Aerodrome Finance: AERO, Swaps, Price, and Risk

Aerodrome is the engine room of Base. Most of the trading on Coinbase's layer-2 network runs through it, which makes it one of the most important pieces of crypto infrastructure most people have never heard of. It is also a puzzle. The protocol pays out more in token rewards than it earns in fees, its total value locked is down more than 80% from its peak, and in late 2025 it managed to get hacked and announce a merger in the same month. That gap between how dominant Aerodrome is and how its economics actually work is the real story behind the AERO price, and it is the part the price-tracker pages skip. Here is what Aerodrome is, how the AERO token works, and what the numbers are really saying.

What Aerodrome Finance Is on Base

Aerodrome Finance is the main decentralized exchange on Base, and if you trade anything on that chain you have probably touched it without noticing. It launched in August 2023 and quickly became the place where Base liquidity lives.

A DEX and liquidity hub on Base

A decentralized exchange, or DEX, lets people swap one token for another without a company sitting in the middle holding the order book. It is one of the basic building blocks of decentralized finance, the on-chain version of the services a bank or brokerage would normally run. Instead of matching buyers and sellers, an automated market maker (AMM) holds pools of two tokens and prices trades against the ratio between them. Anyone can deposit into those pools as a liquidity provider and collect a share of the trading fees. Aerodrome is that kind of AMM, built to be the central liquidity hub for Base and the place most of its token swaps route through. It runs several pool types under one roof: simple volatile pairs, stable pairs tuned for assets that should trade close to one another like two dollar stablecoins, and concentrated-liquidity pools for fine-tuned market making. The scale is real: Aerodrome routinely handles somewhere between 57% and 63% of all DEX volume on Base, and its 30-day trading volume has run around $18 billion. Cumulative fees since launch have passed $349 million. Whatever you think of the token, the exchange itself is genuinely used.

Built by the Velodrome team

Aerodrome did not appear from nowhere. It was built by the team behind Velodrome Finance, the dominant DEX on Optimism, as a deliberate copy of that model aimed at Base. The two are siblings: same vote-escrow design, different chains. Because the Base network is Coinbase's layer-2, Aerodrome ended up as the default liquidity layer for a chain with one of the largest companies in crypto standing behind it. That pedigree is a big reason it grew so fast, and a big reason its fortunes are tied to Base's.

The AERO Token and the ve(3,3) Flywheel

AERO is easy to misread as just another cryptocurrency price ticker. It is really the steering wheel of the whole system. Holding it, and more importantly locking it, is how you decide where the protocol's rewards flow and how you collect the fees they generate.

AERO, veAERO, and voting

The model is called ve(3,3), shorthand for vote-escrow combined with a game-theory reward loop. You lock your AERO tokens for up to four years and receive veAERO, held as an NFT. That veAERO is your voting power: once a week, you vote on which liquidity pools should receive the next batch of AERO emissions. In return, you earn 100% of the trading fees from the pools you vote for, plus any incentives that outside projects pay to attract votes to their pool. That second part is the clever bit: a new token that wants deep liquidity on Base does not have to run its own rewards program, it simply pays veAERO holders a weekly bribe to vote emissions toward its pool. Aerodrome turned liquidity into something projects bid for. The design launched with 500 million AERO, and about 90% of it was locked as veAERO on day one, which tells you the system was built to reward commitment over quick flipping.

The flywheel and its catch

The loop is meant to spin like this. Emissions attract liquidity providers, deeper liquidity attracts traders, trading produces fees, and fees plus incentives make locking AERO worthwhile, which supports the token and funds more emissions. When it works, it is a genuine flywheel, and on Base it clearly spun. The catch sits in plain sight — the fuel is emissions, and emissions are new tokens. Supply has grown from that initial 500 million toward roughly 1.9 billion, with about 953 million circulating and no hard cap. As long as the value those emissions create is greater than the dilution they cause, holders come out ahead. When it flips, they are being paid in a coin that is busy printing more of itself.

AERO Price, Market Cap, and Supply Today

The Aerodrome Finance price tells the unwinding story more bluntly than any chart caption. After a 2024 run, AERO has spent the time since giving most of it back.

| AERO snapshot (as of June 2026) | Figure |

|---|---|

| Price | about $0.35 |

| Market cap | about $332 million |

| Fully diluted valuation | about $669 million |

| All-time high | $2.32 (December 2024) |

| Down from ATH | about 85% |

| Circulating / total supply | ~953M / ~1.92B (no hard cap) |

A market cap near $332 million on a fully diluted valuation near $669 million is the market saying it expects more supply to arrive. That is the honest read of the price today: Aerodrome is a dominant exchange whose token has not yet shown it can hold value through its own emissions.

Is the Aerodrome Flywheel Sustainable?

