Merchant Transaction Number, Merchant ID, and Reference Number Explained

Pull up a payment receipt and you'll find at least three different numbers staring back at you. Ask your processor about a failed transaction and they'll want one more. The merchant transaction number isn't a single thing — it's a family of identifiers, assigned by different parties for different purposes in payment processing.

Merchants who can't tell a Merchant ID from a Merchant Reference Number from a Transaction ID cause themselves real headaches: botched chargebacks, reconciliation errors, wrong codes sent to the bank at the worst moment. This guide maps out every identifier you'll run into, explains who assigns each one, and shows exactly where to find them.

What Is a Merchant Transaction Number?

"Merchant transaction number" is an umbrella phrase, not a standardized term. People searching for it are usually staring at a number on a receipt, a dashboard, or a bank statement with no idea what it refers to or why it matters.

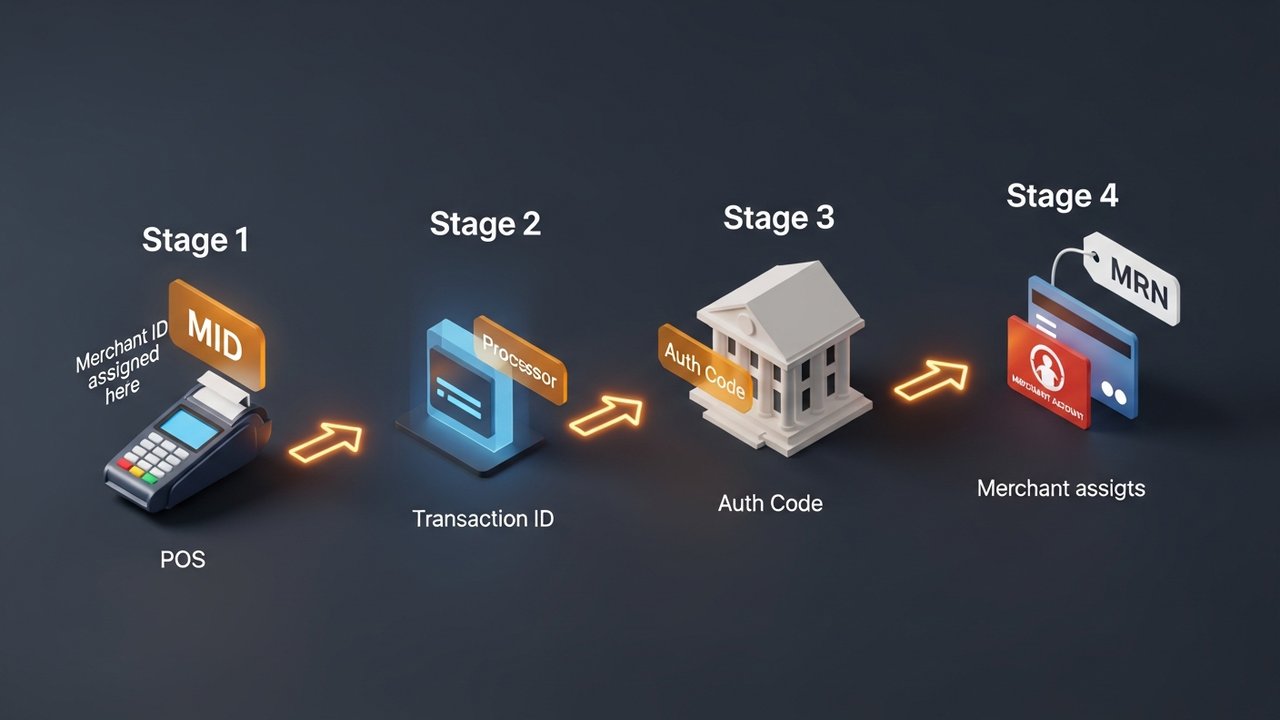

Four distinct identifiers pass through any card transaction:

- Merchant ID (MID) — identifies your business to the payment processor and acquiring bank; permanent, assigned once

- Merchant Reference Number (MRN) — identifies a specific transaction within your own system; you control it

- Transaction ID — identifies a specific transaction within the processor's system; the processor assigns it

- Authorization code — confirms a specific transaction was approved by the card issuer; the issuing bank assigns it

The question each one answers is different. MID identifies the merchant. MRN points to an order in your own records. A Transaction ID pinpoints the payment inside the processor's system. The authorization code is the card issuer's confirmation that the charge was approved.

Merchant ID Number: What It Is and How It Works

A merchant ID number is a unique identifier your business receives when you open a merchant account with an acquiring bank or payment processor. It's typically a 15-digit alphanumeric code, though the exact format varies by processor. The number is permanent — it doesn't change transaction to transaction and stays with your account until it's closed.

