Wealthsimple Crypto Review 2026: Fees, Coins, Bitcoin

Canadians who want to buy Bitcoin in Canada face a quiet paradox. The platform with the calmest user experience — the only one their national securities regulator has licensed as a full investment dealer — also asks them to pay the highest headline spread on the continent for buying and selling cryptocurrencies. Wealthsimple Crypto charges a casual buyer 2% per order on top of network conditions, while NDAX charges 0.20% and Newton bundles a thin spread into the BTC price. Yet Wealthsimple keeps adding clients faster than every competitor combined — so in 2026, is the trade worth it?

This review walks through what the platform actually does, what each tier costs, how it compares to Newton, NDAX, Shakepay, and Bitbuy, and how the Canada Revenue Agency treats the trades you place on it. The aim is to give a Canadian saver enough to decide whether the regulated wrapper justifies the markup.

What Wealthsimple Crypto Actually Is in 2026

Wealthsimple was founded in Toronto in September 2014 by Michael Katchen, Brett Huneycutt, and Rudy Adler. Power Corporation of Canada now holds roughly 52.4% of the firm through its Power Financial subsidiary. Wealthsimple Crypto sits inside Wealthsimple Investments Inc. That is the same legal entity that runs the stock and ETF brokerage. It matters more than it sounds. On January 1, 2024 the standalone Wealthsimple Digital Assets subsidiary was folded into the parent dealer, so a Canadian who buys Bitcoin through the app is, on paper, transacting with the same CIRO investment dealer who would sell them a S&P 500 index ETF.

That structure is unique in Canada. Wealthsimple was the first regulated crypto platform in Canada, granted entry to the CSA Regulatory Sandbox on August 7, 2020, and it has held a restricted-dealer registration ever since. Today it markets itself as fully regulated in Canada, which is technically narrower than how the broader crypto industry uses the phrase, but accurate as Canadian securities law defines it. Newton, NDAX, Shakepay, and Bitbuy all sit under separate crypto-only registrations. Those came after the Pre-Registration Undertaking process the Canadian Securities Administrators rolled out in 2022.

The scale that legal status has produced is large. As of October 2025 the company reported just over three million clients and roughly C$100 billion in assets under administration. Q2 2025 net deposits were up 93.8% year over year. A secondary share sale in October 2025 valued the firm at around US$10 billion. Most of those clients use Wealthsimple Trade or the cash account, not crypto, but the crypto product rides on the same KYC, the same fraud controls, and the same support desk.

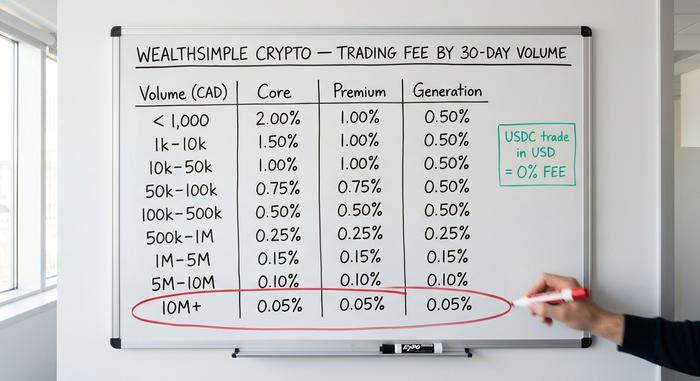

The Crypto Fee Schedule Decoded

The headline 2% per-trade fee on Wealthsimple Crypto is technically accurate and badly misleading. It applies only to Core clients, the tier most casual users sit in by default, and it applies only at the lowest 30-day volume bucket. Above that, the fee drops on a nine-step volume ladder, and it drops further if you have enough across the household to qualify for Premium or Generation status.

The full schedule of crypto fees is below. Wealthsimple charges a trading fee on each order. The rate equals the lower of the tier rate and the volume rate. It is set against the last 30 days of activity. Volumes above C$10 million in trailing thirty-day notional drop the rate as low as 0.05%, which is competitive with any global venue. Trading fees vary by tier and by token in a few edge cases, but the table covers the standard cases.

| 30-day trading volume (CAD) | Core | Premium | Generation |

|---|---|---|---|

| Under $1,000 | 2.00% | 1.00% | 0.50% |

| $1,000 – $9,999 | 1.50% | 1.00% | 0.50% |

| $10,000 – $49,999 | 1.00% | 1.00% | 0.50% |

| $50,000 – $99,999 | 0.75% | 0.75% | 0.50% |

| $100,000 – $499,999 | 0.50% | 0.50% | 0.50% |

| $500,000 – $999,999 | 0.25% | 0.25% | 0.25% |

| $1m – $4.99m | 0.15% | 0.15% | 0.15% |

| $5m – $9.99m | 0.10% | 0.10% | 0.10% |

| $10m + | 0.05% | 0.05% | 0.05% |

A few things hide inside that grid. First, the rate is a per-side trading fee on each order, not a round-trip spread. Buying and then selling at the same price costs you twice. Second, the staking program carries a separate cut. Wealthsimple keeps a percentage of staking rewards received, 30% for Core and Premium clients and 15% for Generation clients, and that number sits on top of validator commissions baked into the network return. Rewards vary by token, and the advertised yield is what reaches your account after both layers.