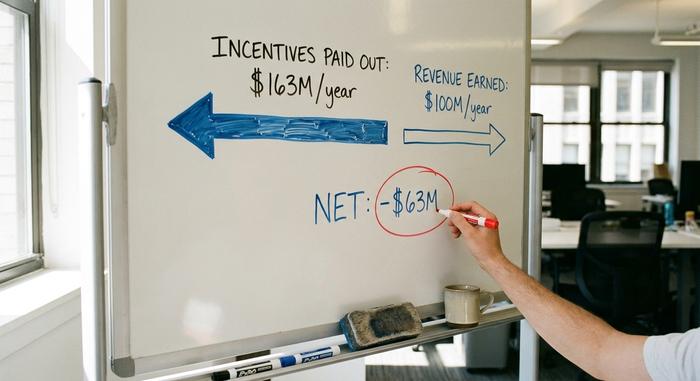

This is the question the price pages do not touch, and it has a number attached. Aerodrome currently pays out more than it brings in.

When incentives exceed revenue

According to DeFiLlama, Aerodrome distributes roughly $163 million a year in incentives while taking in around $100 million in revenue, which leaves it net negative by about $63 million annualized. In plain terms, the protocol is subsidizing its own activity with token emissions. You can see the effect in the deposits. Total value locked peaked near $1.62 billion in December 2024 and had fallen to around $291 million by June 2026, a drop of more than 80%. The trading volume held up far better than the deposits did, which is the interesting part: people kept using Aerodrome to swap even as they pulled their parked capital out. The exchange stayed useful; the yield stopped being worth the dilution.

| Aerodrome economics | Figure |

|---|---|

| Annualized incentives paid | about $163 million |

| Annualized revenue | about $100 million |

| Net | about −$63 million |

| TVL, December 2024 | about $1.62 billion |

| TVL, June 2026 | about $291 million |

Mercenary liquidity and the AERO price

The polite name for capital that chases whichever pool emits the most rewards is mercenary liquidity, and ve(3,3) runs on it. That is fine while emissions are worth more than the dilution they cause. When fees cannot keep up, lockers are effectively being paid in a token that is diluting them, and the rational move is to leave, which is roughly what the TVL chart shows. Aerodrome's answer is an emissions-control mechanism its community calls the "Aero Fed," meant to dial issuance up or down based on conditions rather than running a fixed schedule. It is a sensible idea. It has not yet been stress-tested through a full cycle, so the jury is out.

Slipstream, Coinbase, and the Base Bet

Aerodrome's greatest strength and its single biggest risk are the same thing: Base. In April 2024 it shipped Slipstream, a concentrated-liquidity feature in the style of Uniswap v3 that lets liquidity providers focus their capital in a tighter price range for better efficiency. That kept it competitive on the actual trading experience, not just the rewards. Concentrated liquidity matters because it lets a provider put their capital exactly where trading actually happens instead of spreading it thinly across every price, which means tighter spreads for traders and better returns for the people supplying the pool. The Coinbase connection runs deeper than branding, too. Coinbase Ventures put more than $20 million into veAERO and actively votes its locked position on gauges, including pools for Coinbase's own cbBTC, its wrapped Bitcoin on Base. The upside is obvious: a deep-pocketed backer with every reason to keep Base liquid. The downside is concentration. Aerodrome draws almost all of its volume from a single chain, so if Base stumbles or Coinbase shifts focus, there is no second market to fall back on. A protocol this dominant on one network is only as safe as that network's relevance.

The Aero Merger and the 2025 Hack

Two events in late 2025 reset the story, one structural and one a warning. In November 2025, Dromos Labs announced that Aerodrome and Velodrome would merge into a single protocol called Aero, with AERO holders receiving about 94.5% of the unified protocol's revenue, Base serving as the hub, and an expansion to Ethereum mainnet planned for 2026. The merger consolidates the two sibling exchanges into one token and one story, which simplifies a structure that had always been a little awkward. For holders, the pitch is concentration of value: instead of two competing tokens splitting the liquidity and the fees of essentially the same product on two chains, AERO becomes the single claim on a multi-chain DEX. Whether that fixes the underlying revenue gap or just repackages it is the open question.

The warning came the same month. Aerodrome's website was hijacked through a DNS attack, traced to an insider at the domain registrar NameSilo, and more than $1 million was drained from users who connected to the poisoned front-end. The smart contracts themselves were never breached. That distinction matters: the protocol's code held, but the website pointing at it did not. It is a reminder that in DeFi the dangerous part is often the part that looks most ordinary, like a domain name.

Is AERO Crypto a Good Investment?

Here is the honest version. Aerodrome is the clear leader on Base and a genuinely heavy-used exchange, but AERO the token has not proven it can hold value through its own emissions, and it sits about 85% below its peak. The bull case is real: the Aero merger, continued Base growth, and emissions control actually working would let fees catch up to incentives. The bear case is just as real, because none of that has happened yet. My take is to separate the two questions. Aerodrome the protocol is strong. AERO the investment is a bet that the flywheel turns a profit before the dilution catches up — and that is a bet, not a savings plan. Do not confuse volume dominance with value accrual.

What Aerodrome Finance's Numbers Say

Aerodrome proved something useful: the ve(3,3) model can win a whole chain's liquidity and keep it active through a brutal drawdown. What it has not proved is that the model pays for itself once you net the emissions against the fees. That is the number worth watching, more than any TVL headline or price-prediction thread. The merger and the Aero Fed are the protocol's attempt to close that gap, and the next year should show whether they work. So before you treat AERO as anything more than a high-risk bet, ask the question the price pages never print: can you actually see this flywheel turning a profit?