The MID routes funds in payment processing. The acquiring bank uses it to identify exactly where settlement money should land. Without a valid merchant id, nothing in the payment processing system can connect an incoming transaction to your merchant account.

The sequence from card swipe to settlement:

- Customer pays — card details hit your payment gateway or point-of-sale terminal

- Processor sends the request — your payment processor packages the transaction data, including your MID, and forwards it to the card network

- Card network routes it — Visa or Mastercard routes the authorization request to the cardholder's issuing bank, with your MID tagging the merchant side

- Issuer approves or declines — the issuing bank sends back an authorization code; the decision travels back through the network to your terminal

- Clearing and settlement — at end of day, transactions batch up; the network uses your merchant id to direct settlement funds from the acquiring bank into your merchant account

One business can hold multiple merchant IDs. A retailer running separate online and in-store operations often needs two MIDs. High-risk product lines like supplements, digital goods, or travel may require their own because the acquiring bank treats different business types as different risk profiles.

Merchant Reference Number: Per-Transaction Tracking

A Merchant Reference Number (MRN) is an alphanumeric identifier that your own payment system assigns to each individual transaction. The bank doesn't generate it — you do, or your payment gateway does on your behalf. That's what makes it the most flexible of the four identifiers.

MRNs show up in different formats depending on which system generates them:

| Format type | Example | Structure |

|---|---|---|

| Numeric | 98532147 | Sequential or random digits |

| Alphanumeric | MRN-45TY78-29Z | Prefix + random characters |

| Combined | XYZ001-78945612 | Business code + order number |

| Date-prefixed | 20260514-00447 | Date + sequence |

Different payment gateways use different names for this concept. Stripe calls it the "Idempotency Key." Razorpay includes it automatically in every transaction response. PayPal surfaces it inside the merchant's transaction detail view. The label changes; the function doesn't — it links a payment to a specific order in your records.

Reconciliation runs on MRNs. When your accounting system needs to match a bank deposit against an order, the MRN is the bridge. Without them, matching high transaction volumes means manually comparing amounts and timestamps, a process that scales badly.

Transaction ID vs Merchant ID: Key Differences

Both a Transaction ID and a merchant id show up on receipts and relate to the same payment. That's where the similarity ends — they come from different systems, get assigned by different parties, and answer different questions.

| Identifier | Assigned by | When assigned | Permanent? | Typical length | Primary purpose |

|---|---|---|---|---|---|

| Merchant ID (MID) | Acquiring bank / processor | When account opens | Yes | 15 digits | Identify the merchant to the network |

| Transaction ID | Payment processor | Each transaction | No | 12–18 alphanumeric | Trace a specific payment in processor records |

| Merchant Reference Number | Merchant's own system | Each transaction | No | Varies | Link payment to merchant's order records |

| Authorization code | Issuing bank | Each approval | No | 6 alphanumeric | Confirm card issuer approved the transaction |

The payment processor assigns and randomizes Transaction IDs. PayPal always generates 17-character IDs, and it deliberately creates separate ones for the buyer and the seller on the same payment. If a buyer's transaction record gets exposed, the seller's transaction data stays hidden — the different IDs are a security feature, not a quirk.

The authorization code stands apart from both. It comes directly from the cardholder's bank, not the processor, and its only job is confirming that a specific charge was approved at a specific moment. When a chargeback hits, the authorization code is your proof that the issuer cleared the transaction.

How to Find Your Merchant Transaction Number

Your MID won't turn up on any public database. Check your monthly merchant statement first, then your processor's online dashboard — usually under Account Settings or Business Information. Some terminal setup paperwork includes it too. Guard it like a bank account number; it's private.

Transaction IDs are easier to track down. Every processor dashboard lists them on individual transaction pages. Customers see them in order confirmation emails. Printed receipts carry them. Your payment gateway API returns one in every response. Search directly by Transaction ID in your processor's dashboard to pull a specific payment.

Merchant Reference Numbers don't come from any external system. They exist in your own records — your payment admin panel, order database, or whatever system your integration uses to log transactions alongside order data.

Finding your merchant id number and Transaction ID by platform:

- Stripe — MID is in Dashboard → Settings → Account Details. Transaction IDs appear as "Payment ID" (format: pi_XXXXXXXXXX) in the Payments section, with the full ID on each payment's detail page.

- Square — MID is under Account & Settings → Business Information. Transaction IDs are in the Transactions section of Square Dashboard, visible in the detail view for each sale.

