ASTS Stock: AST SpaceMobile’s Satellite Bet in 2026

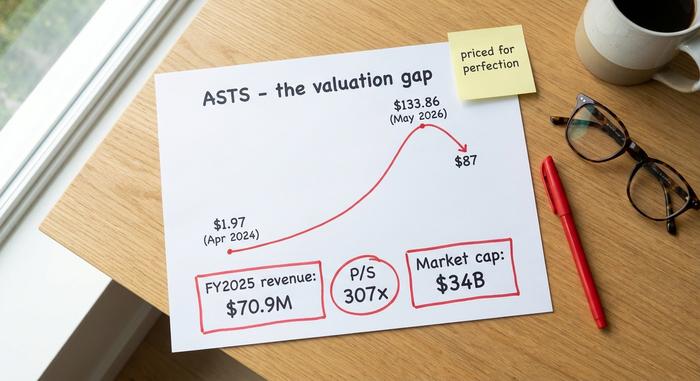

A stock that changed hands for under $2 in the spring of 2024 now carries a price tag above $34 billion, books less annual revenue than a single mid-size car dealership group, and earns an average rating from Wall Street analysts of, almost literally, "reduce." Not many tickers capture the distance between a thrilling story and a demanding price as cleanly as ASTS stock. That distance is the whole subject of this article.

AST SpaceMobile trades on the Nasdaq under the symbol ASTS, and it is one of the most divisive names in the market. This guide walks through what the company actually does, how the stock ran so far so fast, what the financials really say, the bull and bear cases side by side, where analysts stand, and the launch catalysts that will move it. None of it is investment advice; it is the context you need to form your own view.

What AST SpaceMobile actually does

The pitch behind AST SpaceMobile is genuinely big. The company is building a cellular broadband network in space that beams connectivity straight to an ordinary, unmodified smartphone. No dish, no special terminal, no satellite handset. If it works at scale, the phone already in your pocket connects to a satellite the same way it connects to a cell tower, which is the one thing Starlink's dish-based service cannot do for a normal handset.

The hardware doing this is a line of large satellites called BlueBird, flying in low Earth orbit. AST does not sell directly to end-users; it works through mobile carriers, who fold satellite coverage into their existing plans to fill the dead zones their towers miss. Sold this way, AST's broadband services are less a rival to the carriers than an extension of them, plugging satellite cellular coverage into the gaps between towers where almost nobody has a signal today. The company was founded and is led by Abel Avellan, runs its manufacturing out of Midland, Texas, and employs more than 2,250 people across some 500,000 square feet of factory space. For all that scale on the ground, only about six satellites were operational in orbit by mid-2026 — which is precisely why ASTS stock trades on belief in a future network rather than current output.

ASTS stock: from $2 to a $34B company

The ASTS chart is not a story about earnings. It is a story about a narrative being repriced, fast. Shares went for about $1.97 in April 2024. By late May 2026 they touched an all-time high of $133.86, then settled near $87 by June. Call it a fortyfold move in two years, at a company whose revenue is still a rounding error beside its market cap.

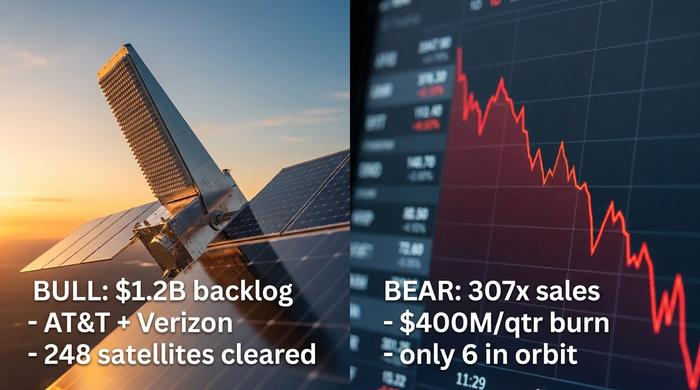

What drove it was credibility, not profit. Strategic investments and commercial deals from AT&T, Verizon, Vodafone, Google, and Rakuten. A long-term spectrum agreement with Ligado that handed the project a real moat. A contracted backlog north of $1.2 billion. Then add the retail crowd that has chased space stocks all year, plus a short interest near 18% of the float, and you get a security that lurches both ways on a single headline. The price reflects belief in a future network, not the trickle of cash arriving today.