Third, and least advertised, USDC pays no trading fee at all when you buy or sell it against USD. That single line item rewires the platform. A Core client can fund USD through the bundled USD account, then hold Circle's stablecoin. No 2% markup applies. Every other ticker on the menu still pays it. Wealthsimple absorbs the spread inside the conversion rate, but the explicit per-order fee is zero.

The USD account itself costs C$10 per month for Core clients and nothing for Premium and Generation. It also kills the 1.5% foreign-exchange fee on USD conversions. For anyone who plans to sit in dollars between trades, that monthly fee usually pays for itself on a single five-figure conversion. Automated recurring payroll buys are exempt from trading fees entirely, which is the cleanest way Core clients save on fees and reduce trading drag without changing tiers. Special investigations cost C$75 per hour, and crypto withdrawal network fees pass through at cost.

Coins, Staking, and the Cold Storage Question

Wealthsimple lists more than 140 crypto assets, including the obvious Bitcoin and Ethereum, Solana, XRP, Cardano, Polkadot, Litecoin, and Dogecoin, along with a long tail of mid-cap altcoins on the blockchain. The two omissions worth flagging are Tether (USDT) and the Tron token (TRX). Both are deliberate compliance calls rather than oversights — USDT in particular has been a flash point in Canadian provincial securities reviews, and Wealthsimple's investment-dealer registration carries listing standards that USDT does not currently clear. Canadians who want USDT exposure to that cryptocurrency must use NDAX, Kraken Canada, or self-custody.

Stake support is narrower. Wealthsimple offers proof of stake on four coins: Ethereum, Solana, Cardano, and Polkadot, a focused way to earn crypto for long-term holders. Users stake crypto through institutional validators, the warm-up period varies by network, and reward payments hit your crypto account on the network's schedule under prevailing market conditions. Indicative net yields, after Wealthsimple's cut, hover around 4.15% for ETH and 4.5% for SOL as of early 2026, though both figures move with network conditions, so check the in-app figure before you stake coins.

Custody runs through Gemini Trust Company, which keeps the majority of customer crypto in offline cold storage. Each custodial partner carries roughly $125 million in insurance coverage, a figure last confirmed publicly in March 2024. Wealthsimple also partnered with Coincover to make sure additional ways to recover your assets exist if a key shard is lost. In the unlikely event of a custodian failure, customer crypto is held in trust at the legal level, but neither the Canadian Investor Protection Fund nor the Canada Deposit Insurance Corporation covers crypto balances. Both backstops apply only to fiat held in your linked accounts.

Wealthsimple vs Newton, NDAX, Shakepay, and Bitbuy

The Canadian crypto market has settled into roughly five viable platforms, and Wealthsimple Crypto sits at one specific corner of it: highest spread, deepest integration with non-crypto investing. The other four pull in different directions.

| Platform | Core fee structure (BTC) | Coin count | Registered (CIRO/CSA) | Stand-out feature |

|---|---|---|---|---|

| Wealthsimple Crypto | 2% trading fee + ~1.5% spread, ladder to 0.05% | 140+ | CIRO investment dealer | Integrated stock + crypto + cash account |

| Newton | ~0.5–0.7% bundled spread on BTC/ETH; 3–6% on altcoins | 80+ | CIRO restricted dealer | Cheapest BTC and ETH for casual buyers |

| NDAX | Transparent 0.20% maker / 0.20% taker | 50+ | CIRO restricted dealer | Best for active traders; FundsCAN integration |

| Shakepay | Spread-only, varies by pair and time | 8+ | CIRO restricted dealer | ShakingSats loyalty, $1 to $20 daily |

| Bitbuy | 1.50% Express, 0.20% Pro | 50+ | CIRO restricted dealer | Pro tier matches NDAX on price |

A few honest comparisons. On Bitcoin and Ethereum alone, Newton crushes Wealthsimple at every volume tier below C$100,000. NDAX wins on transparency. Its 0.20% maker-taker is the easiest fee to model, and it accepts CAD by Interac without conversion friction. Shakepay rewards heavy daily traders through its ShakingSats loyalty mechanic, and the daily Bitcoin shake-and-earn still pays out 1–20 sats per day. Bitbuy's Pro tier matches NDAX's pricing, but its Express tier sits awkwardly between Wealthsimple's simplicity and NDAX's depth.

The part that still bothers me about Wealthsimple's pricing is how few users ever realise the 2% headline is what they are paying. Wealthsimple Crypto wins exactly two things in this race. It wins on the experience for a Canadian who already holds an RRSP, TFSA, or non-registered investment account inside the same app, because the wallet, the cash management, and the equity trading all settle into one client view. And it wins on the legal wrapper: an investment-dealer registration is harder to obtain than a crypto-only restricted-dealer permit, and the firm absorbs slightly more compliance and operational cost as a result.

