P2P Crypto Trading: How Direct Bitcoin Trades Work

In much of the world, the hard part of buying crypto is not the crypto. It is the bank account. Where local banks refuse cards, freeze crypto-linked transfers, or simply do not exist for most people, P2P crypto trading is how coins actually change hands. It lets two people swap cash for crypto directly, with a platform standing in the middle only to hold the funds in escrow until both sides deliver. This guide covers how that works, how to make your first trade without getting burned, and the scams that target newcomers most.

What P2P crypto trading actually is

P2P, short for peer-to-peer, means you trade with another person instead of buying from the exchange itself. It is direct trading: on a centralized cryptocurrency exchange you buy from a giant pooled order book, but on a P2P marketplace you scroll a list of ads posted by individual buyers and sellers, each setting their own price and accepting their own payment methods.

The platform is not your counterparty. It is the referee. When you accept an ad, the seller's crypto gets locked in escrow, you send fiat through the agreed method, and only then does the platform release the crypto to you. That escrow step is the difference between a trusted trade and handing cash to a stranger and hoping. Peer-to-peer crypto trading lives or dies on it. In short, peer-to-peer trades let you buy and sell bitcoin or stablecoins directly with another person, with the platform acting only as escrow.

How P2P exchanges work: escrow at the core

Understand escrow and you understand the whole model. Everything else is detail. Escrow is the mechanism that lets two people who will never meet — often in different countries, in different time zones — trade thousands of dollars without trusting each other at all.

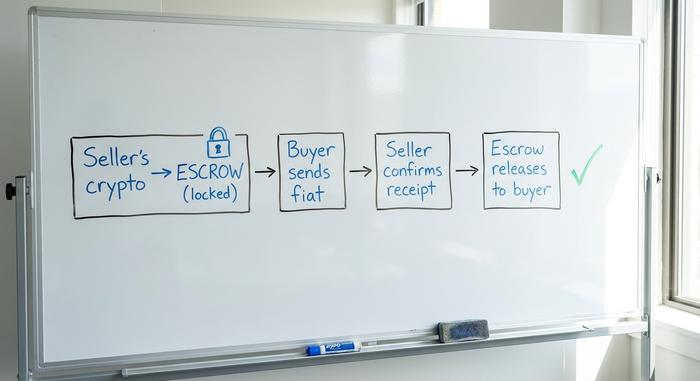

The trade lifecycle, step by step

Every P2P transaction runs in a fixed order. A seller posts an ad, or a buyer does. The other party accepts it for a chosen amount. At that instant the seller's crypto is moved into escrow, held by the platform so it cannot be spent or withdrawn. The buyer then sends fiat through the agreed channel, marks the payment as sent, and waits. The seller checks their own bank or wallet, confirms the money truly arrived, and clicks release. Escrow opens and the crypto lands in the buyer's account. Skip or reorder any of those steps and you have created the exact gap a scammer needs.

Custodial vs non-custodial escrow

Not all escrow is the same. On custodial platforms like Binance P2P, the exchange holds the keys and acts as both vault and judge. On non-custodial platforms like Bisq and Hodl Hodl, the crypto sits in a 2-of-3 multisig wallet, and the platform holds only one key as a tiebreaker. Neither side, nor the platform alone, can move the funds. That removes the "what if the platform itself fails or freezes me" risk, at the cost of a steeper learning curve.

What happens in a dispute

If the buyer claims they paid and the seller disagrees, the trade goes to arbitration. A moderator reads the in-platform chat and the evidence. This is why every serious trader keeps all communication inside the platform and never accepts a screenshot as proof of payment. A real bank confirmation in your own account is proof. A picture is not.

Timing matters too. Most platforms attach a payment window to each trade, often 15 to 30 minutes, with a countdown the buyer must beat. If the buyer does not mark payment in time, the trade auto-cancels and the escrowed crypto returns to the seller untouched. That clock is a feature: it stops a buyer from locking a seller's coins for hours while the price moves. As a seller, let a stalled trade expire rather than releasing early to "be nice."

