When Will Digital Currency Replace Money? Country Timeline

The honest answer to when digital currency will replace money is that it depends on which country you live in and which definition of "digital currency" you accept. According to the Atlantic Council CBDC Tracker, 146 countries, representing more than 98% of global GDP, are exploring a central bank digital currency. Only three have actually launched one, and one of those has already failed in practice. Meanwhile, Norwegians pay for almost nothing in cash. Americans were told in January 2025 that no Federal Reserve digital dollar would ever exist. Kenyans have been using digital money for fifteen years without anyone calling it a CBDC.

The honest map of who is replacing cash, who is not, and what the realistic horizon looks like to 2030, 2040, and 2050 is country-by-country, not global. There is a useful answer at the end. There are no easy ones in the middle.

The 2026 Digital Money Landscape

Three competing forms of digital money are racing for the same purpose. Central bank digital currencies, often shortened to CBDCs, are state-issued tokens that aim to be a digital version of physical currency. Stablecoins are private tokens backed by fiat reserves and now regulated in the US under the GENIUS Act. Bank-rail systems like UPI in India, FedNow in the US, M-Pesa in Kenya, and the global card networks (credit and debit) are the older but vastly larger category. Bitcoin and other cryptocurrencies occupy a fourth lane — useful for store of value and cross-border transfers but rarely used for making payments at the corner shop. The question of when digital currency replaces money rarely names which one is doing the replacing.

Sweden and Norway: Where People Almost Never Use Cash

Norway is the empirical benchmark for a near-cashless economy. The Norges Bank Retail Payment Services survey for spring 2024 found cash at just 3% of all payments and 2% at the point of sale. Sweden sits below 8% of POS transactions according to the Riksbank Payments Report 2026. Neither country has issued a CBDC; Sweden's e-krona remains in pilot form. The counter-twist is striking. Both countries have legislated cash preservation. Swedish law requires merchants to accept cash, and the Riksbank is explicitly tasked with maintaining cash infrastructure. The most digitally advanced payment cultures in the world are not eliminating cash. They are protecting it as a backup.

China e-CNY: The CBDC With the Most Payments

China runs the largest CBDC by transaction volume on Earth. The People's Bank of China and the State Council reported in December 2025 that the e-CNY had processed 3.48 billion cumulative transactions worth 16.7 trillion yuan, roughly $2.37 trillion. That looks enormous until it lands next to the size of China's total payments market, where the e-CNY remains a small share. More importantly, the framework changed on January 1, 2026. The PBOC now allows e-CNY balances to earn interest, applies reserve requirements to the issuance, and extends deposit insurance to e-CNY holdings. The e-CNY has effectively been reclassified. It is no longer trying to replace physical cash; it now competes with commercial bank accounts. That is a different policy direction than "digital currency replaces money."

Nigeria, India, Africa: Digital Payment Without CBDC

The most counterintuitive lesson of the past four years sits in the Global South, where digital payment adoption has reshaped the financial system faster than any CBDC rollout. Nigeria launched the eNaira in October 2021 as one of the first national CBDCs. By 2024, IMF data put adoption at 0.5% of the population. Of 13 million wallets registered, 98.5% were inactive. Lifetime transactions totaled around ₦29.3 billion across roughly 850,000 transactions. The eNaira app was pulled from Google Play. The Central Bank of Nigeria is now forming a working group to explore a stablecoin instead.

India tells a parallel story. The RBI's e-rupee has roughly 7 million retail users despite a serious push that routed about $80 billion of welfare payments through e-rupee pilots in Maharashtra and Gujarat. Meanwhile, UPI, India's private bank-rail instant payment system, processed 228.3 billion transactions in 2025 — about 85.5% of all digital payment volumes. The daily average in February 2026 reached 743 million transactions. Cash use is falling fast in India. The instrument doing the replacing is not the CBDC.

Kenya is the cleanest case. Roughly 86.6% of the population uses mobile money. M-Pesa alone has 51 million users. Sub-Saharan Africa moved an estimated $1.4 trillion through mobile money platforms in 2025. Financial inclusion scaled through the banking system's private rails, not through any CBDC. None of this is a CBDC. Digital currency already replaced cash here, a decade before the term CBDC became fashionable.

