AML Compliance in 2026: Costs, Deadlines, Real Penalties

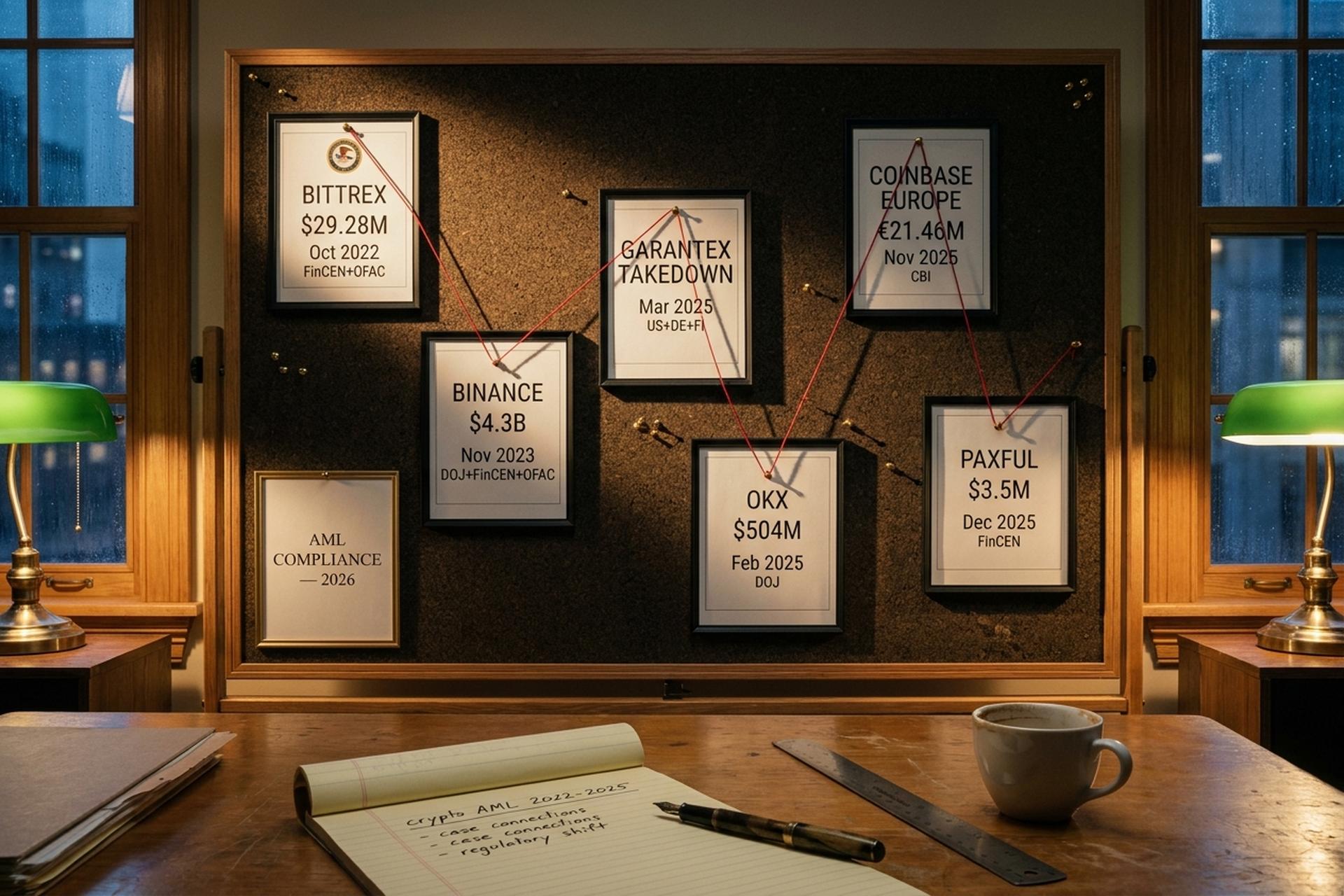

$4.3 billion. That was Binance's settlement with the US Department of Justice, FinCEN, and OFAC in November 2023, and it remains the high-water mark for crypto AML compliance failures. It is not, however, the most recent one. In February 2025, OKX paid $504 million to settle a parallel DOJ case. In November of that year, the Central Bank of Ireland fined Coinbase Europe €21.46 million for failing to monitor 30 million transactions worth €176 billion. In March 2025, Garantex's servers were seized across the US, Germany, and Finland. The pattern is clear. AML enforcement in crypto is no longer episodic. It is continuous. It is jurisdictional. It is expensive.

