Payment Reversal Meaning: Types, Costs, and Prevention

A merchant checks their dashboard and finds an unexpected debit. The notation reads "payment reversal." No explanation, no warning. The money is gone, and it's not clear whether it came from a technical error, a customer complaint, or something worse. Understanding payment reversal meaning matters precisely in moments like this, because not all reversals are equal. The type determines how much it costs, who controls it, and what you can actually do about it.

A payment reversal is any process that returns funds from a transaction back to the payer. It covers everything from a same-day cancellation to a bank-forced chargeback. In 2023, payment reversals in US retail totaled $743 billion, which is 14.5% of all retail sales. For any business running card payment processing, understanding payment reversals is not optional.

What Is a Payment Reversal?

A payment reversal cancels or undoes a payment transaction and returns funds to the buyer. The trigger, timing, and cost depend entirely on what type of reversal it is and which party initiates it.

Payment reversals can be initiated by:

- The merchant, to correct an error before settlement closes

- The customer, requesting a refund directly from the seller

- The customer's bank, forcing a chargeback after a dispute

- The acquiring bank or processor, correcting a technical error

- The card network, intervening in compliance or fraud cases

Most merchants think of a payment reversal as a single event. It isn't. It's a category. Authorization reversals, voids, refunds, chargebacks, and reversal adjustments all fall under it, and they differ radically in cost, control, and timing. Treating them as the same thing is how businesses end up absorbing fees that could have been avoided.

The Five Types of Payment Reversals

Not all types of payment reversal are created equal. The full taxonomy runs from cheapest to most damaging:

- Authorization reversal — cancels a transaction before funds are captured. The issuing bank releases the hold, and the customer's funds free up within hours. No interchange fee applies because settlement never began. For any error caught early, this is the best-case outcome.

- Void transaction — cancels a payment after capture but before the daily settlement batch closes. Like an authorization reversal, no interchange fee applies. The window is narrow, typically same-day, but catching a duplicate charge or wrong amount in time means the void costs nothing.

- Refund — a seller-initiated return of funds after a transaction has fully settled. Interchange fees from the original sale don't come back; the merchant absorbs that cost regardless. Refunds take 5–14 business days to post. The merchant controls the timing, amount, and whether to issue it at all.

- Chargeback — a bank-forced transaction reversal triggered when a customer disputes a charge with their card issuer. The bank reverses the transaction without merchant consent, deducts the original amount, and charges a dispute fee of $15–$100. The merchant can contest it through representment, but the process takes weeks and requires documentation. This is the most costly type of payment reversal.

- Reversal adjustment — a correction issued by a bank or payment processor to fix a technical error, duplicate transaction, or system failure. These are rare and typically require no action from the merchant.

The cost hierarchy in practical terms:

