Payment Networks: Types, How They Work, and Real-Time Payments

Visa processed 233.8 billion transactions in 2024. That's $13.2 trillion moving through one network alone. The actual infrastructure behind each of those transactions — the system that decides whether a payment goes through, routes the request, and moves money from one bank to another — is the payment network.

Payment networks are what merchants rarely think about until something goes wrong. They're the infrastructure layer connecting financial institutions, merchants, and consumers. Each network sets its own rules for authorization, clearing, and settlement, and those rules determine fees, dispute rights, and settlement timelines.

This guide covers the four main types of payment networks, how each operates from authorization to settlement, what each one costs merchants, and when a crypto network offers a better option than the traditional payment system.

What Is a Payment Network?

The term gets confused with payment processor. They're different. A payment processor routes the message. A payment network owns the rails and moves the funds. The processor speaks to the network; the network speaks to the banks.

Every card transaction runs through four parties: the cardholder, the merchant, the acquiring bank (the merchant's bank), and the issuing bank (the cardholder's bank). The network sits between the last two. It routes the authorization request in and the approval decision out, then coordinates the settlement of funds after the fact.

Every card transaction involves four parties:

- Cardholder — the consumer initiating the payment

- Merchant — the seller accepting the payment

- Acquiring bank — the merchant's bank that requests funds

- Issuing bank — the cardholder's bank that approves or declines

For merchants, the network choice matters because it determines which credit cards and debit cards you can accept, what the chargeback rules look like, and what share of every transaction gets taken in fees.

Types of Payment Networks Explained

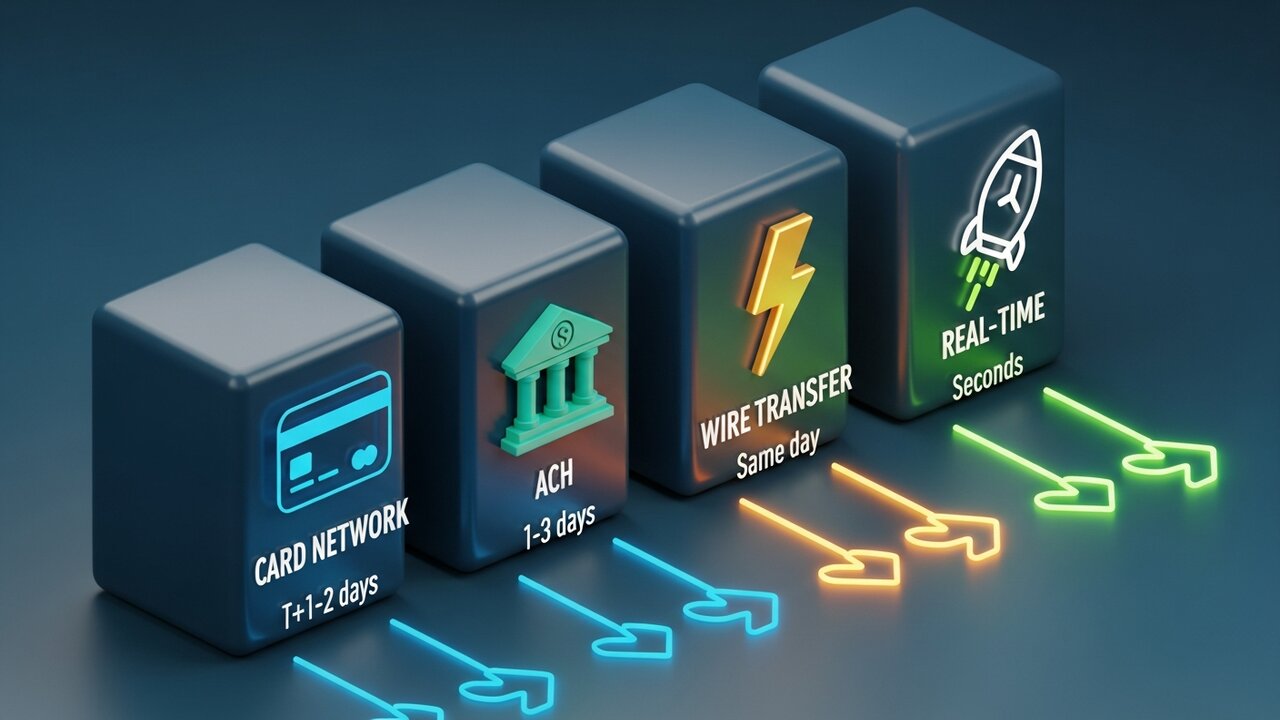

Payment networks fall into four main categories, each a distinct payment method built for a different use case. Speed, cost, and reversibility are where they diverge most.

