MiCA Regulation in 2026: The EU Crypto Rules Explained

Every crypto exchange that wants to keep European customers is now working toward a single deadline. By 1 July 2026, any firm offering crypto-asset services in the European Union without a licence has to stop. The rulebook that the industry spent years debating is no longer a draft. It is in force, and regulators have started to use it. The MiCA regulation, short for Markets in Crypto-Assets, is the law that crypto in Europe now runs on. And 2026 is the year the transition period runs out. This guide explains what MiCA requires, who it applies to, what it has already changed, and why a stablecoin that was fine last year can no longer trade on a European exchange.

What MiCA is and why the EU built it

MiCA is a single piece of EU legislation — Regulation (EU) 2023/1114 — that creates one set of crypto rules for all 27 EU member states. It entered into force on 29 June 2023 and replaced a patchwork that had become hard to work with. Before MiCA, a company could be a legal, registered crypto business in France under the PACTE regime. It might still have no clear right to serve customers in Germany or Spain. Each member state wrote its own rules, or wrote none at all.

The fix is a thing the EU does well when it wants to: a passport. Get one MiCA licence from a national competent authority in your home country, and you can work across the whole bloc. There is no need to apply again in each market. That single change is the reason the regulation matters so much. It does not just add compliance work; it rewires who is allowed to sell what, and where. The European Commission framed this regulatory framework as a tool for consumer protection and market integrity. For most operators, the day-to-day reality is the licence and the paperwork behind it. The clock is the part nobody can change.

MiCA's scope: markets in crypto-assets

The reach of the Markets in Crypto-Assets regulation is defined as much by what it leaves out as by what it pulls in. MiCA sorts crypto-assets into three buckets, and the bucket decides the rules.

Asset-referenced and e-money tokens

The two headline categories are both stablecoins. E-money tokens (EMTs) reference a single official currency, like a euro or dollar stablecoin. Asset-referenced tokens (ARTs) reference a basket: several currencies, commodities, or other crypto-assets. These two classes carry the heaviest rules in the framework. A token people treat as cash can do real damage if its backing turns out to be fiction.

Other crypto-assets

Everything else that is not already a regulated financial instrument falls into a catch-all third category: utility tokens, most ordinary coins, and the long tail of project tokens. The burden here is lighter. An issuer mainly has to publish an honest crypto-asset white paper and not lie in its marketing. There is no licence to issue a plain utility token, but there is liability if the disclosure is misleading.

What MiCA does not touch

This is where a lot of confusion lives. MiCA does not cover non-fungible tokens, unless they are issued in large fungible series and behave like ordinary crypto-assets. It does not cover genuinely decentralised finance where no legal entity acts as the counterparty. It does not cover central bank digital currencies. It also steps aside where an asset is already a financial instrument under older EU financial services legislation such as MiFID. Those stay under securities rules, not MiCA. The carve-outs are narrow on purpose, and "we're decentralised" is not the easy exit some projects assumed it would be.

Who needs MiCA authorisation and compliance

The honest answer is: more businesses than expected. Under MiCA, if you run a crypto exchange, hold customer coins, operate a trading platform, swap crypto for euros, place tokens, or even give investment advice on crypto-assets, you are a crypto-asset service provider and you need a licence.

Crypto-asset service providers (CASPs)

A CASP has to be a legal entity with a registered office in an EU member state and at least one resident director. That requirement quietly ended the offshore model for serving Europe. You cannot run EU crypto-asset services from a shell in a no-rules country anymore. On top of the office, there is a minimum capital requirement that scales with how risky the service is.

| Crypto-asset service | Minimum capital |

|---|---|

| Advice, order execution, placement, transfer services | €50,000 |

| Custody, administration, exchange services | €125,000 |

| Operating a trading platform | €150,000 |

| Asset-referenced token issuance | €350,000 |

Firms must also hold own funds equal to at least a quarter of their fixed overheads, whichever is higher. The application itself is heavy: business plans, governance structures, AML and IT policies, proof of capital, and fit-and-proper checks on the people in charge.

Issuers and the white paper

A token issuer that is not doing a stablecoin generally does not need pre-approval to publish. It notifies the relevant competent authority, usually about 20 working days before publishing the white paper. After that, it carries the liability if the document misleads buyers. The logic is disclosure first, punishment later, not a gatekeeper signing off on every token.

The ongoing obligations

A licence is the start, not the finish. CASPs have to meet the Digital Operational Resilience Act (DORA) for cybersecurity and ICT risk. They must apply the Transfer of Funds Regulation's travel rule, so sender and recipient data travels with each crypto transfer. They also have to segregate client assets from company funds, manage conflicts of interest, and disclose fees plainly. These are ongoing duties, spelled out in technical standards, that regulators can inspect at any time.

The largest platforms get extra attention. A provider classed as a "significant" CASP (broadly, one with more than 15 million active EU users) falls under closer supervisory oversight, with ESMA working alongside the national regulator. None of this is quick. In practice the licence file runs to hundreds of pages. The review takes months, and a firm has to keep paying staff, lawyers, and auditors through the whole wait. That cost is the real barrier, and it is why so many small operators chose not to pursue MiCA compliance at all.

E-money tokens, stablecoins and the USDT exit

Stablecoins are where MiCA bit hardest, and where the case that it overshot is strongest. Here is the number that tells the story: by early 2026, national competent authorities had authorised around 20 e-money token issuers and exactly zero asset-referenced token issuers. The ART regime is so demanding that, so far, nobody has chosen to use it.

