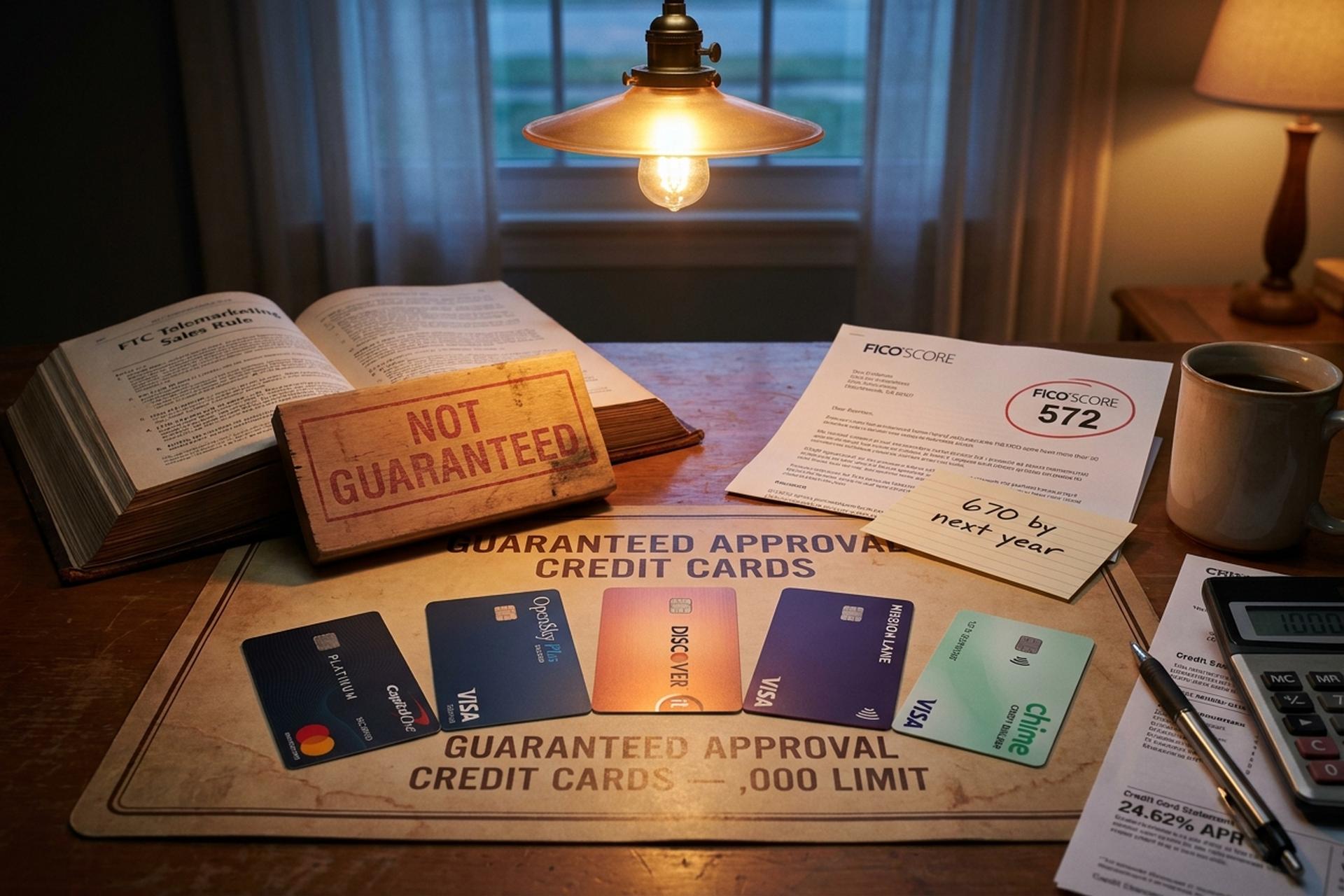

Guaranteed Approval Credit Cards With $1,000 Limits for Bad Credit

"Guaranteed approval credit cards" is one of the most marketed pitches in subprime finance. It is also one of the most misleading. No regulated US issuer can legally promise approval before reviewing your application. The Truth in Lending Act, the Equal Credit Opportunity Act, and the FTC's Telemarketing Sales Rule all require a real underwriting decision. The FTC has brought roughly 60 cases against marketers who used this exact promise to extract upfront fees. So if you have bad credit and you want guaranteed approval credit cards with $1,000 limits, the answer is not "find the magic card." It is "find the closest legal equivalent and apply the right way."

This guide breaks down which credit cards actually approve people with bad credit in 2026. It covers the initial credit limit math you need to reach a $1,000 line. It flags the fee traps that turn cheap-looking subprime cards into expensive mistakes. It also covers a niche question for businesses: if you have been cut off from banks and card networks, what is the alternative? Roughly 16% of Americans hold a FICO score below 580 per Experian. The average card APR ran at 24.62% in January 2026 per the CFPB. So the stakes for picking the right product are real. Many credit cards aimed at less-than-perfect credit are designed to help you build credit history while protecting the card issuer from default risk.

What "guaranteed approval" actually means and doesn't

In US consumer-finance law there is no such thing as a guaranteed approval credit card. Issuers can pre-qualify you with a soft inquiry that does not affect your credit, and they can publish approval-odds calculators that estimate the likelihood of acceptance based on your credit profile. They cannot legally promise the final result before a full application is reviewed. Any company that does is either a scam (advance-fee fraud is the FTC's name for it) or is marketing a product that is not actually a credit card.

