Refund vs. Reversal Transaction: Key Differences Explained

A customer emails saying they want to cancel an order. Another calls because they received the wrong item three weeks ago. Both want their money back — but from a business perspective, these are completely different situations that require completely different responses. The difference between refund and reversal transaction isn't just terminology. It determines how fast the customer gets their money, whether you pay fees, and who actually controls the outcome.

This guide breaks down how refunds and reversal transactions work, where chargebacks fit in, and what each means for your payment operations.

What Is a Refund in a Transaction?

A refund returns funds after a transaction has already settled. Settlement is the point at which money moves definitively from the customer's bank account to yours. Once that's done, the transaction is complete, and getting the money back requires starting a new, separate process.

When you issue a refund, the payment processor routes a credit back to the customer's original payment method. Your account gets debited; the customer's account receives the credit. No third party forces this — the business initiates it voluntarily.

Key facts about the refund process:

- Timing: Only possible after full settlement, usually T+1 or T+2 after the original transaction

- Speed: 5–14 business days for the credit to appear on the customer's statement, depending on the card network and issuing bank

- Fees: Interchange fees from the original transaction are not returned — the seller absorbs that cost even when issuing a refund

- Initiated by: The seller (or their payment processor at the seller's request)

- Customer experience: The original charge stays visible; a separate refund credit appears afterward

If a customer contacts you five days after a purchase about a defective product, that's a refund situation. The transaction settled days ago. Your payment processor handles the credit routing, but it won't be instant, and the interchange cost you paid to process the sale stays paid regardless.

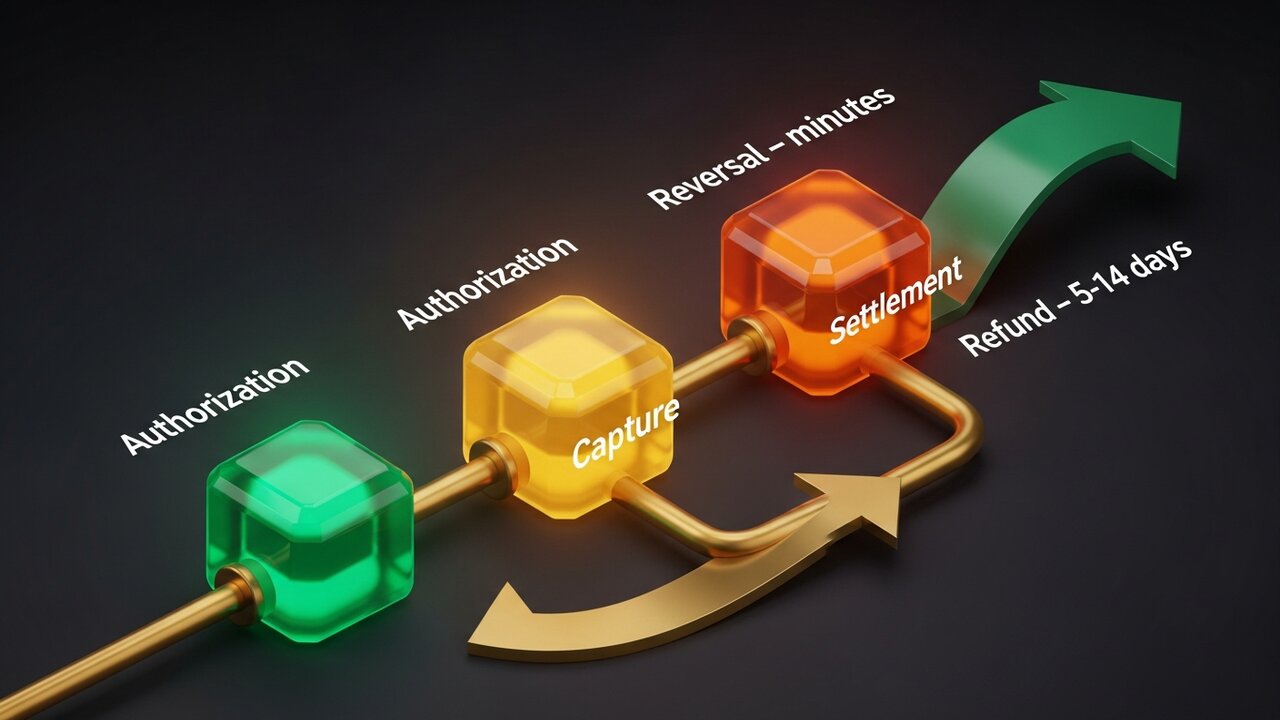

What Is a Reversal Transaction?

