Digital Asset Market CLARITY Act of 2025: What Changes

The week of July 14 to 18, 2025 will end up in every crypto law textbook ever written. Five working days. Three separate crypto bills the industry had been pushing for since at least 2021. The House of Representatives passed all three. The President signed one. And the regulatory scaffolding that had governed digital assets since 2017 effectively died. CLARITY went through the House 294-134 on July 17 (Roll Call 199). GENIUS got signed the next morning. The Anti-CBDC Surveillance State Act squeaked through by a single vote in the same window.

Taken individually, the three bills look technical. Taken together, they form one regulatory framework for digital assets: stablecoins federalised, the crypto market structure pulled from SEC to CFTC, a federal central bank digital currency blocked. It is more comprehensive than anything Congress had tried before. The rest of this piece works through the CLARITY Act in detail. Then I trace how it locks into the GENIUS Act and the Anti-CBDC bill, where the legislation actually stands in mid-2026, and which corners of the crypto industry win or lose.

What the CLARITY Act actually does

Rep. French Hill, who chairs the House Financial Services Committee, dropped H.R. 3633 on May 29, 2025 with Rep. Glenn Thompson co-leading. The first vote came from House Agriculture: 47-6 in June 2025 after its markup session. Financial Services followed 32-19. Then the floor vote: 294-134 on July 17, 2025. The bill passed the House with broader margins than any prior crypto bill. The regulatory authority it shifts from SEC to CFTC is the largest such move in two decades.

The CLARITY Act would grant the CFTC authority over a new category and divide all digital assets into three categories:

| Category | Regulator | Description |

|---|---|---|

| Digital commodities | CFTC | Assets including a digital commodity intrinsically linked to a blockchain system; the definition of digital commodity covers BTC, ETH, and similar |

| Investment contract assets | SEC | Tokens sold during fundraising; status expires once a non-issuer resells in the secondary market |

| Permitted payment stablecoins | Under GENIUS Act | Currency-pegged, redeemable; the permitted payment stablecoin issuer must hold 1:1 reserves |

The bill does several things. It registers digital commodity exchanges, brokers, and dealers with the CFTC and the National Futures Association. It requires Qualified Digital Asset Custodians to hold customer assets ring-fenced from the custodian's own liabilities. And it creates a $75 million small-offering exemption with tailored disclosures.

Section 604 carves out network validators, node operators, and protocol developers from intermediary registration. Section 605 codifies a right to self-custody. The Bank Secrecy Act and the Commodity Exchange Act both still apply to qualifying intermediaries.

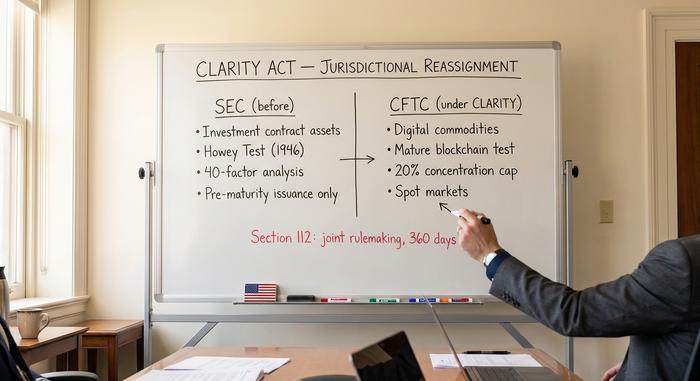

SEC vs CFTC: the jurisdictional rewrite

Everything else in the bill is downstream of one decision. CLARITY moves spot markets for digital commodities to the Commodity Futures Trading Commission, leaving the Securities and Exchange Commission with primary issuance (until a token "matures") and anti-fraud enforcement on SEC-regulated venues.

Background matters here. The SEC under Gary Gensler treated most crypto tokens as unregistered securities. The agency built enforcement actions on the Howey Test from 1946 and a 40-factor analysis. Coinbase, Kraken, Ripple — all sued. Paul Atkins took over as SEC chair on April 21, 2025 after a 52-44 Senate confirmation. The agency then dropped or paused most of those cases inside a quarter. CLARITY writes the new posture into statute so a future SEC cannot simply reverse the policy by enforcement memo.

The replacement for the 40-factor framework is a "mature blockchain system" test with objective criteria. A blockchain counts as mature when four conditions hold. The network is functional (transactions and governance work). The code is open-source. Operating rules are transparent and pre-established. And no single entity controls more than 20 percent of tokens or voting power. Once a blockchain certifies as mature, insider resale restrictions ease and the token sits entirely under CFTC oversight. Investment contract asset status expires the moment a non-issuer party resells in secondary markets. That is the structural answer to the "is Bitcoin still a security if a VC sold it?" problem the SEC litigation never resolved.