| ASTS metric (as of June 2026) | Value |

|---|---|

| Share price | ~$87 |

| Market cap | ~$34B |

| 52-week range | $34.21 – $133.86 |

| All-time high | $133.86 (May 2026) |

| Shares outstanding | ~388M |

| Price-to-sales ratio | ~307x |

ASTS financials and earnings reality

Here the income statement and the market cap are barely on speaking terms. For anyone holding or watching ASTS stock, one question matters financially: does the cash last until the satellites start paying their way?

Revenue, losses, and cash burn

Revenue is growing off a tiny base. Full-year 2025 came in around $70.9 million, up from just $4.42 million in 2024. Explosive growth, until you hold it against a $34 billion valuation. Then the first quarter of 2026 landed with a thud. Revenue of $14.7 million missed the $37 million consensus by about 61%, with a net loss near $191 million. For all of 2025 the company lost roughly $461 million, and it burns more than $400 million a quarter. There is a cushion: about $3.5 billion in cash at the end of March 2026. Set against it sits roughly $2.97 billion in long-term debt.

| Period | Revenue | Net loss |

|---|---|---|

| FY 2024 | $4.42M | — |

| FY 2025 | $70.9M | $461M |

| Q1 2026 | $14.7M | $191M |

Dilution and how the build is funded

A satellite constellation is brutally expensive, and AST has paid for it mostly by printing shares. The count is up something like 437% over five years, through at-the-market offerings and convertible notes, so every holder owns a steadily smaller slice. The Ligado spectrum deal came via a $550 million non-recourse loan parked in a separate entity, which keeps that debt off the main balance sheet without making it free. And insiders sold roughly $280 million of stock in one recent three-month stretch. Bulls and bears read that last fact very differently.

Backlog and forward guidance

The case for paying up rests on what is coming. Management points to the $1.2 billion-plus backlog, guides for $150 to $200 million of revenue in 2026, and has floated a 2027 target "approaching $1 billion." Hit those, and today's price looks less absurd. Miss them, as Q1 shows it can, and the gap between valuation and reality widens fast. The whole trade is a bet that the guidance is roughly right.

The bull and bear case for ASTS stock

Both sides of this trade are strong, which is exactly why the stock is so volatile. Reasonable, well-informed people look at the same facts and land in opposite places. It is worth laying both out plainly.

The bull case for ASTS

The bull case is about a moat and a head start. The Ligado agreement gives AST access to up to 45 MHz of premium lower mid-band spectrum across North America on an 80-year basis, a scarce asset rivals cannot easily copy. It has signed roughly 60 mobile network operators covering more than three billion subscribers, with names like AT&T and Verizon that have both partnered and invested. The FCC has cleared it to deploy up to 248 satellites, it has a foothold in defense work through a US Missile Defense Agency contract, and it is, for now, the clearest first mover in direct-to-device broadband. If the technology scales, the addressable market is much of the planet.

The bear case for ASTS

The bear case is about price and execution. A roughly $34 billion valuation on about $85 million of trailing revenue is a price-to-sales ratio near 307, a number that leaves no room for stumbles. The company burns over $400 million a quarter, carries nearly $3 billion in debt, and dilutes shareholders to keep the lights on. Only about six satellites are actually in orbit. After a 61% revenue miss and the loss of a satellite during launch, the risk that execution simply takes longer and costs more than the price assumes is not theoretical; it is the base rate for hardware this ambitious.