For everyone else, anyone who is trading crypto on volume, the price gap is wide enough that the right choice for active crypto investors is to use NDAX or Newton for accumulation, accepting lower fees in exchange for the worse user interface. NDAX is also the only Canadian venue to offer reduced trading costs alongside advanced trading features like margin and limit orders that Wealthsimple still lacks.

CIRO, CRA, and Trading Crypto on Wealthsimple

The tax and regulatory picture matters because every casual review skips it. Crypto on Wealthsimple is held in a non-registered, taxable account. The product is not eligible for TFSA, RRSP, FHSA, or RESP wrappers, and there is no legal route to put crypto into a registered Wealthsimple account today. Canadians who want crypto-adjacent exposure inside a TFSA or RRSP account must use spot ETFs like the Purpose Bitcoin ETF, not the Wealthsimple Crypto product.

Every disposition triggers a taxable event. The decision to swap crypto for another asset counts as a disposition under CRA guidance. Selling ETH to buy SOL inside the app, or any swap of one crypto for another, is two reportable transactions even though no CAD changes hands. The 2024 federal budget tried to raise the capital gains inclusion rate to two-thirds. The change was deferred and then withdrawn. The 50% inclusion rate remains in force for the 2025 tax year. Half of any net realised gain is added to income, taxed at marginal rates. Losses can offset capital gains in the current year and carry back three or forward indefinitely.

Adjusted cost base accounting is mandatory. It is the part most users get wrong. Every buy revises the average cost; every swap creates a new lot. Wealthsimple supplies a downloadable transaction history. It does not file a T5008 for crypto. The user is responsible for ACB tracking. CoinLedger, Koinly, and several other Canadian crypto-tax tools import the Wealthsimple history directly.

Form T1135, the foreign property disclosure, is the one most retail investors panic about and most do not actually owe. Crypto held with a Canadian-registered dealer is generally treated as Canadian-situs property. It falls outside the T1135 threshold. A Wealthsimple Crypto position usually does not need to be declared even if it crosses C$100,000 in cost base. Self-custodied coins or balances on offshore exchanges are a different conversation. Consult a Canadian tax specialist before the April 30, 2026 filing deadline.

CIRO membership produces one tangible protection: the Canadian Investor Protection Fund covers eligible fiat balances in your investment account up to C$1 million if Wealthsimple itself fails. CIPF does not cover crypto. Coverage applies to the CAD or USD sitting alongside your coin holdings. That difference matters in a worst-case scenario most users never plan for.

Self-Custody, Withdrawals, and USDC on Wealthsimple

For its first three years the platform refused crypto withdrawals at all, a familiar pain point. That changed gradually through 2023 and 2024. Today users can deposit and withdraw a meaningful subset of supported coins to and from external wallets, with the network for each coin specified in the help centre. Bitcoin moves on the Bitcoin network, Ethereum and ERC-20 tokens move on Ethereum, and USDC moves on Solana, Base, or Ethereum at the user's choice. A January 2026 launch added Canada Post cash deposits to the funding mix as well, which mainly matters for unbanked users.

The USDC pipeline matters because it changes what Wealthsimple Crypto actually is. Combine zero-fee USDC trades against USD, a free or C$10-per-month USD account, multi-network withdrawals, and the pilot integration with Visa Canada announced in 2024 that lets selected users spend USDC at point of sale, and the product reads less like a buy-and-hold Bitcoin app and more like a regulated stablecoin on-ramp with retail rails on top. That use case is invisible in 2% headline reviews.

Pros and Cons of Wealthsimple Crypto

The pros. Wealthsimple Crypto is the only Canadian platform inside a full CIRO investment-dealer registration. It integrates cleanly with the rest of a Canadian financial life, charges no account minimums, takes zero fee on USDC, and supports instant deposits up to C$50,000 for Core and C$250,000 for Premium and Generation. Staking covers four major proof-of-stake networks. Self-custody withdrawals work across the most-used networks, and chat support runs around the clock.

The cons. The 2% Core trading fee is high if you are not above the volume thresholds. The staking cut of 30% is steep compared to running a validator or using a no-fee staking provider. There is no margin, no futures, no advanced trading toolkit beyond limit and price-target orders. Crypto cannot sit inside a TFSA or RRSP. USDT and several mid-cap tokens are unavailable, and support runs through chat and email only.

Who Wealthsimple Crypto Is Actually For

Three honest fits. The dollar-cost averager who deposits a fixed amount per pay cycle into BTC or ETH benefits from the no-fee recurring buys and never feels the spread because the time horizon hides it. The USDC holder who wants a Canadian-regulated path between USD and a stablecoin gets the best deal on the market: zero trading fee and multi-network withdrawal. That is unusual. The active trader, who would buy and sell crypto without much regard to the registered account around it, will pay for the privilege at Wealthsimple and should use NDAX or Newton instead. The convenience premium is real — but it is a premium.