How to Short Sell Crypto in 2026: Methods, Exchanges, Risks

The biggest liquidation event in crypto history happened on October 10 and 11, 2025. In a single 24-hour window, $19.3 billion in leveraged positions vaporized across the major exchanges. Roughly 1.6 million trading accounts were wiped out. At 21:15 UTC on October 10, a single 60-second slice of the market burned $3.21 billion. The trigger was a US tariff announcement; the mechanism was forced selling as price whipsawed. Both long and short positions died together. Shorting crypto means betting against price, and in a market with 4%-plus average intraday volatility, that bet can double your margin or zero it inside an hour. Five methods exist, not all of them legal where you live. This guide walks through how each method actually works in 2026, which one fits which kind of trader, and what the post-FTX, post-MiCA regulatory map allows for US and EU residents.

What does "short sell" mean in crypto?

Short selling is a bet that price goes down. The classical version: you borrow the asset from a broker, sell it at today's price, wait for a lower price, then buy it back cheaper, return it to the lender, and keep the difference. The modern crypto version usually skips the borrowing step and uses a derivative (a futures contract, a perpetual swap, an option, or one of several CFDs) that pays out when the underlying asset's price drops on the trading platform you happen to use. A trader who wants to short opens such a position with relatively little upfront margin compared with what an outright sale would tie up. Either way, the trader who opens a short position profits when the market falls and loses when it rises. The opposite stance, the long position, profits on the way up. Every method in this guide is a flavor of one of those two paths. The honest question for anyone new is not what method exists, but why you want to short in the first place: speculation, hedging, or basis trade.

Why traders short crypto: speculators vs hedgers

There are two distinct audiences for short positions, and they use the same tools for very different reasons.

The speculator wants to profit from a down move, to go short and collect when others are selling. Bitcoin fell roughly 38% from its October 2025 all-time high near $126,000 to about $77,000 in early May 2026, with persistent negative funding rates since April 19. Every percentage point of that decline put money in the pocket of every trader holding a short. The same logic applies to other volatile cryptocurrencies during their own bear phases. Most major altcoins are far more volatile than BTC, which is part of why so many trading strategies built around shorts target them.

The hedger has a different goal: insurance. Someone holding 10 BTC in cold storage can open a small futures short that gains in value if BTC drops. The futures gain offsets the spot loss. If BTC rises instead, the futures loses but the spot wins by more. It is the same idea a farmer uses to lock in the price of next year's corn.

A third use case is the basis trade, mostly institutional: short sellers operating at scale buy spot via an ETF and short CME futures at a higher price to capture the spread. When SOL and XRP new contracts launched in July 2025, the annualized basis briefly spiked to 50%, drawing serious institutional flow. Hedging demand is now so strong that BTC options open interest ($65 billion) has exceeded futures open interest ($60 billion) every month since July 2025. The market is moving from raw leverage toward measured downside protection.

Five ways to short crypto in 2026

There are five practical methods plus one US-friendly sixth path. It is possible to short bitcoin and most major coins through any of them, but they differ on leverage, ongoing cost, counterparty risk, and where in the world you can legally use them. Choose based on holding period: short-term tactical bets favor perps, multi-month hedges favor dated futures or put options.

| Method | Max leverage | Ongoing cost | Counterparty | US access | Best for |

|---|---|---|---|---|---|

| Spot margin | 2x–10x | Borrow interest | CEX (Kraken, Binance, OKX) | Limited (Kraken 5x) | Beginner shorts |

| Perpetual futures | up to 100x–125x | Funding rate every 8h | CEX (Binance, Bybit, OKX) | No (US-blocked) | Active traders |

| Dated futures | 2x–25x | No funding, expiry roll | CME, Deribit | Yes (CME) | Hedgers, basis trade |

| Put options | Premium-limited loss | Premium decay (theta) | Deribit, IBIT, CME | IBIT puts US OK | Defined-risk bets |

| DEX perps | up to 50x | Funding rate | Smart contract | Mostly no | Non-custodial users |

| Inverse ETFs (BITI) | None (1x daily) | 1.01% expense ratio | Brokerage | Yes | US retail starters |

Spot margin is the classical version. You borrow BTC or ETH from the cryptocurrency exchange, sell it on the spot market, then buy back the same amount later to repay the loan. Every move shows up as a clear cryptocurrency price movement on your account dashboard. Kraken caps margin leverage at 2x–5x for US users; Binance and OKX go higher offshore.

Perpetual futures are the dominant crypto derivative. Total open interest hit $99.09 billion in April 2026 across all exchanges, with Binance holding 33% and OKX another 15% of the CEX market. Perps never expire; instead, a funding rate is paid every 8 hours between longs and shorts to keep the contract anchored to spot.

Dated futures behave more like traditional futures. They have an expiry, no funding rate, and in the futures market they are the instrument institutions prefer for regulated US-broker access. CME crypto notional volume hit $3 trillion in 2025, with average daily volume up 46% year-over-year in 2026.

