Strangle Strategy: Long and Short Strangle Explained

A strangle is one of the few trades where you do not care whether the price goes up or down. You only care how far it moves. It is a volatility trading strategy, a bet on motion itself placed with two options at once, and it strips away the guessing game of direction that ruins most beginners.

That makes the strangle strategy one of the cleaner option strategies to reason about, and unusually easy to misuse. This guide walks through what a strangle is, the long and short versions and why they are almost opposites, the breakeven math, how to actually trade one, how it compares to a straddle, and how the whole thing changes on crypto options, where volatility runs several times hotter than the stock market. None of this is financial advice; it is a map of how the tool works.

What Is a Strangle in Options Trading?

A strangle is built from two out-of-the-money options on the same asset with the same expiration date: an out-of-the-money call above the current price, and an out-of-the-money put below it. The two strikes sit apart, which is the detail that defines the strategy.

Because the strikes straddle the price from a distance, the position is neutral on direction. It does not lean bullish or bearish. What it leans on is volatility, the size of the coming move. A strangle is a volatility play first and a directional trade never.

Which way you take those two options flips everything. Buy them both and you have a long strangle, a bet that the market is about to move hard. Sell them both and you have a short strangle, a bet that it will sit still. Same three letters, opposite worldviews.

This is why traders reach for a strangle when they have a strong opinion about volatility but no conviction about direction — they think a stock is about to explode or go quiet, without knowing which way the explosion points. A directional trader buys a call or a put. A volatility trader builds a strangle. The distinction is the whole game.

| Feature | Long strangle | Short strangle |

|---|---|---|

| Setup | Buy OTM call + OTM put | Sell OTM call + OTM put |

| Max profit | Large to unlimited | Capped at premium received |

| Max loss | Limited to premium paid | Large to unlimited |

| Profits when | Price moves far either way | Price stays between the strikes |

| Best when | Volatility is low, big move expected | Volatility is high, calm expected |

Long Strangle: Betting on a Big Move

The long strangle is the safer side to learn first, because your risk is known the moment you enter.

How it works

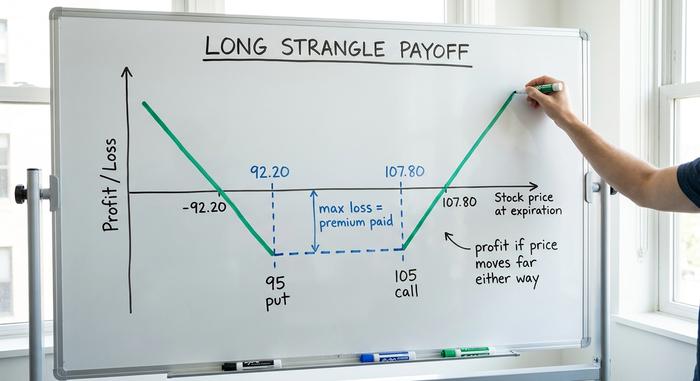

You buy an out-of-the-money call and an out-of-the-money put, paying a premium for each. Add the two premiums together and you have your entire risk, the most you can lose no matter how ugly things get. If the underlying stock just sits there and both options expire worthless, you are out that premium and not a penny more. Flip it around and the upside opens up: a price that rockets higher lets the call run without a ceiling, and a price that collapses sends the put climbing as the stock heads toward zero. Small known downside, big open-ended upside on either end. That lopsided shape is exactly why long strangles appeal to traders who would rather lose a little for certain than risk losing it all.

Breakevens, with an example

The trade only pays once the move covers what you spent. The upper breakeven is the call strike price plus the total premium; the lower breakeven is the put strike price minus the total premium. Say a stock trades near $100 and you buy a 105 call and a 95 put for a combined $2.80. Your breakevens sit at 107.80 on the upside and 92.20 on the downside. Anywhere between those two numbers at expiration, you lose money. The stock price has to move more than the premium, not just nudge, before you see a profit.

When to buy one

A long strangle makes sense when you expect a big move but genuinely cannot call the direction: ahead of an earnings report, a court ruling, an ETF decision, or a central bank meeting. It works best when implied volatility is low, because you are buying cheaply. Rising implied volatility lifts the value of both options (positive vega), while time decay quietly bleeds the position every day the move fails to arrive. Buy a long strangle and the clock is your enemy.

Short Strangle: Selling Volatility for Income

The short strangle is the mirror image, and it is where traders make steady money right up until they do not.

How it works

Here you sell the out-of-the-money call option and the out-of-the-money put option — a short call and a short put — and you collect the option premium upfront. That premium is the most you can make. As long as the price drifts and stays between your two strikes, both options expire worthless and you keep the credit. The problem is the other side of the ledger. If the price breaks above the call strike price or below the put strike price, your losses open up, large on the downside and effectively unlimited on the upside. You are getting paid a small, fixed amount to take on a big, open-ended risk, and the maximum loss is effectively undefined.

Margin and the risk you are really taking

Because the loss is undefined, brokers require margin to hold a short strangle, and most want meaningful account equity behind it, often several thousand dollars at minimum under US rules. There is also assignment risk if an option lands in the money. None of that is a reason to avoid the trade, but it is a reason to size it honestly. The disciplined approach is to take profits early, around 50% of the premium collected, and to roll the untested side closer rather than waiting greedily for every last dollar. Selling a strangle and walking away is how accounts get vaporized.