A reversal transaction cancels a payment before it fully settles. There's a short window between when a card payment is authorized and when funds actually move, and that window is where reversals live.

When a customer pays by card, the issuing bank places a hold on their funds. The acquirer then captures that authorization and sends it to the bank for settlement. A reversal intercepts this process before the settlement batch closes, releasing the hold without ever completing the transfer.

Three distinct types fall under the reversal umbrella:

- Authorization reversal — initiated before the transaction is captured; the hold is voided and the customer's funds are freed immediately

- Void — initiated after capture but before the daily settlement batch closes; still avoids interchange fees

- ACH reversal — a bank-initiated cancellation of an ACH transfer due to account errors, insufficient funds, or duplicate entries

No money actually moved. Because settlement never occurred, no interchange fee applies — the transaction disappears as if it never happened from a financial standpoint. The customer sees the hold drop off their account, usually within hours.

Key Differences Between Refund and Reversal

To understand the difference between refund and reversal transaction, a side-by-side view is the clearest approach:

| Factor | Refund | Reversal |

|---|---|---|

| When it happens | After settlement | Before settlement |

| Initiated by | Merchant | Merchant, acquirer, or card issuer |

| Processing time | 5–14 business days | Minutes to 24–48 hours |

| Interchange fees | Merchant absorbs | Not charged |

| Customer account | Credit posted separately | Hold released |

| Best used for | Returns, post-delivery disputes | Errors, same-day cancellations |

If you catch a problem fast enough — same day, ideally within hours — a reversal is almost always the better option. It's faster for the customer and cheaper for you. Once that window closes, you're in refund territory.

Both options are seller-friendly compared to the third one, which is why the difference between a refund and reversal transaction matters far more than most store owners realize.

Three Types of Payment Reversals Compared

"Payment reversal" is a broader term than most people expect. It covers three distinct mechanisms, each with a very different cost profile:

- Authorization reversal (void before capture) — The cheapest option. Cancels the transaction before any funds are captured. No interchange fee, no chargeback fee, near-instant resolution. Works for errors caught within hours of the original transaction.

- Refund (seller-initiated post-settlement) — More expensive. The transaction completed, so interchange fees apply. The seller voluntarily returns the funds. Slow — 5–14 business days — but controlled. You decide when and whether to issue it.

- Chargeback (customer-initiated dispute) — The most damaging. The customer goes to their card issuer rather than you to dispute a charge. The bank reverses the transaction without your consent, deducts the original amount, and charges a dispute fee, typically $15–$100 per incident. You can fight it through a representment process, but winning takes time and documentation.

The cost hierarchy is worth knowing for business planning:

| Type | Who initiates | Fee | Timeline |

|---|---|---|---|

| Authorization reversal | Merchant / acquirer | None | Hours |

| Void | Merchant | Minimal or none | Same day |

| Refund | Merchant | Interchange cost | 5–14 business days |

| Chargeback | Customer (via bank) | $15–$100 + risk | Weeks |

Chargebacks above 1% of monthly transactions put accounts at risk. Payment processors flag high rates, impose rolling reserves, or terminate accounts entirely. Knowing when to cancel, when to refund, and how to prevent chargebacks is real cash flow management.

Examples of Refunds and Reversal Transactions

Take a clothing store where a customer orders a winter jacket. Two weeks later it arrives with a broken zipper. The customer asks for a return. By the time they get in touch, the transaction settled 12 days ago — there's no reversal window left. The store processes a refund through its payment processor. Seven to ten business days pass before the customer sees a credit. The interchange fees from the original sale don't come back.