Put options give the right to sell at a strike price; if spot falls below the strike, the option pays out. This is structurally the same as selling bitcoin forward at the strike: short selling bitcoin via a put limits loss to the premium paid. Deribit dominates with about 39% of BTC options open interest, but BlackRock's IBIT options briefly overtook it in April 2026 at $27.61 billion.

DEX perpetuals run on smart contracts. They are non-custodial and increasingly liquid (more on that below).

Inverse ETFs like BITI (ProShares Short Bitcoin Strategy) deliver the inverse of BTC's daily return through a regular US brokerage account. No leverage, no funding, no liquidation, but daily-reset compounding makes them poor long-term shorts.

How to short Bitcoin step by step

The mechanics are similar across centralized perp exchanges. The typical flow on Kraken Derivatives or Bybit looks like this. First, fund the spot wallet and transfer collateral (usually USDT or USDC) to the derivatives wallet. Second, find the BTC perp contract (often labeled BTC-PERP or BTCUSDT-PERP). Third, set leverage. A conservative starting point is 2x to 3x, not the headline 100x figure the exchange advertises. Fourth, open a short by placing a sell-to-open order with a stop-loss above your entry; many traders use a 5-10% stop on a 3x position. Fifth, monitor funding payments and price action, then close by placing a buy-to-close order at the new price.

A concrete example. Shorting 1 BTC at $80,000 with 3x leverage requires roughly $26,667 in margin. The position is liquidated if BTC rises to approximately $106,000 (a 33% adverse move). If BTC drops to $72,000, the position closes with about $8,000 in profit, minus exchange fees and any funding paid while holding. If BTC instead rises to $90,000, the loss is roughly $10,000, more than a third of the original margin. That asymmetric outcome is why position sizing matters more than entry timing.

Post-FTX & MiCA: where US/EU traders can short in 2026

The regulatory map has been rewritten twice in two years. After FTX, US enforcement tightened; after MiCA, EU access narrowed.

For US residents, the legal short channels in 2026 are: Coinbase Financial Markets (CFTC-regulated nano BTC and nano ETH perpetual contracts, up to 10x leverage); Kraken Derivatives, which launched US-regulated futures in July 2025 and acquired the CFTC-regulated Bitnomial exchange in April 2026; CME crypto futures and options through any traditional US brokerage; and the inverse ETFs BITI and SBIT (ProShares) for buy-and-hold short exposure without a derivatives account. dYdX explicitly blocks US residents, as do Bybit and most other offshore perp venues.

The SEC and CFTC issued a joint framework on March 17, 2026 that classified BTC, ETH, SOL, and XRP as digital commodities (not securities), placing them squarely under CFTC oversight. That has clarified which US platforms can list which contracts, and pushed Coinbase, Kraken, and CME to expand their US-regulated derivatives offerings.

In Europe, MiCA reached full enforcement on July 1, 2026. Every crypto-asset service provider operating in the EU must now hold a CASP authorization or cease operations. Several offshore exchanges responded by withdrawing EU-resident accounts; others (Bybit, OKX) obtained MiCA licensing for select EU subsidiaries. Using a VPN to access non-licensed venues is a terms-of-service violation almost everywhere and can void access to deposited funds.

| Platform | Jurisdiction | Max leverage | US OK | EU OK | Notes |

|---|---|---|---|---|---|

| Coinbase Financial Markets | US (CFTC) | 10x | Yes | No | Nano BTC/ETH perps |

| Kraken Derivatives | US (CFTC) | up to 50x | Yes | Limited | Bitnomial-licensed |

| CME Group | US (CFTC) | varies | Yes | Yes | Via brokerage |

| BITI / SBIT (ProShares) | US (SEC) | 1x daily | Yes | No | Inverse ETFs |

| Binance | Global (offshore) | up to 100x | No | MiCA-licensed entities only | Largest CEX perp |

| Bybit | Global | up to 100x | No | Select EU only | Heavy retail |

| Hyperliquid | DEX | up to 50x | Mostly no | DEX, varies | On-chain leader |

DEX perps for shorting: Hyperliquid leads on-chain

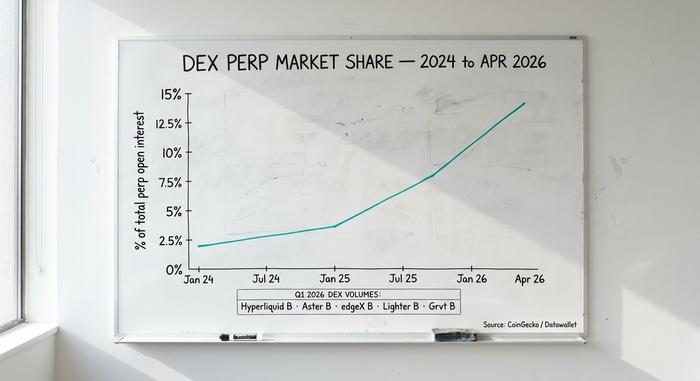

Decentralized perp exchanges have moved from a curiosity to a structural piece of the market. DEX share of total crypto perp open interest rose from 3.6% in January 2025 to 13.5% in April 2026 — close to 4x in fifteen months, a meaningful migration away from centralized venues post-FTX.