When to sell one

A short strangle fits a high implied volatility environment that you expect to cool down, paired with a view that the asset will stay rangebound so that each option expires worthless. Time decay now works in your favor (positive theta), and falling volatility helps you (negative vega). In plain terms: you sell when options are expensive and the market is nervous, betting the nerves fade.

Strangle vs Straddle: What's the Difference?

The strangle has a close cousin, the straddle, and people mix them up constantly. The difference is just the strikes.

| Feature | Strangle | Straddle |

|---|---|---|

| Strikes | Two OTM strikes (call above, put below) | One ATM strike (call and put together) |

| Cost | Lower | Higher |

| Breakeven width | Wider | Narrower |

| Move needed to profit | Larger | Smaller |

Picture both trades on the same stock at $100. A long straddle plants the call and the put right on the $100 strike. That costs more, but it starts making money the moment the stock twitches in either direction. A strangle backs the strikes off, maybe a 110 call and a 90 put, so it costs a fraction as much. The catch is that the stock now has to travel a real distance before either leg pays. Cheaper ticket, bigger move required. That trade-off is the whole story.

So which one do you want? It comes down to two questions: how far do you think the thing moves, and how much will you pay to find out? Sellers face the mirror image. Sell a straddle and you pocket more premium but get poked the instant price drifts; sell a strangle and you collect less while the price gets more room to wander before it ever starts to hurt.

How to Trade a Strangle Step by Step

The mechanics are simple. The edge lives in strike choice, breakeven points, and exits, not in being right about direction.

It starts with the strikes. How far out of the money you reach sets the personality of the trade: pull the strikes in close and the position costs more and triggers sooner; push them far out and it gets cheap but demands a bigger move to matter. Most traders lean on delta to choose, parking each strike price somewhere around 0.15 to 0.30 delta, which roughly balances what you pay against the odds of getting tested. Quick illustration: with a stock at $100, a 110 call and a 90 put become a long strangle if you buy them and a short strangle if you sell them. Same strikes, opposite bets, decided entirely by which side you take. And before you click, make sure both legs actually trade, with tight spreads and real open interest, so you are not trapped when it is time to leave.

Then comes sizing, the part people love to skip. Pick a loss you can live with, especially on the short side where the damage runs open-ended, and build the trade around that number. Write your exit rules down before you enter, not in the middle of the panic: take profits near half the maximum on a short strangle, give the position roughly 45 days so time decay can do its work without the wild gamma of the final week, and roll the untested leg if one side gets threatened. Options punish improvisation. A strangle is a plan, not a reflex.

Trading Strangles in Crypto Options

This is where the strategy gets a personality transplant. Crypto's volatility makes strangles both far more lucrative and far more lethal than any equities textbook assumes.

Start with the market. Most crypto options trade on Deribit, where Bitcoin options open interest hit a record near $50 billion in October 2025. The picture is shifting fast: BlackRock's IBIT Bitcoin options briefly overtook Deribit on open interest in 2026, the first US venue to lead, while Deribit still handles the vast majority of Ether options. CME launched round-the-clock crypto futures and options in May 2026, closing the gap with the 24/7 crypto-native venues.

The number that matters most for strangles is implied volatility. Bitcoin's 30-day implied volatility, tracked by Deribit's DVOL index, ran roughly 45% to 63% in late 2025. The equity market's VIX over the same stretch sat near 16. Crypto implied volatility runs three to four times hotter than stocks, and that single fact reshapes the trade. Strangle premiums on Bitcoin are fat, which is wonderful if you are selling them and painful if you are buying. But the moves are equally outsized, so a long strangle that would never pay on a sleepy stock can pay handsomely on Bitcoin.

The danger cuts the other way too. A short strangle on Bitcoin is selling volatility in the most violent liquid market on earth. A single 20% candle — the kind crypto prints over a quiet weekend — can blow straight through both strikes and turn a month of collected premium into a brutal loss. And because crypto never closes, there is no overnight gap to hide behind and no pause to manage risk; the position is live at 3 a.m. on a Sunday just as it is on a Tuesday open.

The scale here is enormous. Deribit and its rivals settled roughly $27 billion of Bitcoin and Ether options in a single year-end expiry in December 2025, the kind of event that can pin or whip the price as dealers hedge. If you run a long strangle into a known catalyst — a Bitcoin ETF ruling, a major network upgrade, or a Fed decision — the rich premium you pay can still be worth it when the move is violent enough. On the short side, treat crypto strangles with far more caution than any stock would ever demand, and never size one as if Bitcoin behaves like a blue-chip. Personally, I treat a short crypto strangle as a position that needs babysitting, not one I can ever set and forget.

Using the Strangle Strategy Wisely

A strangle is, at heart, a way to trade volatility itself. Go long when you think the market is underpricing the coming move and short when you think it is overpricing calm. The mechanics never change; only your read on volatility does.

In crypto the premiums are bigger and so is the tail, so the short side deserves real respect and a hard risk limit. Used with defined size, clear breakevens, and an exit decided in advance, the strangle strategy is one of the most honest trades in options, because it forces you to have a view on movement rather than a hunch about direction. So before you place one, ask the only question that matters: is the market pricing the next move too cheaply, or too dearly?