| Network type | Speed | Typical cost | Reversible | Best for |

|---|---|---|---|---|

| Card network | Seconds (auth) / T+1–2 (settlement) | 1.5–3.5% | Yes (chargebacks) | Consumer purchases |

| ACH | 1–3 days (same-day option) | $0.20–$1.50 flat | Yes (within window) | Payroll, recurring billing |

| Wire transfer | Same day (domestic) | $15–$50 | No | Large one-time transfers |

| Real-time payments | Seconds | $0.01–$0.045 | No | Instant B2B, gig pay |

| Crypto blockchain | Minutes | 0.5–1% | No | Cross-border, high-fraud categories |

Most consumer transactions run through card networks. Visa and Mastercard operate as open-loop systems — they license their brand to thousands of banks, which then issue cards. Credit cards under these two brands account for the bulk of retail electronic payment volume. American Express and Discover take the opposite approach: they issue cards directly. The economics are different (they keep more per transaction), but merchants pay a higher rate.

Then there's ACH, the US bank-to-bank funds transfer network that handles direct deposits, payroll, and recurring billing. $86.2 trillion moved through it in 2024. Settlement is slower — 1–3 business days, though same-day ACH exists — but the cost structure is fundamentally different from cards. Flat per-transaction fees, not percentages. That makes ACH significantly cheaper than credit cards or wire transfers for large-ticket business payments.

Wire transfers sit at the opposite extreme. CHIPS for domestic, SWIFT for international payments, SEPA for European funds transfer. Same-day domestic settlement, completely irreversible. You pay $15–$50 domestically, more internationally. The cost reflects the finality — no reversals, no disputes, money moves and stays moved.

Real-time payment networks are the newest addition and the fastest growing. RTP, FedNow, SEPA Instant — they all settle in seconds, 24/7, with no overnight batch window. B2B disbursements, gig economy payouts, insurance claims — anything where a 2-day wait has actual consequences.

