Short Squeeze Explained: When Shorts Buy Back Stock

Most bets have a floor. Buy a stock and the worst case is zero; you lose what you put in, and not a cent more. Shorting tears that floor out. Bet against a stock and the loss has no ceiling at all, because a price can keep climbing forever. A short squeeze is the moment that missing ceiling turns into a trapdoor. A heavily shorted stock starts to rise, the traders who bet against it scramble to buy it back before the losses get worse, and every one of those panic buys shoves the price higher still. The strange part is who powers the rally. Not the believers. The bears do it to themselves, the people who hated the stock turning into its most desperate buyers.

What a short squeeze is, and short selling

You cannot squeeze a trade you do not understand, so start with the short itself. A short seller borrows shares from a broker, sells them at today's price, and plans to buy them back cheaper later. Sell at $50, buy back at $30, return the shares, keep the $20. The whole position is one bet: this price is going down.

The trouble is always the exit. The shares are borrowed, so they have to be returned, which means buying them back at some point no matter what the price has done. Now flip the bet. The stock that was sold short starts climbing instead of falling. Every short is bleeding, and the only bandage is to buy the stock back. A short squeeze is what you get when a whole crowd of shorts reaches for that bandage at the same moment. Their buy orders are demand. Demand lifts the price. The higher price drags in the next round of shorts, and none of it has much to do with whether the company is any good. Short sellers do earn their keep, to be fair. They hunt frauds and overpriced names and keep the market a little more honest. But the trade has a structural soft spot, and a squeeze is the market pressing on the bruise.

How a short squeeze works, step by step

A short squeeze is a feedback loop, and the fuel is forced buying rather than conviction. Each short seller who covers makes the squeeze worse for the ones still holding on.

The setup: heavy short interest

A squeeze needs a crowd of shorts and not many shares to go around. When a large share of a company's tradable stock has been sold short, the exits are already crowded before anything happens. Add a limited float, the number of shares actually available to trade, and there are simply not enough shares for everyone to buy back at once — that buying pressure alone is enough to drive the price up sharply.

The trigger and the feedback loop

Something lights the fuse: an earnings beat, a surprise announcement, a wave of retail buying, or just a technical move higher. The rising price puts every short position underwater. Brokers issue margin calls demanding more collateral, and traders who cannot or will not post it are forced to buy back the stock. That buying lifts the price again, which triggers the next round of margin calls and covering. The loop feeds itself until the shorts are mostly gone — that self-reinforcing cycle is what defines a short squeeze.

Why short losses can be unlimited

This is the detail that makes a squeeze dangerous. A long position can only fall to zero, so the most you can lose is what you invested. A short position has no such limit, because there is no cap on how high a price can go. A trader who shorted at $20 is down $180 if the stock hits $200, and still owes the shares. Margin calls turn that paper loss into forced action, and forced action is what a squeeze runs on.

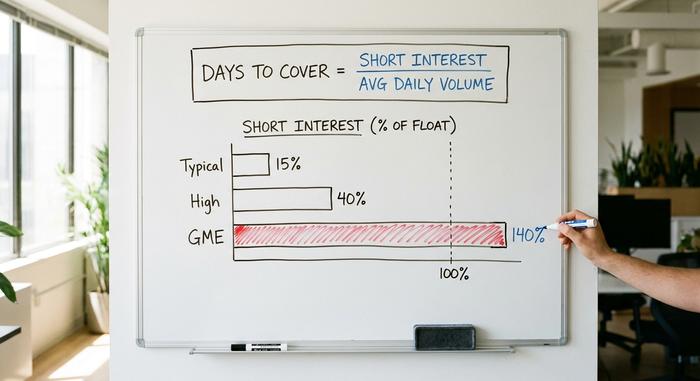

Short interest, days to cover and the float

A handful of numbers tell you how much fuel is sitting around a stock before a short squeeze ignites. None of them predict when one will start, or whether it will happen at all. They only measure the size of the powder keg.

Short interest and percent of float

Short interest is the total number of shares that have been sold short but not yet bought back. Expressed as a percentage of the float, it shows how crowded the short side is. Anything above 10 to 20 percent of float is usually considered high. In extreme cases the figure can pass 100 percent, because the same shares can be borrowed and shorted more than once. GameStop reached roughly 140 percent of its float in early 2021, meaning more shares were sold short than actually existed to trade.

Days to cover (the short interest ratio)

Days to cover, also called the short interest ratio, divides the total short interest by the stock's average daily trading volume. The result is the rough number of trading days it would take for all short sellers to buy back their shares at normal volume. A high days-to-cover number means the shorts are trapped: if they all rush for the exit, there are not enough daily buyers and sellers to absorb them, so the price has to climb to find supply.

Other warning signs

Two more tells matter. A rising borrow fee, the cost of borrowing shares to short, signals that shares are scarce and demand to short is high. A spike in trading volume on an up day, especially in a stock that traders love to hate, can mark the first wave of covering. None of these is a crystal ball. A stock can sit with sky-high short interest for months while the shorts quietly collect, because the people betting against it may simply be right about the business.

| Metric | What it measures | Rough threshold |

|---|---|---|

| Short interest (% of float) | How crowded the short side is | High above 10-20% |

| Days to cover | Days of normal volume to unwind all shorts | High above 5 |

| Borrow fee / utilization | Scarcity and cost of borrowing shares | Rising = tight supply |

| Volume spike on up-moves | First wave of short covering | Sudden, above average |

Famous short squeezes in stock market history

The mechanic is old. Older than the internet, older than the SEC. A cornered float plus a crowd of trapped shorts has produced the same violent spike whether the year was 1901 or 2021.

