Uniswap: How the Biggest DEX Works, How to Trade on It, and What the Data Shows in 2026

November 2018. Hayden Adams, a mechanical engineer who'd been laid off from Siemens, deployed a set of smart contracts on Ethereum. No VC money. No marketing budget. Just an idea that Vitalik Buterin had sketched out two years earlier about using a mathematical formula to replace order books. That deployment was Uniswap v1, and it changed how crypto trading works forever.

Seven years later, the protocol has processed over $3.45 trillion in cumulative trading volume. It runs on roughly 40 blockchain networks. Uniswap Labs, the company behind the protocol, raised over $165 million in funding and is valued in the billions. The UNI token airdrop in September 2020 gave 400 tokens to every wallet that had used the protocol, worth about $1,400 at the time and over $12,000 at the peak. People who used a free tool once got paid thousands of dollars for it.

I've been using Uniswap since v2. Probably done a thousand swaps across four chains at this point. The protocol has evolved from a simple swap tool into a full DeFi infrastructure layer with concentrated liquidity, programmable hooks, its own L2 chain, and a fee switch that fundamentally changed its economics. This article walks through all of it: what Uniswap is, how each version works, how to use it in practice, and where the protocol stands by the numbers in 2026.

What Uniswap is: the protocol that killed order books on DEXs

Uniswap is a decentralized exchange protocol that lets you swap tokens directly from your wallet without a centralized intermediary. No account. No KYC. No deposit. Connect wallet, pick tokens, swap. The trade executes against a liquidity pool, which is a smart contract holding paired tokens deposited by other users.

The pricing comes from the constant product formula: x * y = k. If a pool holds 100 ETH and 200,000 USDC, the product is 20,000,000. When you buy 1 ETH, the pool adjusts the ratio to maintain that constant. The price moves automatically based on supply and demand within the pool. No human market maker decides the price. Math does.

Before Uniswap, every DEX tried to replicate Binance's order book on a blockchain. Didn't work. Placing an order cost gas. Canceling cost gas. Moving your price cost gas. The UX was garbage and nobody used it except masochists. Uniswap killed that entire approach by replacing the order book with a math formula and a pool of tokens. One transaction to swap. No orders to manage. The protocol went from zero to handling 35.9% of all DEX volume because that simplicity turned out to be exactly what the market wanted.

The evolution: v1 through v4

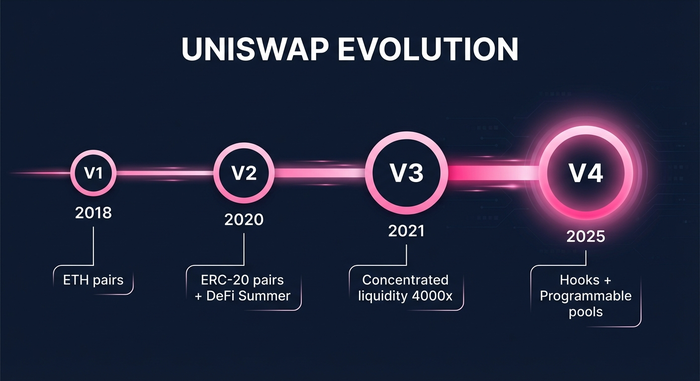

Uniswap has gone through four major versions, each solving problems the previous one exposed.

V1 (November 2018) was the proof of concept. ETH-to-token swaps only. Every pool paired a token with ETH. If you wanted to swap DAI for USDC, your trade went DAI to ETH to USDC, two hops. Simple. Limited. Proved the AMM concept was viable.

V2 (May 2020) added direct ERC-20 to ERC-20 swaps, eliminating the forced ETH hop. It also introduced price oracles (time-weighted average prices) and flash swaps that let developers borrow pool assets within a single transaction. V2 was the version that caught fire during DeFi Summer. TVL went parabolic. Uniswap became the default DEX.

V3 (May 2021) introduced concentrated liquidity, the biggest technical leap in AMM design. Instead of spreading your capital across the entire price curve (zero to infinity), LPs pick a specific price range. If ETH is at $2,000, you can concentrate between $1,800 and $2,200. Within that range, your capital is dramatically more efficient. Uniswap claimed up to 4,000x capital efficiency over v2 for tight ranges. V3 also added multiple fee tiers (0.01%, 0.05%, 0.3%, 1%) so pools could optimize for different volatility levels. It launched on Ethereum, Arbitrum, and Polygon.