Section 112 of the bill sets a 360-day deadline for the SEC and CFTC to issue joint rulemaking. Section 113 establishes a 180-day provisional registration window that sunsets after four years, letting exchanges operate while the formal rules are finalised.

The 20 percent control threshold is the part that worried me when I first read the draft. The number is concrete enough to litigate against, which is the entire point. It is also a number every project will now optimise for, not necessarily in directions that serve users. Distribute the float wider, retain economic control via a foundation that does not vote tokens, and the test passes without the substance.

The Senate has a competing approach. The Senate Committee on Banking dropped a 309-page draft on May 12, 2026. It is called the Responsible Financial Innovation Act of 2025. It preserves more SEC authority over what it calls "ancillary assets." Two days later, on May 14, the committee on banking voted 15-9 to advance a revised CLARITY companion. Senators Gallego and Alsobrooks crossed party lines. The Senate Agriculture Committee's Digital Commodity Intermediaries Act passed out of committee on January 29, 2026. The two Senate versions still need to merge before they reach the Senate floor.

How CLARITY fits with the GENIUS Act and the Anti-CBDC bill

CLARITY is one third of a package. The other two pieces shipped in the same House week. The trio is what actually matters.

Start with GENIUS. The Senate cleared it 68-30 on June 17, 2025. The House moved it 308-122 on July 17. Trump signed it the next morning, July 18. Five weeks. From nothing to a full federal framework on stablecoins. The law requires 100 percent reserve backing in cash or short Treasuries, monthly attestations, and a flat ban on paying yield to holders (Section 4(a)(11)). Three charter paths exist for issuers, and they matter: an OCC-supervised national trust bank, a state-licensed money transmitter, or a new federal qualified payment stablecoin issuer category that did not exist before. Full effective date by January 18, 2027 at the latest.

Now Anti-CBDC. Rep. Tom Emmer's H.R. 1919 squeaked through the House 219-210 on July 17, 2025. Read that vote count again. It is the closest of the three. The bill prohibits the Federal Reserve from issuing a central bank digital currency directly to individuals, or indirectly through intermediaries without explicit congressional authorization, and blocks CBDC use as a monetary-policy tool. Trump had already issued executive order 14178 on January 23, 2025 directing the Working Group on Digital Asset Markets to oppose a CBDC, but an EO can be reversed on day one of the next administration. The bill writes the ban into statute. The Senate version is still pending, folded into a broader package called the Financial Innovation and Authorization Act.

| Bill | House vote | Senate vote | Status |

|---|---|---|---|

| GENIUS Act (S. 1582) | 308-122 (Jul 17, 2025) | 68-30 (Jun 17, 2025) | Signed into law Jul 18, 2025 |

| CLARITY Act (H.R. 3633) | 294-134 (Jul 17, 2025) | Banking Committee 15-9 (May 14, 2026) | Awaiting Senate floor vote |

| Anti-CBDC (H.R. 1919) | 219-210 (Jul 17, 2025) | Bundled into FIAA | Senate pending |

How do they interlock? GENIUS defines the federal stablecoin lane. CLARITY then pulls stablecoins out of the SEC/CFTC tug-of-war by treating them as their own asset class, governed under GENIUS rather than fought over by the two main regulators. Anti-CBDC slams the door on the only competitor a private stablecoin would have actually feared, a Fed-issued retail dollar. Stand back and the policy is coherent. Private stablecoins, regulated and protected. Market structure, clarified. Fed-issued retail dollar, off the table.

Critics like Senator Elizabeth Warren and Better Markets are not buying it. Their argument: the package shifts authority from a more aggressive consumer cop (the SEC) to a leaner one (the CFTC), and the CBDC ban forecloses options central banks elsewhere are actively using. Both points have force. Both also miss that the politics of 2025 made any path forward impossible without trades like this one.

Where the CLARITY Act actually stands in 2026

Procedurally, this is messier than the bill summary suggests. The House moved the bill on July 17, 2025. Then it sat there. Months passed. The Senate Banking Committee postponed its initial markup on January 14, 2026 — the stablecoin yield fight had blown up — and spent four months in negotiation. A revised 309-page draft finally arrived on May 12, 2026. Two days later, the committee voted 15-9 to advance it. Senators Gallego and Alsobrooks crossed over. Senate Agriculture's parallel Digital Commodity Intermediaries Act had cleared its committee back on January 29, 2026. Both chambers still need to reconcile, the Senate has yet to take a floor vote, and the rules for digital commodity intermediaries that the act would create cannot take effect until both chambers agree.