P2P vs a centralized exchange: tradeoffs

Choosing between P2P and a regular exchange comes down to what you are short on. A centralized exchange gives you instant fills, deep liquidity, and a company to complain to. P2P gives you privacy, hundreds of payment options, and access in places where exchanges cannot legally operate. What you give up is speed and a safety net.

Liquidity is the quiet tradeoff people underestimate. On a deep exchange order book, a large buy barely moves the price. On a P2P marketplace, you are limited to whatever individual sellers have posted, so a big order may mean splitting it across several counterparties or paying a premium of a few percent over the spot rate. For small, occasional trades that gap is minor. For size, it adds up fast.

| Model | Best for | Strength | Weakness |

|---|---|---|---|

| P2P marketplace | Privacy, local payments, no-bank access | Flexible fiat rails, hard to block | Slower, scam risk, thinner liquidity |

| Centralized exchange | Speed and volume | Instant fills, deep liquidity, support | KYC, custody risk, can be geo-blocked |

| Decentralized exchange | On-chain swaps | Non-custodial, no signup | Crypto-to-crypto only, no fiat, gas fees |

Your first P2P trade, step by step

Start your first P2P crypto trade as a buyer, and start small. Pick a counterparty with a high completion rate and hundreds of past trades, not the cheapest price from an account opened yesterday. Read the ad's terms before you accept; some sellers demand a specific payment reference or a video selfie.

Once you accept, the crypto is in escrow, so you are safe to pay. Send the fiat only through the method you both agreed, from your own account, and mark it paid. Then wait for release. As a seller, the rule flips and gets stricter: never click release until you have personally seen the money settle in your account. Keep every message in the platform chat. The moment someone asks to move the conversation to WhatsApp, something is wrong.

Payment methods and the chargeback trap

In P2P crypto trading, the payment rail you accept quietly decides how much risk you carry. P2P platforms support everything from bank transfers to gift cards, and that flexibility is the whole appeal. It is also the danger.

Reversible rails are the problem. If you sell crypto and accept PayPal, a card payment, or some instant-payment apps, the buyer can later file a chargeback or reversal, claw the money back from your account, and keep the crypto you already released. The platform's escrow cannot protect against a payment that gets undone after the fact. Sellers who survive long-term lean toward harder-to-reverse rails like bank wires or cash deposits, stick to their preferred payment options, and treat any buyer pushing a reversible method with suspicion.

Security and the risks of P2P scams

Here is the thing worth memorizing. Almost every P2P scam, no matter how elaborate it looks, is a single trick wearing different costumes — convince you to release escrow before an irreversible payment has actually cleared. Once you see that pattern, the specific cons get easy to spot.

Fake receipts and reversed payments

The most common scam is a doctored payment proof. The buyer sends a convincing screenshot of a "completed" transfer, or makes a real payment that is silently pending or scheduled to cancel. Pressured to release, an inexperienced seller does. The fix is absolute: never trust their proof, only confirm money landed in your own account.

Off-platform and triangulation scams

Two patterns dominate. The first is the off-platform move, where a trader insists on finishing the deal over Telegram or by direct transfer, abandoning escrow entirely. The second is triangulation, where the payment you receive comes from a stolen third-party account; weeks later the real owner reverses it and you are liable.

A third variation targets buyers: the overpayment refund. A "seller" claims you accidentally sent too much fiat and asks you to refund the difference to a new account, before any crypto is released. There is no overpayment and no crypto coming. And watch for impostors posing as platform support in your inbox, asking you to verify a wallet seed phrase or move funds to a "safe" address. Real support never asks for either.

Rules that keep you safe

Stay inside escrow always. Confirm funds yourself before releasing. Reject any payment from a name that does not match your counterparty. Check the trader's reputation and account age. Start with small amounts until you trust the flow. None of this is complicated, but skipping one step is usually how people lose money. Follow these rules and P2P stays a reasonably secure trading method even as crypto scams grow more sophisticated. For scale, the FTC reported $12.5 billion in fraud losses in 2024, and Chainalysis traced about $14 billion in crypto scam revenue in 2025.

| Scam type | Red flag | Your defense |

|---|---|---|

| Fake receipt | A screenshot instead of settled funds | Confirm in your own account only |

| Reversed payment | PayPal, card, or instant-app offer | Prefer irreversible rails |

| Off-platform deal | "Let's finish on Telegram" | Never leave platform escrow |

| Triangulation | Payer's name differs from trader's | Reject third-party payments |