V4 (January 2025) is the current version and it introduced "hooks," which are customizable plugins that developers attach to pools. A hook can add dynamic fees that change with volatility. Or on-chain limit orders. Or custom oracle logic. Or automatic LP position management. Each pool can have its own hook, which means v4 isn't one AMM design. It's a framework for building any AMM design. As of early 2026, there are 4,689 tracked v4 pools with an average APY of 56.43%.

| Version | Launch | Key feature | Innovation |

|---|---|---|---|

| V1 | Nov 2018 | ETH-token pairs | Proved AMMs work |

| V2 | May 2020 | ERC-20 pairs, flash swaps | DeFi Summer engine |

| V3 | May 2021 | Concentrated liquidity | 4,000x capital efficiency |

| V4 | Jan 2025 | Hooks (programmable pools) | AMM as a platform |

How to use Uniswap: swapping, LPing, and the wallet app

The basic swap takes thirty seconds if you know what you're doing.

Go to app.uniswap.org. Connect your wallet (MetaMask, Coinbase Wallet, WalletConnect, or the Uniswap Wallet app itself). Select the network: Ethereum, Arbitrum, Polygon, Base, Optimism, BSC, Avalanche, or any of the ~40 supported chains. Pick the token you're selling in the top field, the token you're buying in the bottom field, enter the amount. The interface shows you the exchange rate, price impact, minimum received after slippage, and which Uniswap version is routing your trade. Click swap, confirm in your wallet, done.

Providing liquidity is where it gets interesting and where I've actually made (and lost) money. Pool section, "New Position," pick your pair and fee tier. Then the hard part: choosing your price range. I learned this the expensive way. Set a tight range on an ETH/USDC position once, ETH moved 15% in a week, my position went dormant, and I sat there earning nothing while watching the price walk away from me. Wider ranges are safer. Tighter ranges earn more when they work. Neither is wrong. It depends on how actively you want to manage the position.

Uniswap Labs also ships a wallet app (iOS and Android) that combines a self-custody wallet with a built-in swap interface. You can buy crypto with a card, swap across chains, hold NFTs, and track your portfolio. The app also supports Uniswap's own L2 chain, Unichain, which launched in late 2025 as a purpose-built rollup for trading.

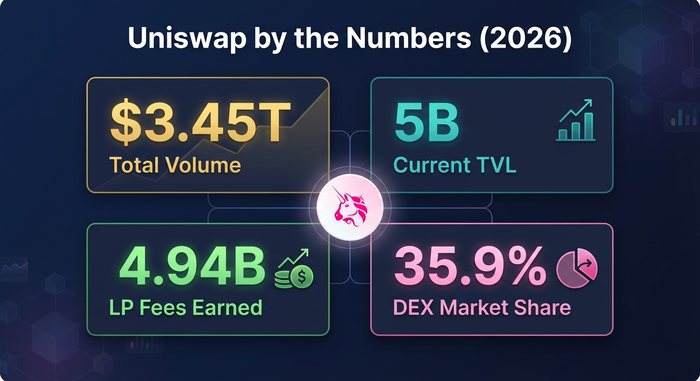

Uniswap by the numbers: the analytical picture

The data makes the case for Uniswap's dominance better than any marketing page.

| Metric | Number | Context |

|---|---|---|

| Cumulative trading volume | $3.45+ trillion | More than many traditional exchanges |

| Current TVL | ~$5 billion | Largest DEX by locked value |

| DEX market share | 35.9% | #1, PancakeSwap is #2 at 29.5% |

| Lifetime LP fees earned | $4.94+ billion | Paid to liquidity providers |

| 2025 fee revenue | ~$985 million | Growing with volume |

| Chains deployed | ~40 | Most multi-chain DEX |

| V3 pools tracked | 2,527 | $2.785B TVL |

| V4 pools tracked | 4,689 | Growing faster than v3 did |

| UNI token holders | 250,000+ (airdrop recipients) | Governance participants |

Uniswap generates close to $1 billion per year in fee revenue. The question that drove the biggest governance debate in the protocol's history: where does that money go?