Two fights drove the delay. The first is stablecoin yield. Banks fight every form of it because they fear deposit flight. Crypto firms want activity-linked rewards — money paid for actually doing something on-chain, not just for holding the coin. GENIUS banned yield on simple holdings outright. The Senate Banking draft tried to push the ban further, and that is where the negotiations stalled. The second fight is the DeFi carve-out. How wide should it be? Wide enough to cover real decentralised protocols. Not so wide that bad actors can slip through claiming to be one.

There was a White House deadline too. March 1, 2026 for a stablecoin-yield compromise. It expired. A Truth Social post from President Trump on March 8 was read across the industry as a quiet deprioritisation of crypto legislation. Prediction markets nevertheless price 2026 enactment near 72 percent. The realistic path forward: a Senate floor vote, a conference committee with the House version, sixty votes to break a Senate filibuster, and another House vote if anything got amended along the way.

Industry winners and losers under CLARITY

The package favours US-domiciled crypto exchanges with public compliance budgets. Coinbase reported $1.0 billion in transaction revenue on $295 billion of trading volume in Q3 2025, plus $355 million in stablecoin revenue, and explicitly cited regulatory clarity as the operating environment it was investing into. Kraken posted $648 million in revenue in the same quarter. Robinhood Crypto sits in the same favoured tier among US crypto exchanges. Credit unions and community banks gain a clearer path under the act's joint federal framework, similar to how the Federal Credit Union Act treats other financial products.

Stablecoin issuers that already match GENIUS standards win. Circle's USDC, with reserves in cash and short Treasuries (around $78 billion as of mid-2026), maps cleanly to the new rules. Tether's USDT, at roughly $190 billion of a total stablecoin market near $323 billion per DeFiLlama, has historically held less transparent reserves and faces a more uncertain compliance path. Established protocols whose tokens can credibly claim mature blockchain status keep secondary-market liquidity. The losers are token issuers that cannot pass the 20 percent concentration test, offshore exchanges without US-compliant arms, and DeFi protocols with discretionary admin keys.

Critics and unresolved problems

Senator Elizabeth Warren has been the loudest opponent. Her argument: the package shifts consumer-protection authority from a stronger cop (the SEC) to a weaker one (the CFTC). And she has a point. Historically, the CFTC was built for institutional derivatives oversight, not for retail spot markets, and its enforcement budget for risks associated with digital trading runs a fraction of the SEC's. Better Markets has hit the same note in formal comments on GENIUS Act rulemakings, warning that stablecoin risk can leak into the broader economy if reserves are not strictly limited under existing Consumer Protection Act and Federal Deposit Insurance Act frameworks.

The decentralisation test is the technical loophole that worries practitioners. Twenty percent control is a bright line. But token distributions can be engineered to clear it without producing real decentralisation. Place tokens with a foundation that does not vote them, and an issuer can technically pass the test. The criteria are easier to game than to enforce. The DeFi carve-out faces a similar problem. The line between intermediary and protocol is contested. The language will generate enforcement disputes for years.

Payment stablecoins are not covered by Regulation E. That means a fraudulent transfer of stablecoins through a hacked wallet may not be reimbursed the way an unauthorised ACH transfer would be. The joint SEC/CFTC rulemaking mandate in Section 112 was designed to force coordination on laws and regulations governing digital assets. In practice, it may slow rule issuance to the pace of the slower agency. The Securities Act references underlying CLARITY rely on existing federal statutes. Six months for joint rules sounds tight on paper. Historically, it takes two to three years.

The honest read on the CLARITY Act's path forward

The CLARITY Act is the centerpiece of a three-bill framework that, if it clears the Senate, will be the largest restructuring of US digital-asset law since the 1934 statutes set the SEC/CFTC architecture in the first place. Two of the three bills are already law. The third has been one Senate vote short for almost a year. The two likeliest 2026 outcomes are Senate passage with a stablecoin-yield compromise that splits banks and crypto firms, or a stall through the midterms with CLARITY rolling into 2027.

Read the CLARITY Act once before forming an opinion. Watch the Senate Banking markup language carefully. Track the stablecoin-yield fight, because that is where the real policy gets decided.