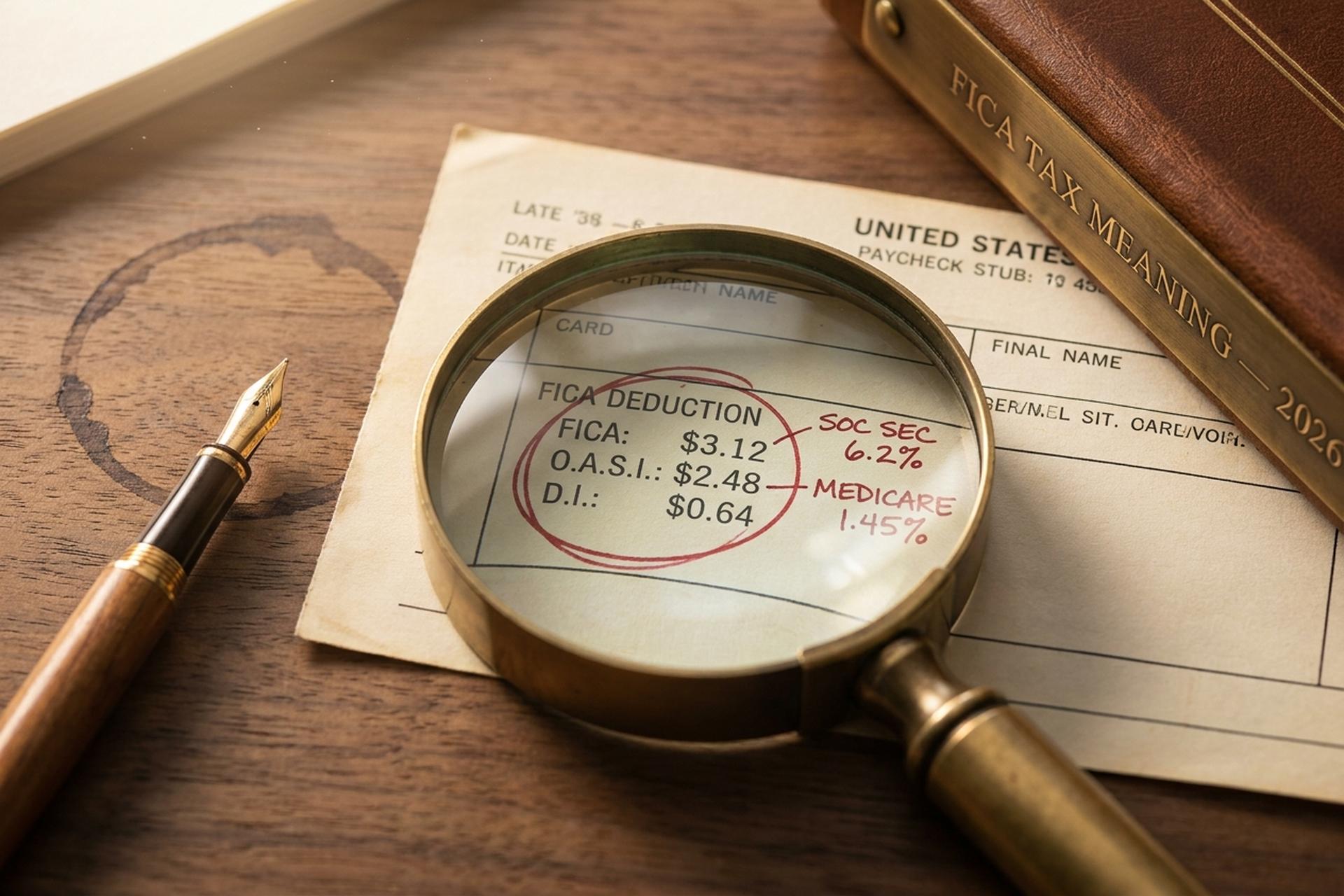

The composition has been remarkably stable since 1990. The social security portion of FICA takes 6.2% as employee tax and 6.2% as employer tax, applied to wages up to an annual cap. Add the security portion of the FICA covering Medicare at 1.45% on each side, with no ceiling, and you have the whole thing. Medicare tax applies to every dollar of wages, all year, all income levels. The only real departures from that pattern in three decades were the temporary cut to 4.2% employee Social Security in 2011 and 2012, and the 2013 introduction of the Additional Medicare Tax.

The social security wage base, which determines where the Social Security portion of the cut stops biting, climbs every year with national average wage growth. The medicare portion has no equivalent cap. The Social Security Administration set it at $176,100 for 2025 and $184,500 for 2026, a step-up of about 4.8%. For a worker earning at or above the cap in 2026, the employee and employer FICA tax withholdings each come out to exactly $11,439, and that is the same amount of tax on wages on both sides. Anything above the cap escapes Social Security entirely, which is why high earners quietly pay a lower effective FICA rate than middle earners. The combined employer and employee contributions are what fund Social Security and Medicare directly through the trust funds.