- PayPal — Transaction IDs appear in Activity → All Transactions → select a transaction. PayPal shows a different Transaction ID to the buyer and to the seller on the same payment — check your merchant-side view, not the buyer's confirmation email.

- Bank statement — some processors embed a shortened MID into the merchant descriptor that appears on cardholders' bank statements. This isn't the full MID, but it can help trace which processor handled the charge.

Can't find your MID anywhere? Call your processor's merchant support line. They'll verify your identity and give it to you directly. No legitimate third-party lookup service for MIDs exists — anyone advertising one is either wrong or running a scam.

Why Merchant IDs and Transaction Numbers Matter

These identifiers aren't bureaucratic overhead. Each one does specific operational work:

- Chargeback disputes — Your acquiring bank needs the Transaction ID, the authorization code, and ideally the MRN to pull a transaction record and build a response. Missing any of them extends the dispute timeline and weakens your case.

- Refund processing — The payment processor needs a Transaction ID to locate and reverse a specific payment. Without one, they can't find the original charge. Logging Transaction IDs at checkout isn't optional if you process refunds at volume.

- Reconciliation — MRNs connect payments to orders in your accounting system. For businesses running high-volume payment processing, that link is the difference between a 20-minute close and a four-hour reconciliation problem.

- Fraud detection — Duplicate Transaction IDs from the same card within a short window are a standard fraud flag. Processors also monitor MID activity patterns to catch account takeovers — unusual velocity on a single MID triggers risk reviews.

- Multi-location reporting — Separate merchant IDs for different store locations or product lines let you track revenue by channel without manually sorting every transaction.

Common Merchant ID and Transaction Number Mistakes

Small errors with identifiers tend to accumulate:

- Running different business types under one MID — A company selling software subscriptions alongside physical goods should separate them. Mixing transaction profiles inflates chargeback ratios and invites a risk review from the acquiring bank.

- Generating duplicate MRNs — Every transaction needs a unique MRN. Duplicates create reconciliation mismatches that take hours to untangle. Use a sequence generator or UUID rather than manual entry.

- Sharing MID credentials — Your MID connects directly to your merchant account. Letting it appear in client-facing documents or sharing it with third parties creates fraud exposure you can't easily undo.

- Skipping Transaction ID logging at checkout — If your system doesn't record Transaction IDs when orders complete, every future refund and dispute gets harder. That's a system design choice, not a support problem.

- Ignoring MID termination risk — Processors can close a merchant account and report the MID to the MATCH list (Member Alert to Control High-Risk Merchants) for excessive chargebacks, fraud, or policy violations. Getting onto the MATCH list makes opening any new merchant account significantly harder. Keeping your chargeback ratio below processor thresholds is the only reliable protection.

Crypto Payments and the Blockchain Transaction Hash

Traditional payment processing routes transactions through a chain of intermediaries. The acquiring bank assigns your merchant id. The processor generates a Transaction ID. Each hop adds a party that can delay, block, or reverse a payment. Crypto works differently.

When a customer pays in Bitcoin, Ethereum, or a stablecoin, the network generates a cryptographic hash — a unique 64-character string that permanently records the transaction on the blockchain. No acquiring bank assigns a MID. No processor generates a Transaction ID. The hash is the record, publicly verifiable on any block explorer.

What this means in practice:

- No intermediary can revoke a blockchain address the way a bank can terminate a MID

- Transaction hashes are permanent and tamper-proof — no dispute about whether a payment occurred

- No chargeback mechanism exists on-chain; a confirmed transaction is settled

- Settlement happens in minutes, not the T+1/T+2 cycle of card processors

For merchants dealing with chargeback exposure — digital goods, subscriptions, international sales — crypto removes the identifier infrastructure that makes disputes possible in the first place. Plisio lets merchants accept Bitcoin, Ethereum, USDT, USDC, and 20+ other cryptocurrencies through a single payment gateway, with each transaction settled and recorded on-chain.

Conclusion

The merchant transaction number isn't one thing — it's four, each assigned by a different party and each used for different purposes.

The Merchant ID number permanently identifies your business to the acquiring bank. The Merchant Reference Number tracks each transaction in your own records. The Transaction ID traces each payment in the processor's system. The authorization code confirms the card issuer said yes.

In practice: Transaction IDs handle refunds and chargebacks, MRNs power reconciliation, and your merchant id number routes settlement funds to the right account. Knowing which one to hand over in which situation cuts dispute resolution time and prevents the accounting errors that build up when records aren't kept properly.

For merchants who want out of the bank-assigned identifier system entirely, crypto payment networks offer a different architecture — no MID, no processor Transaction ID, just a blockchain hash no bank or processor controls.