For any operator of a virtual asset business, AML compliance in 2026 is a seven-figure annual cost line. Three licensing tracks (EU MiCA, UK FCA, Singapore DTSP) all hit within a single twelve-month window. Stablecoins now drive 84% of all illicit on-chain volume. The financial crime threat profile has shifted faster than any compliance program written before 2024 can absorb. This is the practical state of the field, with the numbers attached.

What AML Compliance Means in 2026

AML is the legal and operational framework banks and crypto firms use to keep criminal funds out of their products. Those funds take many forms: proceeds of crime, tax evasion, fraud, ransomware payouts, sanctions evasion. The goal of any AML program is to prevent money laundering, combat money laundering schemes already in motion, and stop money laundering and terrorist financing flows from blending into the financial system. In the crypto context, the framework was extended through FATF Recommendation 16 in 2019. In the US, the Bank Secrecy Act now applies to money service businesses including crypto firms. AML sits on four operational pillars. A customer identification program (CIP). Customer due diligence (CDD) with enhanced due diligence triggers that satisfy major-framework due diligence requirements. Ongoing transaction monitoring, with a duty to report suspicious activity to the relevant financial intelligence unit. Sanctions screening. Know your customer, or KYC, is just the identification component. The harder work happens after onboarding. You have to spot suspicious transactions in real time, file the right report with the right authority on the right deadline, and do this while customers expect a frictionless product.

For a crypto business, this means a few things. You need to know your customer. You need to know what funds they are moving. You need to know where those funds came from. And you need to check that no address, name, or counterparty is on a sanctions list. The level of effort scales with risk and jurisdiction. Different countries tune the rules differently. That is where the 2026 picture gets interesting.

2026 Enforcement Scoreboard: The Cost of Getting It Wrong

What does an AML failure actually cost in 2026? The enforcement arc since 2022 is the empirical answer. Each case set a precedent, and the recent ones moved well beyond the US-only pattern.

| Date | Firm | Penalty | Authority | Why |

|---|---|---|---|---|

| Oct 2022 | Bittrex | $29.28M | FinCEN + OFAC | 116,000+ tx with sanctioned jurisdictions, $263M total |

| Nov 2023 | Binance | $4.3B | DOJ + FinCEN + OFAC | Systemic AML failures, 5-year FinCEN monitor, US exit |

| Mar 2025 | Garantex | Takedown | US + Germany + Finland | OFAC-sanctioned since 2022, continued operating |

| Feb 2025 | OKX | $504.3M | DOJ | $5B+ suspicious tx 2018-2024, $420M forfeiture + $84M fine |

| Nov 2025 | Coinbase Europe | €21.46M | Central Bank of Ireland | 30M tx not monitored over 12 months (€176B value) |

| Dec 2025 | Paxful | $3.5M | FinCEN | $500M+ suspicious flows, Iran/DPRK/Venezuela exposure |

Two patterns are worth pulling out. First, enforcement is no longer concentrated in the United States. Europol and the Central Bank of Ireland are now acting on their own. They are not waiting for AMLA's full powers. Second, the Garantex case shows that sanctions alone do not stop a non-compliant exchange. OFAC sanctioned Garantex in April 2022. The exchange ran for nearly three years. It only stopped when law enforcement physically seized the servers.

The cost of a serious AML breach now spans cease-and-desist orders, multi-billion-dollar fines, criminal monitoring, and forced market exit. Binance's $4.3 billion is still the headline. The OKX and Coinbase Europe cases set the more relevant benchmarks for a mid-size CASP looking at risk.

The Stablecoin Pivot and the Bybit Hack

Chainalysis's 2026 Crypto Crime Report shifted the frame of the illicit-finance problem. Total illicit on-chain volume reached $154 billion in 2025. That is a 162% jump from the prior year. Of that, 84% involved stablecoins, up from 63% in 2024. Sanctioned entities drove the surge. Receipts to sanctioned addresses grew 694% year over year. Almost all of that came from Russia's A7A5 ruble-backed stablecoin, which moved $93.3 billion in under twelve months. Much of it flowed through the Grinex exchange.

The signature case of 2025 is the Bybit hack. On February 21, North Korea's Lazarus Group, operating under the TraderTraitor cluster, extracted $1.5 billion in Ethereum from a Bybit cold wallet through a compromised SafeWallet front-end. Within five days, roughly $400 million had been moved through decentralized exchanges, cross-chain bridges, and conversions to Bitcoin. Zero funds were recovered. North Korean state-linked actors stole more than $2 billion across 2025, the most successful year in their history of crypto theft.