The closest legitimate equivalent is a no-credit-check secured card. Because the deposit collateralises the credit line, the credit card issuer takes essentially no credit risk and approves nearly everyone who funds the account. The OpenSky Plus Secured Visa credit card runs no credit check at all, requires a $300 minimum security deposit, and reports to the three credit bureaus. The Chime Card, technically a credit builder secured Visa, does not require a credit check, no minimum deposit, no annual fee, and no interest, but it needs a Chime checking account and only reports on-time payments rather than the credit utilization ratio. Both will approve a thin-file low credit or poor-credit applicant who would be declined for many unsecured cards for poor credit.

This is the practical translation of the search query: "guaranteed approval" almost always means "secured card with low or no credit check." It is also why looking to rebuild credit through one of these card offers is the standard 2026 entry point for people with bad credit looking to rebuild their credit. A best credit card for a thin-file applicant is rarely the one with the flashiest rewards; it is the one that reports to all three major credit bureaus consistently month after month.

Best secured credit card for bad credit and credit builder picks

A secured credit card requires a refundable deposit equal to the credit limit. The deposit is the issuer's protection if you stop paying, and it is the reason secured credit card requires that the deposit be funded before activation but approval rates are so much higher than for unsecured products. The strongest options in 2026 are the ones that combine a low minimum deposit, no annual fee, reporting to the three major credit bureaus, and a clear path to a credit limit increase or unsecured graduation. These secured cards help you rebuild your credit by gradually demonstrating that you can manage a credit card responsibly, which over time will improve your credit score and credit profile.

| Card | Min deposit | Limit range | Annual fee | APR | Notes |

|---|---|---|---|---|---|

| Capital One Platinum Secured Mastercard | $49 / $99 / $200 | $200 starting, up to $1,000+ | $0 | 28.99% | Only card with a non-1:1 deposit-to-limit ratio |

| OpenSky Plus Secured Visa | $300 | $300–$3,000 | $0 | 23.89% | No credit check; $1 deposit = $1 limit |

| Discover it Secured Credit Card | $200 | $200–$2,500 | $0 | 26.49% | 2% cash back at gas stations and restaurants |

| Self Visa Credit Card | $100 | $100+ | $25 after year 1 | 27.49% | Pairs with Self Credit Builder Account ($9 admin fee) |

| Chime Card (Credit Builder Secured Visa) | None | Equals deposited cash | $0 | 0% (no interest) | Requires Chime Checking; utilization not reported |

