ROI Meaning: How to Calculate Return on Investment

A vending machine that "earns 30%" and a token that doubled in a year both wear the same label. The label is ROI, and it is the most quoted, least understood number in all of investing. In traditional finance it usually behaves itself. In crypto it does not.

This guide covers what ROI means, the formula behind it, and how to calculate return on investment on a real crypto trade. Then it covers the harder part: what a good ROI actually is, and the four things this tidy little metric quietly hides from you. Bitcoin makes a useful teacher here, because it pushes every weakness of ROI to the surface.

What ROI Means and What It Actually Measures

ROI stands for return on investment. It is a single ratio that tells you how much profit or loss an investment produced relative to what it cost you. Nothing more.

That word "relative" is the whole point. ROI does not measure dollars; it measures efficiency. If you put in $1,000 and walk away with $1,200, your profit is $200 and your ROI is 20% — a positive ROI. Read literally, a 20% return on investment means you earned 20 cents for every dollar you committed. A negative ROI means the opposite: lose half your money and you are sitting at -50%.

Here is where people trip. ROI is not a rate of return over time. It says nothing about whether that 20% took you a week or a decade. As a financial metric it is closer to a snapshot than a speedometer. A profitability ratio tells you whether you came out ahead; an annual rate of return tells you how fast. People quote the first and assume the second. That gap between profit ratio and time matters everywhere, but in crypto, where prices can move 20% before lunch, treating ROI as a yearly yield is how investors fool themselves. The number is honest. The reading is often wrong.

The ROI Formula and How to Calculate ROI

Here is the good news: the ROI formula is simple enough to scribble on a napkin. The hard part was never the math. It is being honest about the two numbers you feed it.

The basic ROI formula

The basic ROI calculation:

ROI = (net profit / cost of investment) × 100

Net profit is just what you walked away with minus what you put in. Cost of investment is sneakier than it looks. It is your initial investment plus every fee, tax, and expense bolted onto it — the full investment cost, not the sticker price. (Some people plug in net income instead of net profit. Same thing.) Out pops a percentage. And percentages are what let you stack a token next to a stock next to a rental and actually compare them.

How to calculate ROI on a crypto trade

Now a real one. You buy a Bitcoin at $40,000 and sell it later at $52,000. Twelve grand of profit, so 30%, right? Not so fast. The two trades cost you about $200 in exchange and network fees. That nudges your true cost of investment to $40,200 and trims net profit to $11,800. So: ($11,800 / $40,200) × 100 = 29.4%. Close to 30. Not 30.

Two hundred dollars feels like a rounding error. It is not, especially if you trade often or trade small. On a $200 buy, fees can swallow the entire gain. Honest crypto ROI counts the gas, the spread, and the exchange's cut. Leave them out and the calculation is just a flattering story you tell yourself.

ROI on staking and yield

Crypto bolts on a second engine that stocks rarely hand you directly: yield. Stake your tokens and the rewards pile onto your proceeds. As of January 2026, Ethereum's network staking pays roughly 3.3% APY, according to Datawallet, while Solana's native staking runs 5.75% to 6.5%, with liquid-staking tokens pushing a bit higher. Solana shows how normal this has become. About 68% of its supply sits staked, the highest share of any large proof-of-stake chain.

Keep the two engines apart in your head. Price appreciation is one return. Staking yield is another. Stake $10,000 of ETH for a year at 3.3% with a flat price and your yield ROI is about $330. Let the price climb 20% on top and total ROI jumps near 23%. Stack them for the full picture. Just never mistake a calm 5% yield for protection against a price that can drop 50% in a quarter.

What Counts as a Good ROI in Crypto

"What is a good ROI?" is the question everyone asks and almost nobody frames correctly. A good ROI is meaningless without a benchmark and a time frame.

Start with the benchmark. From 1928 to 2024, the S&P 500 returned about 10.2% a year on average with dividends reinvested. That is the bar. Any crypto position has to clear roughly 10% annually just to match a boring index fund, and it has to clear it after you account for how much stress you took on to get there. Once you adjust for risk, a lower ROI from a calmer asset can quietly beat a flashier one.

The good news is that, often, it does. A 2026 consumer survey found that 53% of US crypto holders were sitting on net gains, against 21% with net losses and 23% roughly breaking even. So crypto is not a guaranteed loss machine.

Chasing the highest ROI is its own trap, though. In 2024 the top gainer, Virtuals Protocol, returned more than 23,000%, per CoinGecko Research, a number that looks life-changing on a chart and ruins people in practice, because almost nobody buys at the bottom and sells at the top, and for every Virtuals there are a thousand tokens that quietly went to zero. The survivors get screenshotted; the corpses do not. Notice, too, that "good" still depends entirely on when you bought. The highest ROI in the market and the worst loss in the market can belong to the same asset in back-to-back years. Compare different investments on ROI all you want; just compare them over the same window, or the comparison is theater.