| Type | Who initiates | Fee | Timeline | Merchant control |

|---|---|---|---|---|

| Authorization reversal | Merchant / acquirer | None | Hours | Full |

| Void transaction | Merchant | None / minimal | Same day | Full |

| Refund | Merchant | Interchange cost | 5–14 days | Full |

| Chargeback | Customer (via bank) | $15–$100 + risk | Weeks | None |

| Reversal adjustment | Bank / processor | None | Varies | None needed |

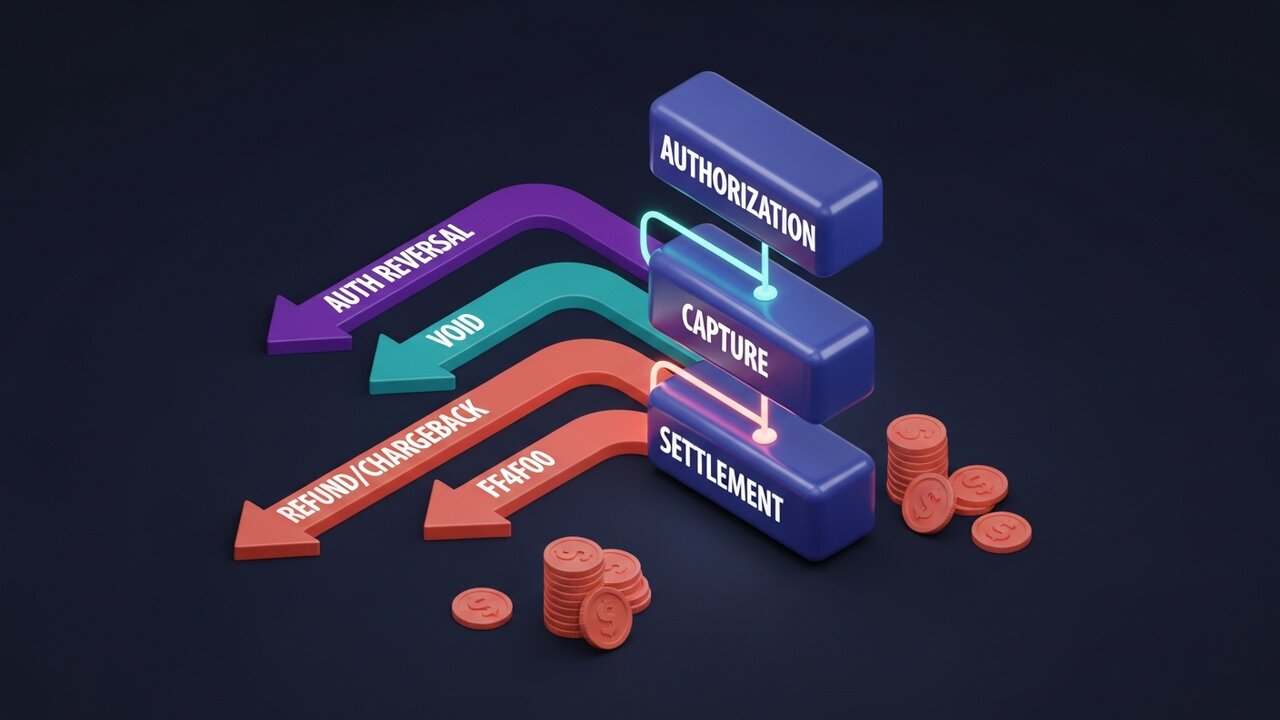

How a Payment Reversal Works

Every card transaction moves through a fixed lifecycle. The types of payment reversal available to you depend entirely on where you are in that sequence. Understanding this flow is the foundation of understanding payment reversals in a payment processing context.

The process runs in four stages:

- Authorization — the customer's bank validates the payment and places a hold on the funds. The merchant has received approval but no money has moved yet. Authorization reversals are possible at this point.

- Capture — the merchant confirms the transaction and the amount locks in for settlement. Void transactions are possible between capture and the settlement batch closing, typically by end of business day.

- Settlement — funds move from the customer's bank through the card network to the acquiring bank and then to the merchant account. This usually takes T+1 or T+2 business days. Once settlement completes, only refunds or chargebacks can return the money.

- Post-settlement dispute — if the customer contacts their bank rather than the merchant, a chargeback begins. The bank initiates a forced transaction reversal, debits the merchant's account, and opens a dispute process. The merchant has 30–45 days to respond with evidence.

Card authorizations can stay active 1–30 days depending on the merchant category. Hotels, car rentals, and subscription services often hold authorizations longer than standard retailers, which creates more time to catch and correct errors before they reach settlement.

Payment Reversal vs Refund: Key Differences

These terms get used interchangeably in everyday language, but they're not the same thing. A refund is a specific type of payment reversal, one where the merchant voluntarily initiates the return after settlement. The payment reversal meaning in this case is narrower: it's seller-initiated, post-settlement, and controlled. Payment reversal is the broader category.

The confusion matters in practice. A customer asking for "their money back" might be requesting a refund, or they might skip the merchant entirely and file a chargeback. Both are payment reversals, but the merchant experience is completely different.

| Factor | Refund | Chargeback | Authorization Reversal |

|---|---|---|---|

| Initiated by | Merchant | Customer (via bank) | Merchant / acquirer |

| Timing | Post-settlement | Post-settlement | Pre-settlement |

| Merchant control | Full | None | Full |

| Fee to merchant | Interchange cost | $15–$100 + risk | None |

| Timeline | 5–14 days | Weeks to months | Hours |

| Can be disputed? | No | Yes (representment) | N/A |

Every time a customer contacts you about a problem, you have a window to resolve it as a refund rather than letting it escalate to a chargeback. A refund costs interchange fees. A chargeback costs interchange fees plus a dispute fee, plus your time, and you have no say in whether it happens.

The Real Cost of Payment Reversals for Merchants

There's what you see on the statement and then there's everything else.

Mastercard's data on 2023 chargebacks: 80% of disputes filed that year were fraudulent. Customers falsely claimed non-receipt or disputed charges they'd authorized, a practice called friendly fraud. The year-over-year increase in chargeback fraud sat at 32%. Run the numbers for a merchant doing $50,000 monthly in payment processing volume with a 1.5% chargeback rate — that's $750 in dispute fees alone, before you count lost merchandise and the hours spent building evidence packages.

The card network thresholds make this urgent:

- Visa and Mastercard set the acceptable chargeback ratio at approximately 1% of monthly transactions

- Exceeding the threshold triggers enhanced monitoring programs

- Sustained high rates lead to rolling reserves, where the processor holds back 5–10% of each transaction for 90–180 days

- Persistent violations result in account termination, making the business unable to accept card payments at all

What most merchants don't factor in: the processor relationship. High dispute rates don't just cost fees. They cost approval rates, pricing tiers, and eventually the account itself.