Why the US Chose Stablecoins Over CBDCs

This is the most underreported policy story of the decade. The United States has explicitly rejected a Federal Reserve digital currency. On January 23, 2025, President Trump signed an executive order prohibiting all federal agencies from "establishing, issuing, or promoting" CBDCs, citing risks to "individual privacy" and "financial sovereignty." The decision was decisive. There will be no Fed digital dollar under the current reserve system.

The strategy instead is private. On July 18, 2025, the GENIUS Act was signed into law, creating the first US federal regulatory framework for payment stablecoins. Issuers are required to hold 1:1 reserves in cash or short-dated Treasuries, publish monthly disclosures, and meet anti-money-laundering safeguards. The result is that dollar-denominated stablecoins are now America's de facto digital currency strategy, just without the CBDC label. DeFiLlama and CoinMarketCap put the total stablecoin market cap at roughly $321 billion as of May 2026. Tether holds about $189.6 billion, or 57.96% of the market, with USDC at $77.6 billion, USDS at $8.6 billion, USDe at $5.8 billion, and DAI at $4.6 billion.

Federal Reserve research papers continue to study CBDC design as an academic exercise. FedNow, the Fed's instant-settlement service, operates as a bank-to-bank rail but is explicitly not a retail CBDC. The Federal Reserve is not going to issue a digital dollar. That has been decided.

This shifts the practical meaning of the question. Inside the US reserve system, the new forms of money are private dollar tokens with public backing, not a central bank digital currency. The OCC and the Fed are now writing prudential rules for stablecoin issuers under the GENIUS framework, focused on capital requirements, reserve segregation, money laundering controls, and bankruptcy treatment for customer claims. The aim is to make a $1 USDC and a $1 bank deposit functionally identical in trust if not in legal form. Whether that lasts will depend on whether one or two large issuers gain market dominance and whether the next administration keeps the executive order intact. For now, the US answer to "when will digital currency replace money" is that physical cash continues alongside private digital dollars, with no central bank token in the picture.

Digital Euro: Central Banks Push 2029 Issuance

The European Central Bank takes the opposite position. In a speech on March 24, 2026, ECB executive board member Piero Cipollone confirmed the operational timeline: payment service provider selection by June 2026, a 12-month pilot in the second half of 2027, and possible full issuance as early as 2029. Every part of that schedule is conditional on EU co-legislators adopting the digital euro regulation in 2026. The ECB has been explicit that it will not issue a digital euro until the legislation is in place. The eurozone position is that the digital euro will be issued alongside cash, which remains legal tender, allowing both to coexist without one forcing out the other. The framing matters: the EU is preparing to add a digital option, not retire the paper one. The Bank of England has set a similarly cautious tone for the digital pound, framing any decision as "not before the second half of the decade." The Bank of Japan continues a study phase without committing to a launch year. The pattern across Western central banks outside the eurozone is a long evaluation horizon and explicit coexistence with banknotes, not replacement.

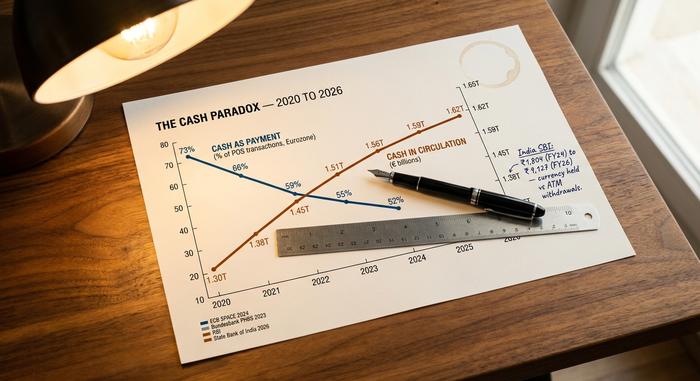

The Cash Paradox: When You Use Cash Less but Hold More

Central bank data across most major economies shows a paradox that almost never appears in payments commentary. Cash as a payment method is falling. The ECB SPACE 2024 survey of nearly 41,000 eurozone consumers put cash at 52% of POS transactions by count, down from 59% in 2022. The Bundesbank found Germany at 51% by count and 26% by value, with a 73% YouGov majority still preferring cash. McKinsey's 2025 Global Payments Report estimated global consumer cash use at 46%, down from 50% in 2023. All of these point one direction.