The Capital One Platinum Secured Mastercard is the only product on this list that breaks the 1:1 deposit-to-limit relationship. Deposit just $49 and you can open a $200 line, then build toward a $1,000 limit through on-time payments and Capital One's automatic credit-line-increase reviews after the first six months. Every other secured card requires roughly $1 of deposit for every $1 of credit, which means a starting credit limit of $1,000 generally requires a $1,000 security deposit.

Unsecured credit card options for a credit card with bad credit

An unsecured card requires no deposit, which is the appeal for applicants who do not have a spare $300 to $1,000 sitting around. The trade-off is that the issuer is taking real credit risk, so the underwriting is stricter and the fees are usually heavier. The honest 2026 list is shorter than it used to be.

| Card | Limit range | Annual fee | APR | Best for |

|---|---|---|---|---|

| Mission Lane Visa | $300–$700 | $0–$59 | 19.99%–33.99% | Pre-qualification with soft pull |

| Credit One Bank Platinum Visa for Rebuilding | $300+ | $75 year 1, $99 after | 29.74% | Last-resort no-deposit option |

| Petal 2 "Cash Back, No Fees" Visa | $300–$10,000 (legacy) | $0 | varies | Closed to new applicants in 2026 |

| Cred.ai Unicorn Card | varies (WSFS Bank) | $0 | n/a | Credit-builder; functions closer to debit |

| Tomo Card | varies | varies | varies | Operationally compromised; avoid |

Two of the brand-name cash-flow underwriters that dominated this category in 2023 are effectively gone — and that absence reshapes the realistic shortlist for any unsecured credit card in 2026. Petal stopped accepting new applications after Empower Finance acquired it; Tomo has had spending disabled for some accounts and persistent customer-service issues running through 2026. Mission Lane is the strongest active option for an unsecured credit card with bad credit alongside a soft credit card application pre-qualification step, and Credit One is the no-questions-asked fallback if you can absorb the annual fee. Note that very few business credit cards approve applicants with a sub-580 personal credit score, so business owners with bad credit usually start on the consumer side too.

Why some credit cards require punishing fees: traps to avoid

The single most expensive card a consumer with bad credit can sign up for in 2026 is the First Premier Bankcard. Many advisors flag it as one of the worst instant approval credit cards for bad credit on the market. The fee stack is documented and worth reading. A one-time program fee of $55 to $95. An annual fee of $50 to $125 in year one, often $125 thereafter. Monthly servicing fees of $6.25 to $10.40 from year two. A 36% APR. And a 25% credit-limit-increase fee. A $300 limit can be cut by 25% or more in fees before you spend a dollar. Credit One is cheaper but still loads $75 in year one on a $300 line.

Then there are the marketing-only products. Any pitch that promises approval in exchange for an upfront fee is illegal under the FTC Telemarketing Sales Rule. Reload-fee prepaid debit products marketed as "credit cards" do not build credit. They do not report a credit line to the bureaus. If a product is not in the three major credit bureaus' files and not issued by a Member-FDIC bank, it is not what you want.

How a $1,000 credit limit affects your credit score and history

A $1,000 starting credit limit matters less for the spending power and more for the utilization math — a number that drives roughly 30% of your FICO score on its own. Credit scoring models penalize balances above 30% of the available credit, so a $1,000 line lets you carry up to $300 without hurting your credit score. The same balance on a $300 line drives utilization to 100% and tanks the score immediately. Issuers that report a higher credit limit to the bureaus therefore deliver more credit-building value than a higher initial limit on paper that the issuer chooses not to report.