What Is a Payment Reversal on a Mortgage?

Most discussions about payment reversal meaning focus on card transactions, but mortgage payments can be reversed too, and the consequences play out differently. The mechanics involve ACH or bank transfer rails rather than card network payment processing.

A mortgage payment reversal occurs when a scheduled payment fails to process and gets returned. Common causes:

- Insufficient funds in the linked bank account at the time of the debit

- Incorrect account or routing number submitted with the payment

- Bank error: duplicate posting that the bank subsequently corrects

- Payment submitted too close to the grace period cutoff

There are no chargeback fees with mortgage reversals. But the consequences can be severe: a reversed mortgage payment that isn't corrected quickly gets recorded as a late payment on the borrower's credit report. Repeated reversals can trigger penalty fees from the lender.

If you receive notice of a mortgage payment reversal, contact the lender immediately. Confirm the reason, correct the underlying issue, and resubmit before the grace period expires. Most lenders give a 15-day grace period, and acting within it typically avoids the late payment notation on your credit file.

How to Prevent Unnecessary Payment Reversals

The best payment reversal is the one that never happens. Knowing the types of payment reversal that can be prevented, versus those that are forced, focuses effort where it matters. For the types within merchant control, prevention comes down to timing and information quality:

- Catch errors before settlement — monitor transactions throughout the day; an authorization reversal or void costs nothing; a refund costs interchange fees; a chargeback costs fees plus dispute overhead

- Use clear billing descriptors — the most common reason customers file chargebacks is not recognizing a charge; make your billing descriptor match your brand name, not your legal entity name

- Accurate product listings — mismatched expectations between what was advertised and what arrived drive return and chargeback rates; photos, dimensions, and specifications need to be precise

- Send transaction confirmations — order confirmation, shipping notification, and delivery confirmation emails close the gap where customers lose track of a charge and assume fraud

- Deploy AVS and 3D Secure — address verification service and two-factor authentication at checkout block fraudulent transactions before they ever settle, cutting that entire category of chargebacks

- Track reversal patterns — a cluster of reversals from a specific product, geographic region, or customer segment points to a fixable problem, not random bad luck

- Respond to every dispute on time — each chargeback carries a 30–45 day response deadline; missing it forfeits the transaction automatically, with no appeal

- Issue returnless refunds on low-value items — for items under $20–$30, processing the return costs more than the item; refunding without requiring a return prevents escalation to a chargeback

Crypto and the Payment Reversal Problem

Card network payment reversals exist because the system was designed around consumer protection. The ability to force a transaction reversal is a feature from the buyer's perspective. From the merchant's side, the chargeback mechanism is a structural overhead that compounds over time. You didn't consent to it. You just pay for it.

Crypto payments work on different assumptions. Once a Bitcoin, Ethereum, or stablecoin transaction is confirmed on the blockchain, no party can initiate a payment reversal. There's no card issuer to file a dispute with, no card network to enforce a forced reversal, no chargeback fee. The 80% false chargeback rate that plagues card-accepting merchants has no equivalent in crypto payment processing.

When a crypto merchant needs to return funds, they manually send the equivalent amount back to the customer's wallet address. No automated process, no third-party intermediary. The merchant controls it entirely, exactly like a refund, but without the card network's timeline or fees.

For businesses dealing with high chargeback exposure, digital goods, travel, high-ticket items, adding crypto to the payment stack has a direct financial case. Plisio lets you accept Bitcoin, Ethereum, USDT, USDC, and 20+ other assets at checkout with transaction fees starting at 0.5%, and no chargeback mechanism to expose you to forced reversals.

Conclusion

Payment reversal meaning depends entirely on which type you're dealing with. Authorization reversals and voids cost nothing and preserve the transaction relationship. Refunds cost interchange fees but keep the merchant in control. Chargebacks cost the most, fees, labor, and the ongoing risk of account termination, and remove merchant control entirely.

The practical priority for any business processing cards: catch errors early, resolve complaints before customers escalate to their bank, and monitor dispute rates against card network thresholds. For understanding payment reversals at scale, the most important number isn't the fee per incident. It's the percentage of transactions that become disputes, because that's what determines whether you keep your payment processing account.

When the standard payment reversal framework doesn't fit — international sales, high-fraud categories, cross-border transactions — crypto payment rails offer a structural alternative where forced reversals don't exist. That's not a workaround. It's how the system was designed. Grasping the full payment reversal meaning, from authorization holds to chargeback disputes, is what separates businesses that control their dispute rates from those that get controlled by them.