For an AML team, two things follow. First, screening counterparties with chain analytics alone is no longer enough. Laundering routes now use immutable smart contracts, atomic swaps, and bridging within hours of theft. Second, stablecoin issuers are now the most powerful choke point in the chain. A freeze on the right address by Tether or Circle is more effective than any post-hoc tracing.

The 2026 Compliance Calendar: MiCA, UK FCA, MAS

Three of the four major Western jurisdictions are hitting structural AML deadlines at the same time. All within twelve months. A crypto firm working across them needs to plan three licensing tracks in parallel.

| Jurisdiction | Framework | Deadline | Impact | Threshold |

|---|---|---|---|---|

| EU | MiCA + Transfer of Funds Regulation | July 1, 2026 | All grandfathered CASPs need full authorization; ESMA confirmed in April 2026 there will be no extensions | Zero (CASP-to-CASP) |

| EU | AMLR + AMLA supervision | July 10, 2027 | AMLR replaces AMLD5/6; AMLA direct supervision of 40 highest-risk entities | Standardised EU-wide |

| UK | FCA full crypto authorization | September 2026 | Application window opens; no automatic rollover from existing AML registration | Per regime |

| Singapore | MAS DTSP framework | June 30, 2025 (passed) | DTSP licence required for overseas-serving firms; MAS stated it will "generally not issue" one | Per regime |

| Global | FATF Recommendation 16 | Ongoing | Travel Rule: 73% of jurisdictions have legislation, 59% are not enforcing | USD/EUR 1,000 baseline |

AMLA is the new European Anti-Money Laundering Authority. It is based in Frankfurt and began formal operations on July 1, 2025. Its mandate covers both money laundering and countering the financing of terrorism. For the first time, AML/CFT regulatory compliance sits under a single EU authority. AMLA's first job is to harmonize roughly sixty fragmented national AML supervisors under a single rulebook. Direct supervision of the forty highest-risk EU entities starts in 2028. The Central Bank of Ireland's €21.5 million Coinbase Europe fine in November 2025 is an early signal. National authorities are not waiting for AMLA's full powers.

The Travel Rule gap is striking. FATF's 2025 Targeted Update found that 73% of the 117 jurisdictions permitting VASPs had passed Recommendation 16 legislation, yet 59% had still not enforced it. The EU Transfer of Funds Regulation goes further than FATF: it imposes a zero threshold for CASP-to-CASP transfers, meaning every transfer between regulated entities must carry full beneficiary information.

AML Cost: Vendor Stack and Compliance Officer Salaries

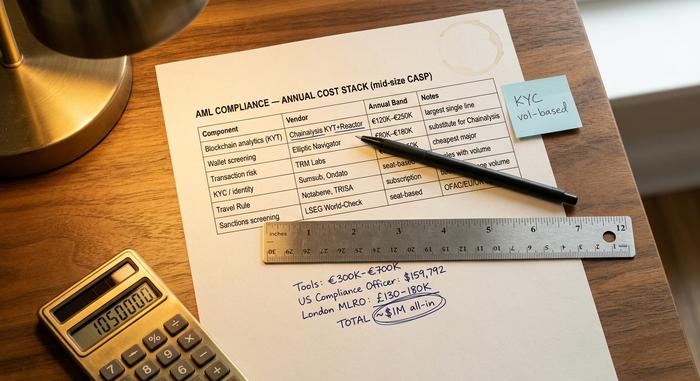

This is the part of AML compliance the educational content rarely talks about. A mid-size CASP running an in-house program faces a stack of clear line items. The numbers are not small.

| Component | Vendor examples | Annual band | Notes |

|---|---|---|---|

| Blockchain analytics (KYT) | Chainalysis KYT + Reactor | €120K-€250K | Often the largest single line item |

| Wallet screening | Elliptic Navigator | €80K-€180K | Sometimes substituted for Chainalysis |

| Transaction risk | TRM Labs | €60K-€150K | Cheapest of the major three |

| KYC / identity | Sumsub, Ondato, Trulioo | Seat-based | Scales with onboarding volume |

| Travel Rule | Notabene, Sumsub Travel Rule, TRISA | Subscription | Pricing tied to VASP message volume |

| Sanctions screening | LSEG / LexisNexis World-Check | Seat-based | OFAC SDN, EU, UK lists daily refresh |

The tooling alone for a serious mid-size operation runs €300,000 to €700,000 per year. That is before any salary cost. Then come the people. A US-based crypto Compliance Officer earns an average of $159,792 (ZipRecruiter, 2025). Chief compliance officer roles average $200,000. A London MLRO commands £130,000-£180,000 (Morgan McKinley 2025 guide). Add one assistant compliance role. The headcount line is now over $400,000 in the US or £220,000 in the UK. A serious AML program at a regulated CASP rarely runs below $1 million all-in. That includes legal counsel, audit, and infrastructure.