The SpaceX and Starlink question

Then there is the elephant. SpaceX's Starlink Direct to Cell is chasing the same idea with vastly more launch capacity, and when SpaceX filed to go public in 2026 under the ticker SPCX, its prospectus named AST SpaceMobile as a competitor. Bulls read that as validation of the market; bears read it as the arrival of a rival that can out-build almost anyone. Lynk Global and the Globalstar partnership behind Apple's emergency texting are circling the same space. AST's counter is that its large satellites aim at true broadband to a standard phone, not just basic messaging, but it is competing against the most capable launch company on Earth.

| Bull case | Bear case |

|---|---|

| Ligado spectrum moat, 80-year access | ~307x price-to-sales, no margin for error |

| 60+ carriers, 3B+ subscribers, big-name investors | >$400M/quarter burn, ~$3B debt, heavy dilution |

| FCC cleared for 248 satellites; defense contracts | Only ~6 satellites live; Q1 miss and a lost launch |

| First mover in direct-to-device broadband | SpaceX Starlink scale and the SPCX IPO |

Analyst ratings and forecast for ASTS

The professionals are, on average, telling you the price has already run past them. The analyst consensus on ASTS sits between "hold" and "reduce," and the average price target, around $81, is actually below where the stock trades. A target beneath the current price is unusual, and I would sit with that signal rather than dismiss it. The spread is enormous, from roughly $45.60 at the bearish end (Scotiabank) to $108 at the bullish end (Roth MKM), which is another way of saying nobody really knows.

Sentiment on the stock is as divided as the targets, and the split runs through the individual calls too: Roth has stayed positive on the strength of the technology, Deutsche Bank moved to the sidelines after the Q1 revenue miss, and Barclays has a sell. Roughly 18% of ASTS stock's float is sold short, so there is real money positioned against the story. For an investor, the message in the consensus is caution, even where the believers are louder and the headlines are brighter. Price targets are guesses dressed as numbers, and on a pre-revenue space stock they are guesses with very wide error bars, but the direction of the consensus is a signal worth weighing.

BlueBird satellite launches and catalysts

For a pre-revenue space company, the catalysts are refreshingly physical. Rockets reach orbit or they do not. And 2026 is wall-to-wall launches, so the market trades every one. Next up: BlueBirds 8, 9, and 10, set to fly on June 17, 2026, aboard a SpaceX Falcon 9 from Cape Canaveral.

The launches also carry the clearest risk. BlueBird 7 was lost in April 2026 when Blue Origin's New Glenn rocket dropped it in the wrong orbit. The write-off ran $155 to $160 million, only partly insured. A blunt reminder that this is rocket science. The goal is roughly 45 satellites in orbit by the end of 2026. It flies six today. That is a steep climb. The newer Block 2 satellites help, because they are far bigger, arrays around 2,400 square feet, about three and a half times the last generation, and the network has already clocked peak speeds near 99 Mbps in testing. A TELUS deal aims to reach Canada by late 2026, another milestone ASTS stock watchers will be tracking. Each launch that works tightens the story. Each one that fails reopens it.

How to invest in ASTS stock and ETFs

The mechanics are simple. AST SpaceMobile stock trades on the Nasdaq under the ticker ASTS, so any standard brokerage account can buy or sell it the same as Apple or Ford. One warning. Leveraged single-stock ETFs now track it, like the 2x daily products under tickers such as ASUP and LITU. Those are short-term trading tools that decay over time, not buy-and-hold investments, and they magnify a name that is already wild. ASTS can swing double digits on a single launch, so how much you own matters as much as whether you own it at all. Again, this is general information, not a recommendation to buy or sell anything.

The bottom line on ASTS stock in 2026

AST SpaceMobile is a real company with a real moat and a price that already assumes near-flawless execution. That is an uncomfortable combination, because it means the upside requires the bull case to mostly come true while the downside only requires the schedule to slip. The next twelve months of launches, and the first quarter where commercial revenue actually shows up at scale, will decide whether the valuation grows into itself or unwinds. If you are looking at ASTS stock, the honest question is not whether the technology is impressive, it clearly is, but whether you are being paid enough for the execution risk you are taking on. Answer that one for yourself before the next launch does it for you.