The stablecoin rulebook

Algorithmic stablecoins try to hold a peg with code instead of reserves. They are effectively banned, because they cannot meet the reserve rules. A compliant stablecoin has to be backed one-to-one, redeemable at par on demand, and issued by an authorised credit institution or e-money institution. A meaningful share of the reserves must sit in EU bank accounts. The white paper and transparency requirements apply on top. The aim is plain: a token marketed as a euro should always be worth a euro, and the holder should always get the euro back.

The reserve rules are also where MiCA arguably pushed too far. Forcing issuers to park much of their backing in EU banks limits how they earn yield on it. The bank-only rule also shuts out the kind of independent issuer that built the dollar-stablecoin market. The zero asset-referenced token count is the clearest symptom: the regime exists, but its terms are heavy enough that not one firm has found it worth the trouble.

Why USDT left EU exchanges

Tether's USDT is the most-traded stablecoin in the world, and it never sought EMT authorisation under MiCA. So the major exchanges did the math and delisted USDT from European spot trading rather than break the rules. Binance, Coinbase, and Kraken all pulled or restricted it for EU users. For a lot of European traders, the single most visible effect of MiCA has been the loss of the pair they used most.

The euro-stablecoin reality

The replacement market exists, but it is small. Circle's EURC leads with roughly 41% of euro-stablecoin share and a market cap around $427–460 million in early 2026. The whole euro-stablecoin market still sits under €350 million, less than 1% of global stablecoin value. MiCA cleared the field of the giant and left a handful of compliant euro tokens competing for a fraction of the volume.

| MiCA-compliant euro stablecoin | Issuer |

|---|---|

| EURC | Circle |

| EURCV | Société Générale |

| EURI | Banking Circle |

| EURe | Monerium |

| EURS | STASIS |

The 2026 transition cliff for EU crypto

"Grandfathering" sounds generous, and the headline version is: firms already operating legally under national law before 30 December 2024 can keep going during a transition of up to 18 months, ending 1 July 2026. The catch is that each member state set its own length, and several slammed the window shut early. The Netherlands and Poland closed theirs around mid-2025; Germany, Austria, and Ireland near the end of 2025. So the cliff is not one date for everyone — for some firms it has already passed.

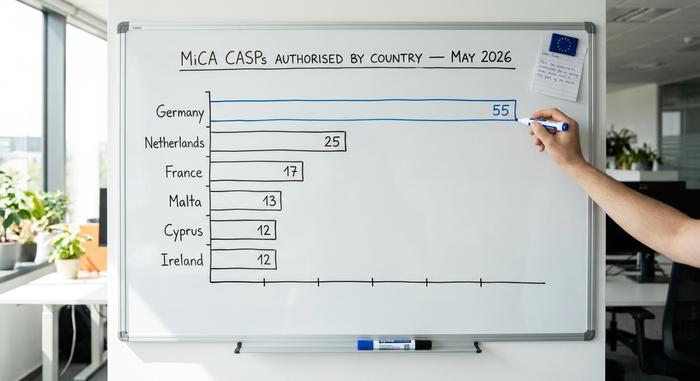

ESMA has been blunt about what comes next. It told CASPs to prepare orderly wind-down plans for when their transition ends, and warned that last-minute authorisation applications would face heightened scrutiny. Progress has been real but slow: about 204 CASPs held a licence across the EU by May 2026, and the spread is lopsided.

| Member state | CASPs authorised (May 2026) |

|---|---|

| Germany | 55 |

| Netherlands | 25 |

| France | 17 |

| Malta | 13 |

| Cyprus | 12 |

| Ireland | 12 |

Germany alone holds more than a quarter of all MiCA licences. For the thousands of smaller providers that operated under the old national registers, the path is narrower than the headline 18 months suggested.

MiCA also does not arrive alone. From 1 January 2026, a separate EU tax framework, the Crypto-Asset Reporting Framework folded into the DAC8 directive, requires service providers to collect and report customer transaction data, with the first cross-border exchanges of that information due in 2027. Layered on top of DORA and the travel rule, the compliance load is cumulative, not a single licence box to tick. A firm that clears MiCA authorisation still has to stand up tax reporting, operational resilience, and AML systems at the same time. That is part of why the licensed market is shrinking into fewer, larger players rather than growing.

Market abuse rules, penalties and enforcement

The MiCA regulation is not only a licence form. It imports the logic of securities law into crypto. There are rules against insider dealing, market manipulation, and the unlawful disclosure of inside information, all enforced by national regulators. Break the service rules and the fines run up to €5 million or 5% of annual turnover; breach the market abuse provisions and the ceiling rises to €15 million or 15% of turnover. Authorities can also revoke a licence, which shuts a firm out of all 27 markets at once.

This is not theoretical. The first notable MiCA-era enforcement came from Germany's regulator, BaFin, which ordered the winding-up of Ethena GmbH over its USDe token and imposed a €600,000 coercive fine in April 2025. The amount is modest; the signal is not. Regulators are willing to act before the transition even closes, and "we were still getting authorised" is not a defence.

What this crypto regulation means for you

For a crypto business, MiCA is a trade. You get one passport instead of 27 separate fights, and you get to tell customers you are a regulated, supervised firm. In exchange you accept a compliance bar high enough that a lot of smaller operators simply leave — consolidation in the EU crypto market is the predictable result, and it is already happening.

For an ordinary user, the deal is also mixed. European venues are safer on paper: segregated assets, real disclosures, a competent authority you can complain to. But the menu shrinks. Fewer tokens get listed, the most popular stablecoin got pulled, and non-EU platforms face limits on how aggressively they can chase European customers. Whether that is a fair price for the protection is the open question the MiCA regulation leaves on the table. What is no longer in question is that the rules apply, the deadline is real, and the regulators are watching.