How Payment Networks Work

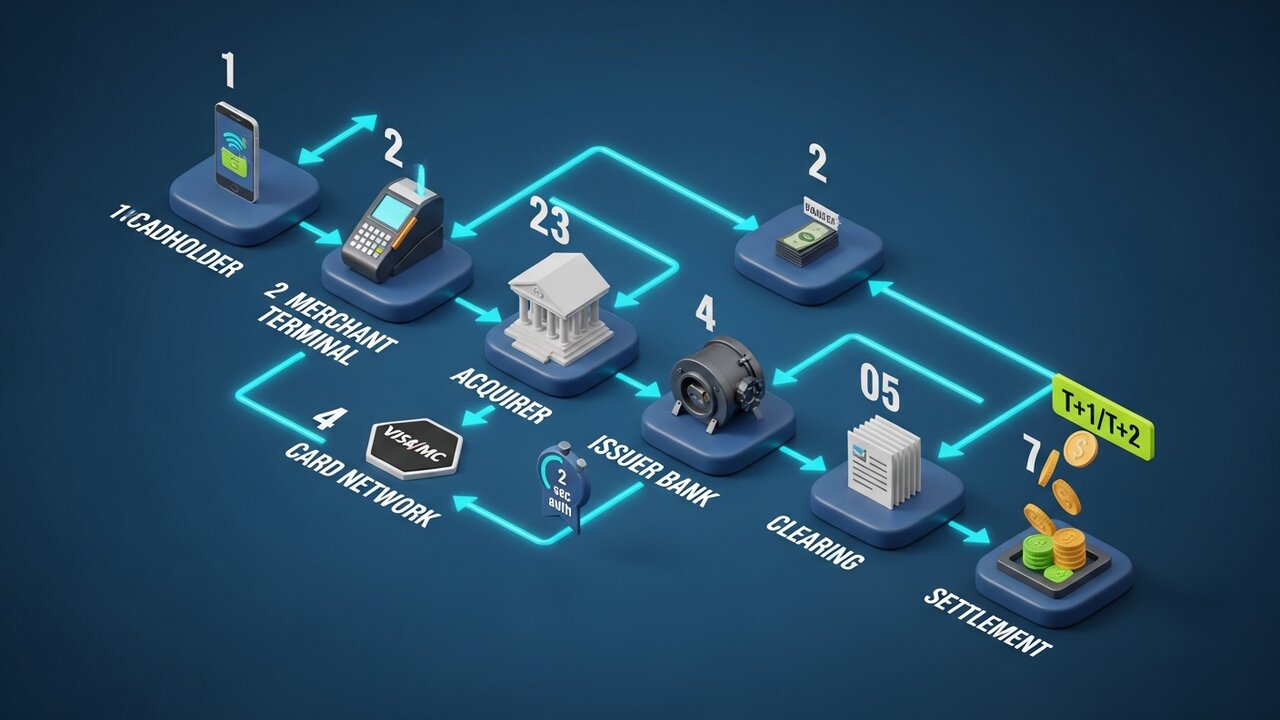

Every card transaction moves through three phases before money actually changes hands. Understanding this sequence explains why authorization is instant but settlement takes days.

The process runs in seven steps:

- Initiation — the cardholder presents their card at the merchant's point of sale or enters card details online

- Authorization request — the merchant's payment processor sends transaction details to the acquiring bank

- Network routing — the acquiring bank forwards the request to the appropriate card network (Visa, Mastercard, etc.)

- Issuer check — the network routes the request to the issuing bank, which checks available credit, fraud signals, and account status

- Authorization response — the issuing bank approves or declines; the decision travels back through the network to the merchant terminal in approximately 2 seconds

- Clearing — at end of day, transaction details are batched and sent through the clearing house for reconciliation

- Settlement — the final funds transfer moves money from the issuing bank through the network to the acquiring bank and into the merchant account, typically T+1 or T+2 business days

Most people think authorization is the payment. It isn't. Authorization is permission. The actual money movement comes later, which is why card transactions take days to settle even though approval happens in two seconds.

Tokenization handles data protection throughout. The real card number never travels the full path. Each hop substitutes a unique token for the actual account details — that's why a breach at a merchant level rarely results in real card number exposure.

The Four Major Card Networks

Visa and Mastercard together control approximately 87% of global credit card market share. Credit cards under these two networks are accepted in more countries and by more merchants than any other payment method. The other two major networks operate at a fraction of that volume.

| Network | US market share | Annual volume (2024) | Network model | Chargeback window |

|---|---|---|---|---|

| Visa | 61.6% | $13.2 trillion | Open-loop | 120 days |

| Mastercard | 25.7% | $4.4 trillion | Open-loop | 120 days |

| American Express | 10.5% | $1.8 trillion | Closed-loop | 120 days |

| Discover | 2.2% | $224.6 billion | Closed-loop | 120 days |

Visa leads on global acceptance. With 40% global market share and operations in over 200 countries, it has the widest reach of any card payment network.

Mastercard is close behind on global coverage but stronger in certain European and emerging markets.

American Express targets premium cardholders. Because AmEx operates as both network and issuer, it captures more of each transaction but charges merchants a higher acceptance rate. Average AmEx cardholder spending runs higher than Visa or Mastercard users, which is why many merchants accept it despite the cost.

Discover has the smallest US footprint among the four major networks. Interoperability agreements with China UnionPay expand its acceptance across Asia.

Real-Time Payment Networks

Traditional card networks authorize instantly but settle in 1–2 days. Real-time payment networks collapse that gap entirely. Funds arrive in the recipient's account within seconds.

Three real-time systems matter most for US merchants and businesses:

- RTP (Real-Time Payments) — launched 2017 by The Clearing House, a private bank consortium. Handles up to $10 million per transaction. Widely adopted by large US banks.

- FedNow — launched July 2023 by the Federal Reserve. Open to all US banks and credit unions, including community institutions that couldn't connect to RTP. Limit of $500,000 per transaction.

- SEPA Instant — the European equivalent, covering 25 countries with 10-second settlement and a €100,000 limit per transfer.

Real-time payment networks eliminate float risk. Money settles immediately rather than sitting in clearing for 24–48 hours. That makes them ideal for insurance claim payouts, gig economy worker payments, and B2B invoice settlement where the other party needs funds today, not Thursday.

The trade-off matters: real-time networks use push-based transfers, where the sender initiates rather than the receiver. Once sent, the payment is final. No chargeback mechanism, no dispute window. That's a feature for merchants but a genuine risk for consumers paying unfamiliar vendors.

Payment Network Fees: What Merchants Pay

Every card transaction carries three layers of fees. Most merchants see a single blended rate from their processor, but the underlying structure determines what you're actually paying.