Cash in circulation, by contrast, is rising in most countries. The Bundesbank's split between transaction count (51% cash) and transaction value (26% cash) shows the same dynamic from inside one economy: Germans use cash for small things often and large things rarely, but they still hold the notes. A 2025 YouGov survey found 73% of German adults preferred cash over cards, up 4 points from 2024. In India, State Bank of India research reported that the gap between currency held and ATM withdrawals jumped from ₹1,804 in fiscal 2024 to ₹9,127 in fiscal 2026. People are holding more cash even as they pay with less of it. The ECB SPACE 2024 survey also asked the preference question: 62% of eurozone consumers want cash to remain available as an option, although only 22% prefer cash as their primary payment method. Cash is shifting role. It is becoming a savings instrument, a precautionary reserve, and a privacy hedge, rather than a daily payment medium. That is a very different outcome than "digital currency replaces money."

Country comparison

| Country | Cash share of payments | Main digital rail | CBDC status |

|---|---|---|---|

| Norway | 3% all / 2% POS | Cards + Vipps | None (no CBDC plans) |

| Sweden | <8% POS | Cards + Swish | e-krona pilot |

| Germany | 51% by count | Cash + cards | Digital euro pilot |

| Eurozone | 52% by count | Cards + SEPA | Digital euro 2029+ |

| Japan | ~57% | Cash + IC cards | Research only |

| China | Mid range | Alipay + WeChat Pay | e-CNY (interest-bearing 2026) |

| India | Mixed | UPI (85.5% of digital) | e-rupee (~7M users) |

| Nigeria | High | Bank apps + cash | eNaira (failed, 0.5%) |

| Kenya | Low | M-Pesa (86.6% pop) | None |

| United States | Falling | Cards + FedNow + stablecoins | Prohibited by EO |

Resilience: When Digital Payment Systems Go Dark

A grid failure across Spain and Portugal on April 28, 2025, left roughly 60 million people without electricity. ATMs went dark. Point-of-sale terminals stopped working. Mobile payment apps could not connect. For hours, in some places longer, cash was the only payment instrument that worked. The event has since been referenced by the Riksbank and the ECB as direct evidence for keeping cash in circulation even in advanced digital economies. The resilience case is the part of the cashless debate that the people pushing CBDCs least want to discuss. Digital money is fragile against power loss, network outage, and cyberattacks. A €50 note is not. Until that gap closes, no central bank is going to declare cash retired.

2030 to 2050: Forecasts for Digital Currencies

Almost no reputable institution has published a numerical "year cash disappears" forecast. The closest available signals are partial.

| Horizon | Best-evidence forecast |

|---|---|

| By 2030 | BIS 2024 survey estimates up to 15 CBDCs in public circulation, around 9 wholesale CBDCs active. Juniper Research projects 7.8 billion CBDC transactions in 2031 (versus Visa's 200+ billion per year today). |

| By 2040 | No major institution has published a specific cash-replacement target. McKinsey's projection trajectory (50% in 2023, 46% in 2025) would put global cash use somewhere in the 25-35% range by 2040 if linear, but trajectories rarely stay linear. |

| By 2050 | No serious institutional forecast exists for a fully cashless world. WEF Davos has produced aspirational "100% digital" statements without dates. The honest answer here is that the question loses meaning at this horizon. |

There is one extra signal worth pulling out. Wholesale CBDCs — central bank settlement tokens used between banks, not by households — are moving faster than retail CBDCs. The mBridge project, run by the BIS Innovation Hub with the central banks of China, Thailand, the UAE, and Hong Kong, has cleared roughly $55.49 billion in cross-border transactions, a 2,500x increase from early 2022 levels. A wholesale digital currency could quietly become the part of the CBDC story that actually scales, while retail CBDCs remain symbolic in most jurisdictions.

The honest synthesis is that digital currency has already replaced cash for daily payments in roughly six to eight countries, and widespread adoption of some digital form is gaining traction across most of the rest. It will replace cash for daily payments in another fifteen to twenty within a decade. It will not eliminate physical cash in most economies by 2040, and probably not by 2050 either, because cash is shifting role rather than dying. The right question is not when digital currency will replace money. The right question is which form of digital money will dominate each use case, and what role the residual cash supply plays in resilience and financial inclusion. On that question, the timeline answers itself country by country.