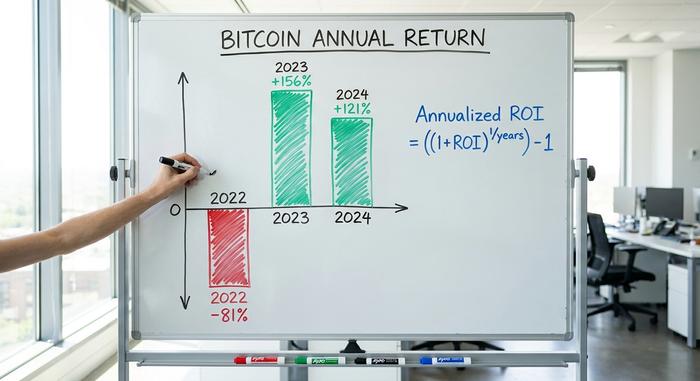

Annualized ROI and Why Timing Changes It

A raw ROI with no clock attached is half a truth. Annualizing is the fix, and Bitcoin makes the case better than any textbook. Look at three years back to back:

| Year | Bitcoin annual return |

|---|---|

| 2022 | -81% |

| 2023 | +156% |

| 2024 | +121% |

Same asset. Same code. Three completely different lives, decided by nothing but the day you happened to buy. That is the uncomfortable lesson here: entry timing, not the asset itself, separated the winners from the bag-holders.

So you annualize. It rewrites a lump-sum ROI as a yearly equivalent:

Annualized ROI = ((1 + ROI)^(1 / years)) − 1

A 200% gain sounds like generational wealth, right up until you hear it took ten years. Annualized, that is about 11.6% a year. Barely past a boring index fund. A clean 50% in a single year beats it handily. So when someone flashes a monster crypto ROI and skips the timeline, do the quiet division yourself. The number tends to deflate.

How to Compare Investments Using ROI

ROI's best trick is putting wildly different assets on one ruler. A stock, a rental property, marketing campaigns, a bag of tokens — all of them collapse into a single comparable percentage. The catch: the ruler only works if you measure each over the same window, with the same costs counted.

Here is 2024 across a deliberately mismatched lineup:

| Asset | 2024 return | Typical yield | Risk profile |

|---|---|---|---|

| Solana (SOL) | +493% | 5.75-6.5% staking | Very high volatility |

| Bitcoin (BTC) | +134% | None | High volatility |

| Ethereum (ETH) | +53% | ~3.3% staking | High volatility |

| S&P 500 | ~+25% | ~1.3% dividend | Moderate |

| US savings account | ~4% | 4% interest | Near zero |

Scan it top to bottom and crypto looks untouchable. That is the trap, baited and set. One green year hides the 80% drawdowns crypto hands you in the red ones, and it ignores that a savings account has never once lost a cent. Two more wrinkles wreck lazy comparisons. Most tokens pay no dividend, so the entire return rides on price. And crypto never closes; it trades 24 hours a day, seven days a week, while the stock index clocks out on Friday afternoon. Same percentage, completely different ride. ROI compares investments. It will never compare the sleep you lose holding them.

The Limitations of ROI Every Investor Misses

ROI's simplicity is also its trap. As a measure of profitability it is excellent. As a complete decision tool it is dangerous, because it ignores four things, and crypto magnifies every one.

First, time. We covered this; raw ROI is blind to it, which is why internal rate of return (IRR), net present value (NPV), and payback period exist. IRR and NPV fold the time value of money into the math where plain ROI refuses to; payback period at least tells you how long your cash is tied up.

Second, risk. A 30% ROI from a Treasury bond and a 30% ROI from a memecoin are not the same achievement. Risk-adjusted measures try to capture this. From 2020 to 2024, Bitcoin's Sharpe ratio came in around 0.96, beating the S&P 500's 0.65, with a Sortino ratio near 1.86. That is the strongest rebuttal to "crypto is just gambling," and it is exactly the context ROI alone will never give you.

Third, taxes, fees, and inflation. ROI quoted before tax overstates what you keep. Sell a token at a gain and the IRS wants its share; that tax is part of the real cost of being in the trade. Inflation chips away at the rest: a 10% ROI in a year when prices rose 4% is really closer to 6% in purchasing power. Plain ROI never makes that adjustment for you.

Fourth, and most brutal in crypto: realized versus unrealized. A paper ROI is not money. If your token showed +300% and then the protocol got drained in a hack, or you simply held through an 80% drawdown, that ROI was never yours. The number on the screen and the number in your bank are different numbers until you sell. I have watched people quote gains they never once locked in.

How to Use ROI Effectively in Decisions

Use ROI as a screening tool, never as a verdict. It is the back-of-the-envelope number that tells you which ideas deserve a closer look, not which ones to bet the house on.

A few habits make ROI trustworthy in crypto:

- Count every cost: gas, exchange fees, spreads, and tax. Hidden costs are where ROI lies.

- Annualize before you compare. A time frame turns a vanity number into a real one.

- Check the drawdown, not just the peak. Survivable beats spectacular.

- Separate realized gains from paper gains. Only the first kind pays your rent.

Do that and ROI becomes what it should be in any investment decision: a fast, honest first filter, not the final word.

What ROI Can and Cannot Tell You

ROI is a starting line, not a finish line. It tells you, cleanly and quickly, whether an investment made or lost money relative to its cost. That is useful, and you should use it.

What it cannot tell you is whether the gain was worth the risk, how long it took, or whether you will ever actually collect it. In crypto, those three blanks are the whole game. So treat the percentage as the first question, never the last. Next time a token's ROI makes your eyes widen, ask the boring follow-up: over how long, and at what risk?