The Additional Medicare Tax, sometimes called the "additional tax" on high earners, is the wrinkle most payroll calculators get wrong. It adds 0.9% on employee wages above $200,000 for single filers, $250,000 for married filing jointly, and $125,000 for married filing separately. Crucially, the employer does not match this 0.9%; the worker pays the full surtax, which is reported on the federal tax return via Form 8959. Medicare tax applies to all earned income with no wage cap, and the thresholds for the surtax are not indexed for inflation, so each year more workers cross into Additional Medicare Tax territory.

| Component | Employee | Employer | 2026 cap |

|---|---|---|---|

| Social Security | 6.2% | 6.2% | $184,500 |

| Medicare (regular) | 1.45% | 1.45% | none |

| Additional Medicare | 0.9% | 0% | over $200k single / $250k joint |

| FICA total | 7.65%+ | 7.65% | mixed |

How to Calculate FICA Tax on Your Paycheck

Almost nobody actually checks whether their FICA was withheld correctly. The math takes about thirty seconds if you know the rules, and the failure modes are predictable: hitting the Social Security cap, working multiple jobs across the year, or stumbling across the Additional Medicare Tax threshold without an employer flagging it. Calculate FICA taxes once per tax year and you avoid most filing surprises.

Take a worker earning $50,000 in 2026. The FICA arithmetic is the easy case. Social Security at 6.2% of $50,000 is $3,100. Medicare at 1.45% is $725. The total employee FICA comes to $3,825, no cap impact, no Additional Medicare. The employer deposits the same $3,825 on its side, so a single job sends $7,650 to the federal government every year.

Now climb the income ladder. A $150,000 earner pays the full 7.65% because they are still below the $184,500 cap and well below every Additional Medicare Tax threshold. Total employee FICA: $11,475. At $300,000 the picture changes. Social Security freezes at $11,439 (the $184,500 cap × 6.2%). Medicare keeps running and produces $4,350. Additional Medicare adds 0.9% on the $100,000 above the $200,000 threshold, another $900. Total employee FICA: $16,689.

| Annual salary | Social Security | Medicare | Add'l Medicare | Total employee FICA |

|---|---|---|---|---|

| $50,000 | $3,100 | $725 | $0 | $3,825 |

| $150,000 | $9,300 | $2,175 | $0 | $11,475 |

| $300,000 | $11,439 (capped) | $4,350 | $900 | $16,689 |

The W-2 form documents the whole thing in four boxes. Box 3 holds Social Security wages (the taxable wages capped at $184,500). Box 4 holds Social Security tax withheld. Box 5 holds Medicare wages. Box 6 holds Medicare tax. The FICA deduction on every paystub is what fills these boxes. If Box 4 ever exceeds the annual maximum, something has gone wrong in payroll. Workers who held more than one job in a single year can recover excess Social Security tax (the over-cap result when employer and employee FICA combine across two payrolls) via Form 1040 Schedule 3 line 11 on the income tax return.

FICA Tax Exemptions: Students, Clergy, Foreign Workers

There is no group of US workers who genuinely "don't pay FICA," and yet the belief turns up constantly in break rooms and online forums. It is almost always wrong. The real exemption list is statutory, narrow, and full of strings. People who assume they qualify often do not. People who never think to check sometimes fall into a category they could have used.

Start with students. IRC §3121(b)(10) exempts employees enrolled and regularly attending classes at the school where they work. The phrasing matters. A graduate student paid by her own university qualifies. The same student paid by a third-party employer does not. A school administrator who happens to take a single continuing-education class does not. The IRS has litigated the distinction more than once, and the test boils down to whether education is incidental to employment, or employment is incidental to education. The second wins; the first loses.

Foreign students on F-1, J-1, M-1, or Q-1 visas get a five-year FICA exemption, counted from the calendar year of arrival as a nonresident alien. Members of recognized religious sects with long-running theological objections to insurance can opt out via Form 4029. Self-employed ministers use Form 4361. Children under 18 working in a parent's sole proprietorship are exempt. State and local government employees may or may not be covered, depending on the Section 218 agreement between the state and the SSA, and Section 218 agreements happen to be some of the most idiosyncratic documents in the entire US tax code.

The misconception worth correcting loudest, though: independent contractors and 1099 freelancers are not exempt from FICA. They pay it under a different name (SECA) at the full 15.3% rate, because there is no employer left to share the bill.