Interchange fee is paid to the issuing bank (the cardholder's bank). The card network sets the rate, it's not negotiable, and it varies by card type. Standard consumer credit runs 1.5–2.0%. Rewards and business cards: 2.0–2.5%. Debit cards: 0.05–0.5% plus a flat fee, regulated under the Durbin Amendment for large US banks.

Assessment fee goes to the card network itself. Visa charges 0.14% on credit transactions; Mastercard charges 0.13–0.15%. Small percentages, but applied to total volume. On $1 million in monthly sales, that's $1,400 going directly to the network.

Processing fee goes to the acquiring bank or payment processor. Typically $0.05–$0.30 per transaction plus a small percentage.

ACH is structurally different. No percentage-based interchange, just flat fees of $0.20–$1.50 per transaction regardless of amount. On a $10,000 B2B invoice, ACH costs a few dollars. The same payment via credit cards at 2.5% costs $250. For high-ticket recurring transactions, the choice of payment method has real cash flow implications — it's not just a payment system preference, it's a cost decision.

Wire transfer costs are fixed: $15–$50 for domestic, $20–$50+ for international. The premium buys same-day finality.

How to Choose a Payment Network

The right payment network depends on your transaction profile. No single network optimizes for everything.

- Transaction size matters — card networks are efficient for low-to-mid ticket consumer purchases; ACH beats them on cost for anything over $200 where a percentage fee becomes painful

- Geographic reach — for international payments, card networks (Visa/Mastercard) have the widest acceptance; crypto networks handle cross-border without currency conversion or SWIFT fees

- Speed requirements — real-time payment networks for immediate settlement (gig payouts, insurance claims, time-sensitive B2B); ACH if 1–2 day settlement is acceptable and cost is the priority

- Chargeback exposure — businesses selling digital goods, travel, or high-value services face elevated chargeback risk on card networks; ACH, wire, and crypto networks are irreversible by design

- Customer base — consumer-facing retail must accept credit cards and debit cards as the default payment method; B2B and subscription businesses can often substitute ACH for a fraction of the cost

Most businesses end up using multiple payment networks simultaneously, accepting Visa and Mastercard for consumer purchases, ACH for recurring billing, and potentially crypto for international payments or high-risk category sales. Each is a separate payment system with its own rules, but they run in parallel without conflict.

Crypto Payment Networks and Blockchain

Card payment networks are built on a fundamental assumption: transactions can be reversed. An issuing bank can initiate a chargeback weeks after a purchase. The network enforces it. The merchant has no veto.

Blockchain payment networks work on the opposite premise. Once a Bitcoin, Ethereum, or stablecoin transaction is confirmed, no party can reverse it. There's no clearing house, no issuing bank, no chargeback mechanism. The peer-to-peer architecture removes the intermediary entirely. Funds move directly between wallets without passing through a financial institution.

The merchant implications are concrete:

- Zero chargeback exposure — no dispute window, no forced reversals, no $15–$100 dispute fees

- Settlement in minutes rather than T+1/T+2 business days

- International payments without SWIFT fees or currency conversion spreads — funds transfer settles in minutes at a fraction of wire costs

- Tokenization is native — wallet addresses substitute for sensitive payment data automatically

Crypto networks have real limitations. Customer adoption is lower than cards, and consumer-facing refunds require manual outgoing transactions rather than an automated reversal process. But for the right business type, those are manageable trade-offs.

For businesses dealing with high chargeback exposure — digital goods, subscription software, travel, high-ticket items — adding crypto to the payment stack has a direct financial case. Plisio lets merchants accept Bitcoin, Ethereum, USDT, USDC, and 20+ other assets at checkout with transaction fees starting at 0.5%. No chargebacks, instant settlement, and blockchain as the payment network means no intermediary taking a percentage of every transaction.

Conclusion

Payment networks are the infrastructure that determines how fast money moves, what it costs, and who controls the transaction after it's sent. Card payment networks handle most consumer commerce but carry the highest fees and the most dispute exposure. ACH is the workhorse for high-volume, lower-cost business payments. Real-time payment networks are closing the gap between authorization and settlement, delivering funds in seconds instead of days.

For merchants evaluating their payment stack, the choice of payment networks comes down to transaction size, geographic reach, speed requirements, and chargeback risk. Most businesses need at least two: one card network for consumer-facing sales, and something cheaper and faster for recurring or B2B transactions.

When card network chargebacks become a structural problem — digital goods, travel, international sales — blockchain payment networks offer a different architecture entirely. No intermediaries, no reversals, settlement in minutes. Understanding payment networks at this level is what separates businesses that control their transaction costs from those that accept whatever their processor charges.