Best P2P crypto platforms in 2026

The field has thinned out. LocalBitcoins, the pioneer that launched the whole model, halted trading in February 2023. Paxful, once 14 million users strong, shut down for good in November 2025. What remains splits into two camps. Custodial giants, led by Binance P2P with its roughly 100-plus fiat currencies and 800-plus payment methods, dominate on liquidity and ease, and it remains the default P2P trading platform for most beginners. Bybit P2P and OKX P2P mirror the same model for people already on those exchanges. Non-custodial platforms like Bisq, Hodl Hodl, and NoOnes serve crypto traders who want minimal or no KYC and full control of their keys.

Fees are low across the board. Binance P2P advertises zero trading fees on many markets, taking its cut on the spread instead, while non-custodial platforms charge a small trade fee. When you compare P2P options, weigh fees against escrow type and reputation, not price alone.

How do you pick between them? Start with your country and your payment method, since an ad means nothing if no one near you accepts it. Then weigh the reputation system: a good platform shows each trader's completion rate, total trades, and account age, and those numbers protect you more than any logo. Beginners are usually best served by a high-liquidity custodial venue first, graduating to non-custodial tools once the escrow flow feels routine.

| Platform | Escrow type | KYC | Fees | Best for |

|---|---|---|---|---|

| Binance P2P | Custodial | Required | 0% maker | Liquidity, beginners |

| Bybit / OKX P2P | Custodial | Required | Low/0% | Existing exchange users |

| Bisq | Non-custodial multisig | None | ~Low trade fee | Privacy maximalists |

| Hodl Hodl | Non-custodial multisig | None | ~0.5% | No-KYC Bitcoin |

| NoOnes | Custodial | Tiered | Varies | Emerging-market payments |

Why P2P trading thrives in emerging markets

Where banking works smoothly, P2P crypto trading is a niche. Where it does not, it is infrastructure. The pattern is clearest in the global adoption data: India ranked first in Chainalysis's 2025 Global Crypto Adoption Index, with much of the activity flowing through grassroots, P2P-style channels rather than institutional desks.

Sub-Saharan Africa is the sharpest example. The region took in about $205 billion in on-chain value in the year to June 2025, up 52% year over year, and stablecoins made up roughly 43% of that volume as people reached for a dollar substitute their local currency could not provide. Nigeria alone accounted for around $92.1 billion. The pull is not limited to Africa. Asia-Pacific crypto value grew from roughly $1.4 trillion to $2.36 trillion in the year to June 2025, a 69% jump, with a large share moving through retail and peer channels rather than institutions. The common thread across these regions is the stablecoin: people are not chasing speculative gains so much as holding a synthetic dollar their local currency cannot give them. In economies with currency controls and unstable money, buying crypto locally through a peer is often the only door open, which is exactly why governments have started slamming it.

Is P2P crypto trading legal? KYC and rules

In most countries P2P crypto trading is legal, but the gray area it used to enjoy is closing fast. Custodial platforms now run mandatory KYC as standard; the EU's MiCA travel-rule requirements went fully live on December 30, 2024, and FATF travel-rule standards have been adopted across 85-plus jurisdictions. The friction point is currency control. When P2P becomes a way to dodge official exchange rates, states react hard, as Nigeria did in 2024 when it detained Binance executives amid scrutiny of naira P2P markets. Non-custodial, no-KYC platforms still operate, but they sit in a shrinking gray zone, not a safe harbor.

The verdict on P2P crypto trading

P2P crypto trading is the right tool for a specific person — someone who lacks easy banking access or genuinely values privacy, and who is disciplined enough to respect escrow every single time. For that person it is liberating, and often the only option. It is the wrong tool if you want instant fills, deep liquidity, or a company to refund your mistakes. I keep coming back to that asymmetry: P2P hands you real freedom and, in the same motion, the full bill for any slip. The whole system runs on escrow discipline and reputation. The open question is whether that quiet, person-to-person trust can keep scaling as regulators tighten the rules around it.