Contrast that with a hotel scenario. The property pre-authorizes $400 on a guest's card at check-in. The final bill comes to $310. Within hours of checkout, the hotel's system releases the $90 excess hold — a standard authorization reversal. The guest's bank frees the funds that same day. No fee, no paperwork, no trace of a $90 charge on the guest's statement.

A restaurant provides another clean example of a void. A server runs an $85 dinner charge and accidentally submits it twice. The duplicate shows up in the terminal before the nightly settlement batch closes. A manager voids the duplicate. The customer never sees it; the restaurant pays nothing extra because the transaction never cleared.

Chargebacks look different. A customer buys software, downloads it, and three weeks later calls their card issuer saying they don't recognize the transaction. The bank kicks off a reversal process without contacting the seller at all. A chargeback notification lands in the seller's account — minus the $49 sale and a $35 dispute fee on top. Getting the money back means building an evidence file: the receipt, download logs, IP address, timestamped access records. And it has to arrive before the card network's deadline.

The first three scenarios all have a path to zero cost. The fourth one doesn't.

How Refunds and Reversals Affect Merchant Cash Flow

The financial impact of refunds and reversal transactions isn't about isolated incidents. At scale, the patterns tell a different story.

Authorization reversals and voids leave cash flow untouched. The funds never settled, so there's nothing to claw back. In accounting terms, these transactions disappear cleanly.

Refunds hit cash flow directly. The money was in your account; now it isn't. When refund rates climb above 2–3%, payment processors start paying attention. High rates trigger risk signals — the processor may hold back a percentage of each transaction (typically 5–10%) for a rolling 90–180 day period as a financial buffer.

Chargebacks compound the damage differently. Each one deducts the transaction amount and tacks on a fee. A business running a 1.5% chargeback rate on $50,000 in monthly revenue is paying $750+ in fees monthly, before accounting for the lost revenue itself.

Steps that reduce exposure over time:

- Watch authorization-to-settlement timing and act on errors before the settlement window closes

- Write clear return policies — customers who know how to request a refund rarely escalate to a dispute

- Use AVS and 3D Secure to block fraudulent transactions before they turn into chargebacks

- Track refund and reversal rates separately in your processor dashboard; they point to different problems

- For digital goods, keep evidence packages ready in case a chargeback arrives

Crypto Payments and the Reversal Problem

Card networks are built on the assumption that completed transactions can be reversed — by the bank, by regulatory action, or by fraud. Crypto works on the opposite premise: confirmed transactions are final.

Once a Bitcoin, Ethereum, or stablecoin payment is confirmed on the blockchain, no party can reverse it. There's no authorization window to cancel. There's no card issuer to file a dispute with. The chargeback mechanism that costs card-accepting businesses billions annually simply has no equivalent in crypto.

That changes the refund and reversal landscape in concrete ways for sellers:

- No chargebacks — friendly fraud (falsely claiming non-receipt) doesn't work without a card network to file the dispute with

- No unauthorized reversals — only the seller can send funds back, and only by sending a new outgoing transaction

- Refunds are manual — a crypto refund means sending the equivalent amount back to the customer's wallet address; no processor automates this

- Disputes are handled directly — without a card network intermediary, sellers set their own policies and manage disagreements with customers themselves

- Settlement is instant — no T+1/T+2 delay; confirmed funds arrive in your wallet immediately

For businesses dealing with chargeback fees and fraudulent disputes, adding crypto as a payment option has a real financial case. Plisio lets you accept Bitcoin, Ethereum, USDT, USDC, and 20+ other assets at checkout — no chargeback exposure, transaction fees from 0.5%.

Conclusion

The difference between refund and reversal transaction is fundamentally about timing. Reversals work before settlement — fast, cheap, controlled. Refunds work after — slower, more expensive, still controlled. Chargebacks are a forced version that removes your control entirely and costs the most.

For any business processing card payments, catching errors early enough to void rather than refund saves real money. Managing refund rates keeps your processor relationship healthy. And structuring your payment stack to limit chargeback exposure — whether through better fraud controls or by adding crypto where reversals aren't possible — directly protects your margins.

The goal isn't to never have returns. It's to route each one through the path that costs the least.