The fee switch: UNIfication and what it means for UNI holders

For years, 100% of Uniswap's trading fees went to liquidity providers. UNI holders got governance rights but no direct cash flow from the protocol. That changed in December 2025 with the "UNIfication" fee switch.

Under the new structure, the Uniswap protocol itself takes a cut of LP revenue. On v3 pools, the protocol captures 16.7% to 25% of fees. On v2 pools, the split shifts to 0.25% for LPs and 0.05% for the protocol (same as SushiSwap's model, ironically). This was the most debated governance decision in Uniswap's history. LPs argued their income was being taxed. UNI holders argued that the token needed real cash flow to justify its market cap.

The result: Uniswap now has direct protocol revenue. That revenue flows to the Uniswap DAO treasury, which UNI holders control through governance votes. Whether it eventually gets distributed to token holders (like a dividend) or used for grants, development, and ecosystem growth depends on future governance decisions. As of early 2026, the treasury is accumulating but no distribution mechanism has been voted in.

The UNI token: governance, supply, and honest assessment

UNI launched in September 2020 via one of crypto's most legendary airdrops. Every wallet that had ever used Uniswap received 400 UNI tokens. Over 250,000 addresses qualified. The tokens were worth about $1,400 at launch. At UNI's peak of ~$44 in May 2021, that airdrop was worth $17,600. Free money for using a product, the kind of story that defines DeFi's appeal.

Total supply: 1 billion UNI, distributed over four years. 60% to community members (including the airdrop), 21.5% to team and future employees, 18% to investors, 0.5% to advisors. The token is now fully distributed.

UNI currently trades in the $5-8 range with a market cap of $3-5 billion. As a governance token without guaranteed cash flow (the fee switch sends revenue to the DAO, not directly to holders), UNI's value proposition is "you vote on how billions in protocol revenue gets spent." Whether that's worth a multi-billion dollar valuation is the fundamental bull/bear debate on UNI.

Unichain: Uniswap's own Layer 2

Unichain launched in late 2025 as Uniswap's purpose-built L2 rollup. Instead of deploying on someone else's rollup (Arbitrum, Optimism, Base), Uniswap built their own. The logic: if your protocol generates enough volume, running your own chain lets you capture sequencer revenue, optimize the execution environment for swaps, and reduce fees below what general-purpose L2s offer.

Early data from Unichain shows faster finality and lower fees than Uniswap on Arbitrum, which was already cheap. The chain uses the OP Stack (same technology as Optimism and Base) but with custom modifications for DEX workloads. Whether Unichain attracts enough liquidity to justify its own chain versus fragmenting users across yet another L2 is the open question. I'm cautiously skeptical. Every new chain needs to bootstrap liquidity from scratch, and the market already has too many L2s fighting for the same users. But if any protocol has the brand and volume to justify its own chain, it's Uniswap. Most volume still flows through Ethereum mainnet and Arbitrum for now. We'll see if that shifts.

Risks and honest limitations

Uniswap is the market leader. It's also not perfect.

Impermanent loss on concentrated liquidity is more severe than on v2. If you set a tight range and the price moves outside it, you're earning zero fees while holding a bag of whichever token depreciated. The Topaz Blue / Bancor study found 49.5% of v3 LPs had negative returns. Professional LPs outperform passive ones by managing ranges actively, but most retail LPs don't do this.

Smart contract risk still exists despite extensive auditing. V4's hook system introduces new complexity: each hook is essentially custom code attached to a pool. A malicious or buggy hook could drain a pool. The permissionless nature of hooks means anyone can deploy one. Users need to check what hook a pool uses before depositing.

Regulatory pressure is building. Uniswap Labs received a Wells Notice from the SEC in 2024. The outcome of potential enforcement action could reshape how the protocol operates in the US. As a decentralized protocol, Uniswap itself is hard to shut down. But Uniswap Labs, the company that maintains the frontend, is a US entity subject to US law.

MEV (maximal extractable value) means sophisticated bots front-run and sandwich trades on Uniswap, extracting value from regular users. UniswapX was designed to mitigate this through intent-based routing, but MEV remains a persistent tax on every swap. If you're trading large amounts, you're almost certainly paying an invisible MEV cost on top of the displayed fees.