The realistic timeline is well documented. With a single secured card, on-time payments, and utilization under 30%, applicants usually move from a 580 FICO score to a 670 prime score in 12 to 18 months. The first visible improvement on a credit report shows up at the two- or three-month mark. That is when one full month of activity reports. VantageScore 4.0 was approved for Fannie Mae and Freddie Mac mortgages on July 8, 2025. FICO 10T historical scores publish in summer 2026. Both models use trended data and alternative data such as rent and utility payments. That gives subprime applicants new paths to score boosts.

How to apply: rebuild credit, minimum credit score and credit history

Three rules cover most of the practical playbook for the credit card application stage. First, use the soft-inquiry pre-qualification tools that Capital One, Mission Lane, and a handful of other issuers publish before applying. They show approval odds without affecting your credit. Second, do not stack a hard credit check in the same month. Each hard credit pull shows on your credit history and aggregate inquiries can hurt your credit score. Third, dispute anything on your credit report that is wrong. The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days, extendable to 45 if you supply new evidence during the review. Many credit cards do not require a credit check at all on the secured side, so if speed matters and you want to improve your credit fast, those are the path of least resistance.

If you are denied, the issuer must send an adverse-action notice explaining why. Read it. The reason given (usually too many recent inquiries, too little credit history, or a derogatory item) is the exact thing to fix before reapplying.

Plisio: a crypto-payments alternative for debanked businesses

This guide is about consumer credit cards. There is a separate, growing category of users for whom the question is not "which card should I apply for" but "how do I accept payments at all," because their business has been cut off from card networks or bank processors. The House Financial Services Committee's November 30, 2025 debanking report documented at least 30 crypto entities and individuals, including Coinbase, Marathon Digital, and founders of Uniswap, Ripple, and Gemini, that were cut off from banking services under prior-administration FDIC pause letters. Even with the GENIUS Act now in force, banks remain cautious about reputational risk categories.

Plisio is a merchant-side crypto-payment gateway built for that gap. The flat fee on its Gateway API tier is 0.5%, with a 1.5% white-label option and a free personal wallet for individual receivers. Supported assets include BTC, ETH, USDT on both Tron and Ethereum, USDC, LTC, BCH, DOGE, DASH, XMR, and a handful of other stablecoins and altcoins. Settlement goes directly to the merchant's own wallet, and the standard onboarding does not require KYC, though verification may apply at higher tiers and in specific jurisdictions. This is a B2B tool, not a consumer credit replacement. If your business cannot get a Visa or Mastercard merchant account because of the categories it operates in, Plisio is one of the cleaner alternatives to keeping the storefront open.

Cash rewards credit card options from a best credit card company

The reason to start with a secured or subprime unsecured card is to graduate from it. Once your credit score crosses into the high-600s, the cash rewards credit card market opens up and you can find credit cards designed for fair-credit consumers instead of those with bad credit. Capital One Quicksilver Secured is unusual in that it offers 1.5% to 5% cash back on a secured Visa credit card with a 28.99% APR and no annual fee, a useful step-up product that several credit card companies do not match. Discover credit cards include the Discover it Secured Credit Card, which rotates 2% cash back at gas stations and restaurants, with Discover matching all cash back earned in the first year. Either is a defensible path to your first prime online credit card 12 to 18 months later, and the credit card benefits get materially better as you move up. Student credit card products like the Discover it Student or Capital One Quicksilver Student are also worth checking if you are enrolled.

Conclusion

A genuinely guaranteed approval credit card does not exist in the legal sense in 2026, and the closest substitute, a no-credit-check secured card, usually requires a deposit equal to the credit limit you want. Capital One Platinum Secured is the rare card that breaks the 1:1 rule, Mission Lane is the best unsecured option that runs a soft pre-qualification, and First Premier is the cleanest example of what to avoid. If you are a business that has been pushed out of card processing entirely, crypto gateways like Plisio fill a different gap. Either way, the path back to prime credit is roughly 12 to 18 months of disciplined utilization.