Hyperliquid dominates the DEX side completely. In Q1 2026, it processed $619.46 billion in perp volume, capturing roughly 70% of all on-chain perp activity. April 2026 monthly volume was $190 billion, ranking ninth across all venues centralized or otherwise. Annualized fee revenue exceeds $700 million. The HYPE token sits at a $9.9 billion fully diluted valuation. The fee structure undercuts most CEX tiers: a maker rebate of -0.01% and a taker fee of 0.035%.

Other DEX perps are far behind in volume but worth knowing about. Aster recorded $318.7 billion in Q1, edgeX $272.3 billion, Lighter $254.1 billion, Grvt $131.2 billion. dYdX, once the on-chain leader, has fallen out of the top five entirely and now blocks US residents.

The reasons for the shift are not subtle. Post-FTX, traders prefer non-custodial venues where the exchange cannot freeze withdrawals. On-chain order books are auditable in real time. KYC is optional on most of these venues, which appeals to international users locked out of regulated CEXes. The trade-offs are real: smart-contract risk (a bug can drain a venue), wallet UX friction, and gas fees at signing. But for sophisticated short-sellers willing to manage those costs, DEX perps offer better fees and full self-custody.

Liquidation math: how retail short positions blow up

Most retail shorts do not die from being wrong about direction. They die from being right too early, at too much leverage, into a squeeze.

The October 10-11, 2025 cascade was the canonical modern example. Trump's threat of a 100% tariff on Chinese imports triggered a violent whipsaw in crypto: BTC dropped sharply, longs got liquidated, the resulting forced selling drove price lower, then a partial recovery liquidated late shorts on the way back up. Total damage: $19.3 billion in 24 hours, 1.6 million accounts wiped, $3.21 billion in one minute. Other significant events: the August 5, 2024 Bank of Japan yen-carry unwind ($1.2 billion), the December 5, 2024 BTC flash crash from $103,900 to $97,000 ($1 billion+), the February 2025 tariff news ($2.3 billion).

Then there is the slow drain of funding rates. Bitcoin perp funding sits around 0.01% per 8 hours in calm bitcoin market conditions but spiked to 0.04% (roughly 44% annualized) as BTC approached $100,000 in January 2026. A short held through that environment pays the long every 8 hours, every day, until the price actually falls.

Position sizing is where the math gets brutal. A 3x leverage short on Bitcoin is wiped out by roughly a 33% adverse price move. A 10x short dies on a 10% move. A 100x short blows up on a 1% move. Bitcoin routinely moves 4% intraday. The honest rule a serious trader keeps in mind: if losing the entire margin would actually hurt, the leverage is too high.

Risks associated with shorting crypto and the real cost

Shorting has structural risks long positions do not.

First, theoretically unlimited loss. A long position can lose at most 100% (price goes to zero). A short position can lose 200%, 500%, infinitely (price can rise without limit). Real-world short squeezes have wiped out funds.

Second, ongoing cost. Funding rates compound. A 100x perp short held for ten days at 0.02% per 8 hours bleeds about 6% to funding alone, before any price move. Borrow rates on margin shorts run ~0.37% annually on Binance for BTC, higher on smaller venues.

Third, counterparty risk. CEX bankruptcy (FTX, Celsius, BlockFi, Genesis) showed depositors how badly that can end. DEX smart-contract exploits like the April 2026 Kelp DAO incident showed the on-chain version. The risk is different on each side, never zero.

Fourth, taxes. US shorts on derivatives are short-term capital gains, taxed at ordinary income rates. Starting in tax year 2026, Form 1099-DA reporting covers most derivatives venues. Inverse ETFs like BITI compound daily, which means holding longer than a few weeks introduces meaningful tracking error against the underlying — they are tactical instruments, not long-term shorts.

Which short method should you actually use?

Five trader types, five answers. A US retail beginner who wants downside exposure without leverage: BITI or SBIT through a regular brokerage. A US active trader who wants real perps: Coinbase Financial Markets or Kraken Derivatives. An EU or offshore active trader: Bybit, OKX, or Binance with full KYC. A trader who wants non-custodial leverage: Hyperliquid for depth, GMX for simplicity. A HODLer hedging a spot bag: short-dated put options on Deribit, or IBIT puts through a US brokerage. The reminder for everyone: most retail shorts lose money long-term. Use small position sizes, real stop-losses, and only what you can afford to lose.