Self-Employed FICA Contributions: SECA at 15.3%

Every freelancer who has ever opened a 1040 has called SECA a "double tax." It isn't, technically; it just feels that way because you cover both halves of the 15.3% yourself, with no employer in the picture. The Self-Employed Contributions Act (also called the Self-Employment Contributions Act, IRC Chapter 2) kicks in at $400 of net self-employment earnings. The self-employment tax liability lands on Schedule SE.

Two technical details matter more than the marketing names. First, SECA applies to 92.35% of net SE earnings, not the full 100%. That 0.9235 multiplier is the IRS's rough way of giving you back the employer-side deduction a regular W-2 worker gets without thinking about it. Run the math on $100,000 of net SE earnings: 100,000 × 0.9235 × 15.3% = $14,130 in SECA, not $15,300. Second, you get to deduct half of what you paid above the line on Form 1040, Schedule 1, line 15.

The $184,500 Social Security cap still applies in 2026. The Additional Medicare Tax also stacks, which catches plenty of freelancers off guard. You pay self-employment tax via quarterly estimates through Form 1040-ES on the usual April-June-September-January rhythm. The tax deductions for the deductible half land as a federal tax payment adjustment on the return at year end. Calculate the FICA tax exposure once and the rest is mechanical. Miss a quarter and you owe underpayment penalties under IRC §6654, calculated at the federal short-term rate plus three points.

FICA Withholding on Crypto Wages and Payroll Tax

This is where mainstream FICA coverage thins out. The IRS settled the basic question over a decade ago: cryptocurrency paid as wages is treated like cash for payroll-tax purposes. The mechanics around that rule are anything but simple.

IRS Notice 2014-21 (still controlling as of 2026) established that wages paid in cryptocurrency are subject to FICA, FUTA, and federal income tax withholding, all against the fair market value of the crypto at the time of payment in US dollars. Crypto wages are subject to FICA on the same basis as cash wages: the FICA payroll tax attaches to the dollar-equivalent amount. The Form W-2 reports dollars, not coins. The employer converts at payroll time, calculates the FICA tax in dollars, deposits the dollar-equivalent FICA payments, and absorbs any timing risk between conversion and deposit. Federal and state withholding both attach to the same FMV figure, and state and local income tax rules typically follow the federal treatment.

Crypto payroll providers have professionalized this stack. Bitwage was the dominant US vendor until Paystand acquired it in Q1 2026. Deel launched stablecoin payroll on February 10, 2026, but the initial rollout is EU and UK only. Most stablecoin-rail providers convert to USD at payment moment for tax-basis purposes and then redenominate into the stablecoin for transfer. For merchants accepting USDT through a gateway like Plisio, vendor-payment timing follows the same FMV-at-payment rule. FICA compliance here means treating crypto wages exactly like cash; the FICA meaning admits no "crypto exception."

Self-employed crypto income gets messier. A miner who receives 0.1 BTC owes SECA at 15.3% on the FMV at receipt. If the BTC then appreciates and the miner sells, a second taxable event triggers capital gains tax on the appreciation, with FMV at receipt becoming the basis. Crypto freelancers face an underappreciated trap with the Additional Medicare Tax: a worker earning $180,000 on a W-2 plus $30,000 in self-employment income from crypto consulting crosses the $200,000 threshold by $10,000. The employer does not withhold the 0.9% Additional Medicare Tax (because W-2 wages alone stay under the threshold), so the worker owes $90 in surtax at filing that nobody flagged in advance. The new Form 1099-DA (gross proceeds reporting from January 2025, basis from January 2026) tightens this further by making crypto income harder to forget.

What Happens If FICA Is Withheld Incorrectly

Recovery procedures for FICA errors are asymmetric, a quiet trap for both workers and employers. Overpayment of Social Security tax (the common scenario: a worker held multiple jobs and crossed the $184,500 cap across employers) can be reclaimed by the worker directly on Form 1040 Schedule 3 line 11. Overpayment of Medicare tax has no individual refund mechanism. The employer has to file Form 941-X to correct the error, and the worker has to chase the employer to get the money back, a structurally weaker position.

Underwithholding flows the other direction. The employer is liable for the employer share of FICA regardless of whether it actually withheld correctly. The employee may owe an unwithheld balance at filing time. Most consequentially, employers who fail to deposit withheld FICA face the trust-fund recovery penalty under IRC §6672, which can reach 100% of the unpaid amount and attach personal liability to the officers responsible.

What FICA Actually Buys You: The Bottom Line for 2025

FICA is not glamorous. It is one of the most successful US federal programs, sitting on a paycheck line nobody reads. Crypto wrinkles are operational, not legal: the IRS settled that in 2014. What changes year to year: the wage base, the Additional Medicare creep, and the trust fund clock.