Northern Pacific (1901) and Piggly Wiggly (1923)

The Northern Pacific Railway got there first, in May 1901. Two rival camps were fighting for control of the railroad and bought so aggressively that between them they held more than 94 percent of the shares. The short sellers who had bet against Northern Pacific went looking for stock to buy back and found almost none. Their scramble briefly launched the price and yanked the rest of the market down with it. Clarence Saunders tried the same move from the other side two decades later. The grocery magnate behind Piggly Wiggly set out to corner his own company's stock and burn the short sellers circling it. He nearly did it, running the price up hard, until the exchange simply halted trading and rewrote the rules against him. Sometimes the house just changes the game mid-hand.

Volkswagen (2008)

For sheer scale, the Volkswagen short squeeze of October 2008 still stands alone. Porsche revealed it controlled around 74 percent of Volkswagen through shares and options, and with another large block held by the state of Lower Saxony, less than 6 percent of the stock was actually free to trade. Short sellers, who had bet VW would fall in a financial crisis, were trapped. The share price rocketed from about €210 to over €1,005 in two days, and Volkswagen briefly became the world's most valuable company at roughly €296 billion. Hedge funds were estimated to have lost around $30 billion.

GameStop and AMC (2021)

The most famous squeeze of all was retail-driven. Short interest in GameStop had climbed to about 140 percent of its float, and traders on the Reddit forum WallStreetBets piled into the stock to force the shorts out. GameStop hit an intraday high of $483 on January 28, 2021, up from under $20 weeks earlier. Melvin Capital, one of the funds short the stock, lost about 53 percent of its value that month and took a $2.75 billion lifeline from Citadel and Point72. AMC, another heavily shorted stock, rode the same wave. The move was amplified by a gamma squeeze in GameStop's call options, and it grew chaotic enough that brokers like Robinhood temporarily restricted buying, a decision that drew lawsuits and Congressional scrutiny.

| Squeeze | When | Move | Short interest | Who got hurt |

|---|---|---|---|---|

| Northern Pacific | May 1901 | Brief spike, market panic | >94% held by two camps | Railway short sellers |

| Volkswagen | Oct 2008 | €210 to ~€1,005 in 2 days | <6% free float | Hedge funds, ~$30B |

| GameStop | Jan 2021 | Under $20 to $483 | ~140% of float | Melvin Capital, -53% |

| AMC | 2021 | Multi-bagger spike | Heavily shorted | Various short funds |

How a short squeeze works in crypto markets

Crypto runs the same play with different equipment. No borrowed shares. No fixed float. No waiting. Just leverage, and leverage changes everything about how fast a squeeze can move.

Liquidations, not borrowed shares

Most crypto shorting happens on perpetual futures: contracts that let you bet against an asset with borrowed money, often twenty or fifty times your own. The catch is the auto-liquidation. Move against a leveraged short far enough and the exchange does not send a polite margin call. It closes the position for you, buying the asset back at market. That forced buy lands as demand, the price ticks up, and the next short over the line gets liquidated too. Same loop as a stock squeeze, minus the manners. Funding rates are the tell. When the periodic payment between longs and shorts on a perp flips hard, the crowd is piled onto one side, and a small shove can topple all of them at once. Two details make crypto squeezes nastier than the stock kind. Leverage means a five percent move can erase a position outright. And nothing ever closes, so there is no opening bell, no circuit breaker, no overnight pause to let the panic cool.

A real one versus a cascade in 2025

The labels get mangled constantly, so here is the difference in two dates. March 15, 2025 was a genuine short squeeze: around $470 million liquidated in a day, 83 to 86 percent of it shorts, spread across Bitcoin, Ethereum, and Solana. October 10, 2025 was not. That day about $19 billion vanished across 1.6 million accounts, but roughly 88 percent of the wiped positions were longs. That is a long-liquidation cascade, the mirror image of a squeeze. Both look like chaos on a chart. Only one is a short squeeze. The full-year tally for 2025 crossed $150 billion in liquidations, which tells you how routine this kind of violence has become.

Is a short squeeze market manipulation?

A short squeeze on its own is not illegal. Buying a stock you believe is underpriced, even buying it specifically because you know the shorts are trapped, is legal trading. The line is crossed only when buyers coordinate to spread false information or run a pump-and-dump, which is market manipulation under existing securities law. The irony of 2021 is that the rules were already in place. Short selling had been governed by the SEC's Regulation SHO since 2005, and the agency's later staff report found no evidence that illegal naked shorting drove the GameStop move. The Congressional hearings that followed produced plenty of headlines but no major new legislation. What the episode really exposed was how far a stock price can detach from any fundamental value when a squeeze takes over, the so-called meme-stock disconnect.

Can you trade a short squeeze safely?

Spotting the fuel is not the same as timing the spark. The metrics can tell you a stock is heavily shorted, but they cannot tell you when, or whether, a squeeze will ignite, and a stock can stay crowded with shorts for months without moving. The harder problem is the exit. Squeezes are short-lived and reverse hard once the covering is done, and most retail buyers arrive after the spike is already underway, then hold through the collapse. The honest summary is that a short squeeze is thrilling to watch and brutal to trade. If you do not have a plan for when you are wrong, the round trip can hurt as much as being the short seller did. Is the next squeeze worth chasing, or just worth understanding? For most people, the answer is the second one.