These figures are why the build-versus-buy question is now central to anyone entering crypto payments. AML laws and compliance stack choices can determine whether a business is viable at all.

Build vs Buy: When to Outsource AML to a Payment Processor

A small or mid-size crypto merchant does not need to staff an MLRO and license three analytics vendors. A payment processor takes on the AML obligations as the lead financial institution. The merchant integrates an API. The PSP carries the licensing, the KYC, the screening, the SAR filing, and the Travel Rule rails. This is how providers like Plisio, BitPay, and CoinGate position themselves. AML is the product, not an add-on.

The decision tree is fairly clean. Take roughly $50 million as the volume threshold. Below that, in a single jurisdiction, with no regulated VASP activity (custody, exchange, money transmission), the PSP route almost always wins. Above the threshold, in-house wins on customization, data control, and operational flexibility. The cost stops being avoidable.

The hybrid model is now dominant for medium operators. A regulated CASP uses a third-party for one or two niche services like Travel Rule routing. The key question is not which model is cheaper. It is which model puts the licensing risk in the right entity.

Tornado Cash, Smart Contracts, and the OFAC Boundary

A separate policy shift compliance teams must internalize. On November 26, 2024, the US Fifth Circuit Court of Appeals ruled in Van Loon that immutable smart contracts are not "property" under the International Emergency Economic Powers Act. On March 21, 2025, OFAC formally lifted sanctions on the Tornado Cash mixer. The criminal prosecution of co-founder Roman Storm continues, with the trial set for July 14, 2025.

What this means in practice for an AML team is precise rather than expansive. The protocol itself can no longer be sanctioned, but specific wallet addresses can be and remain on the OFAC SDN list (12,000+ entries as of March 2026). Interacting with the protocol is not, by itself, a sanctions violation. Sending funds to or receiving funds from a sanctioned address still is. Smart-contract interaction policies need to be written at the address level, not the protocol level, with screening tied to the OFAC SDN feed and equivalent EU and UK lists. The UK has consolidated its lists: as of January 28, 2026, the OFSI Consolidated List was closed, and the UK Sanctions List is now the single source.

The Crypto Travel Rule Reality Check

The Financial Action Task Force (FATF) Travel Rule, Recommendation 16, requires VASPs to transmit originator and beneficiary information for transfers above $1,000 USD/EUR. As of FATF's 2025 Targeted Update, 73% of jurisdictions permitting VASPs had passed legislation, but 59% of those had not enforced it. The EU goes further than FATF, imposing a zero threshold for CASP-to-CASP transfers under the Transfer of Funds Regulation.

On the operational side, the Notabene 2025 State of Travel Rule Report (91 VASPs surveyed) found 100% of respondents committed to Travel Rule compliance by end-2025, and a 431% year-over-year increase in firms that block withdrawals until beneficiary information is verified. The infrastructure has matured: Notabene, Sumsub Travel Rule, TRISA, and Veriscope are the operational rails. The remaining problem is interoperability between competing network providers, a fragmentation that will likely consolidate over the next two years.

What an AML Program Actually Has to Do in 2026

Stripped of the marketing layer, a 2026 AML compliance program at a crypto firm has nine concrete obligations. A designated MLRO or AML Compliance Officer with documented authority. A risk-based CIP and CDD framework with EDD triggers for high-risk customers and politically exposed persons (PEPs). Sanctions screening against OFAC SDN, EU Consolidated, UK Sanctions List, with continuous rescreening. Transaction monitoring with documented rules and thresholds. Suspicious activity reporting (SAR and CTR filing) with the relevant FIU on defined timelines. Travel Rule implementation for transfers above threshold (zero in the EU, $1,000 globally). Independent annual testing of the program. Ongoing staff training, documented and dated. Recordkeeping under the applicable retention period (typically five years).

The frameworks differ in detail, but the operational minimum is the same across FinCEN, FCA, MAS, and the post-AMLA EU. Anti-money laundering regulations and broader laws have converged faster than most operators expected. Global AML rules now cross-reference at the level of regulatory requirements, not national framework. Anti-money laundering compliance programs are more aligned across regulators than ever. Compliance efforts once stopped at correspondent banking and traditional financial services. They now extend through every regulated crypto channel. The penalty cases of 2022-2025 cluster around failures in two pillars: transaction monitoring at scale, and SAR filing on what the monitoring flagged. Build for those two first. Effective AML compliance is mostly boring work. You do those two things consistently across millions of transactions and every customer in your book.