Flare Network (FLR): 3 Years In, What Was Built

There is a rift in the Flare Network story between what the price chart says and what the protocol has actually shipped. FLR trades near $0.0084 in May 2026 with a market capitalisation around $727 million, ranked roughly #85 by CoinGecko. That is about 94 percent below its all-time high of $0.1501, printed on the token's first day of trading in January 2023. The chart is brutal. The build log is something else: a fully live FTSO with a hundred independent providers updating a thousand price feeds every 1.8 seconds, a FAssets mainnet that opened a five-million-FXRP minting cap and filled it in four hours, a Google Cloud-run validator, and a fresh governance proposal in April 2026 that cuts annual inflation by 40 percent and introduces MEV-capture burns. Both stories are real, and reconciling them is the only honest way to write about Flare in 2026. Most coverage picks one and ignores the other.

The question worth asking three years in is not whether Flare's TGE went badly — it did — but whether the protocol that came out the other side is something different. What surprises me about Flare is how rarely either camp engages the other; the people pointing at the chart almost never read the changelog, and the people defending the build almost never explain why $0.0084 is the right price for it. This profile walks through the founding story, the two-year XRP airdrop delay, how the network actually works as a blockchain interoperability layer, where FLR tokenomics stand after FlareDrops ended, what is genuinely live in the ecosystem for decentralized applications, and where Flare lands against Chainlink and the broader oracle market for crypto data feeds.

The Spark-to-FLR backstory and the two-year airdrop delay

Flare was announced in August 2020 by three founders with academic and trading backgrounds: Hugo Philion (CEO), Sean Rowan (CTO), and Dr. Naïri Usher (Chief Scientist). The original pitch was a layer-1 blockchain that would bring smart contracts to assets historically excluded from them: XRP first, then Litecoin, Dogecoin, and eventually Bitcoin. To bootstrap the network's community, the team announced a 1:1 airdrop of the native token (then called Spark) to all XRP holders captured in a December 12, 2020 snapshot.

The snapshot happened on time. Everything afterwards did not. Between regulatory headwinds around XRP, technical readiness, and a redesign of the distribution mechanics, the token generation event slipped from "early 2021" through multiple delays. FIP.01, an early Flare improvement proposal, restructured the airdrop into a phased distribution: 15 percent of the allocated supply at TGE, the remainder spread across thirty-six monthly FlareDrops.

The token was rebranded from Spark to FLR in October 2022. The TGE finally happened on January 9, 2023, more than two years after the snapshot. Around 4.278 billion FLR were distributed in the initial drop. The price hit $0.1501 on day one, then dumped roughly 70 percent within hours as the airdrop went liquid. CoinDesk's day-after coverage captured the mood. Three years on, that opening-day candle is still the all-time high.

The FlareDrops program ran on schedule from there. The final monthly distribution settled on January 30, 2026. From that point forward, no new FLR has been entering the market through the airdrop mechanism. The token's circulation now lives or dies on the protocol's economic design.

How Flare actually works: FTSO, FDC, and FAssets

Flare is an EVM-compatible layer-1 blockchain that runs a modified Avalanche consensus combined with Federated Byzantine Agreement. The setup matters because it lets the chain do something most general-purpose L1s outsource: bake oracle services and cross-chain attestation into the protocol itself.

Three protocols carry the weight.

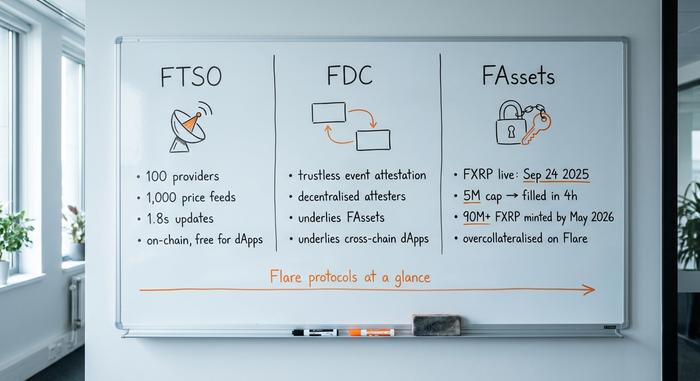

The first is the Flare Time Series Oracle, or FTSO. This is Flare's most-cited piece of infrastructure. About a hundred independent providers stake influence in the system and submit price quotes for roughly a thousand assets. Updates land roughly every 1.8 seconds. Because the oracle is enshrined at the chain level, Flare-native dApps consume those feeds without paying per call. That is the structural pitch against Chainlink, where every read costs LINK gas. Whether free-on-chain feeds actually win business is its own argument, but the data layer is live and has been since mainnet.

The second is the Flare Data Connector, or FDC. Originally launched as the State Connector, the FDC handles trustless attestations of events on external blockchains. The use case is "did this XRP payment happen, did this Bitcoin transaction confirm, did this off-chain event occur," answered by a decentralised set of attesters rather than a bridge multisig. It is the technical foundation underneath FAssets and any cross-chain dApp built on Flare.

The third is FAssets. This is the product most likely to define whether Flare matters. FAssets lets a non-smart-contract asset like XRP be locked on its native chain and minted as a synthetic token on Flare with overcollateralisation, giving holders DeFi access without giving up the underlying. FXRP, the first FAsset, went live on mainnet on September 24, 2025. The initial five-million-FXRP minting cap filled in four hours. By May 2026, more than 90 million FXRP had been minted across the network. The on-paper goal extends to FBTC and FDOGE, but only the XRP version is mainnet-confirmed at the time of writing.

Songbird is the canary network, with Coston and Coston2 as testnets. Google Cloud has been operating both a validator and an FTSO provider since January 15, 2024. That is a notable institutional signal, but not by itself proof of broader enterprise adoption.

| Protocol | What it does | Live since | Concrete metric |

|---|---|---|---|

| FTSO | On-chain decentralized oracle for price feeds | Mainnet 2022 | 100 providers, 1,000 feeds, 1.8s updates |

| FDC | Trustless cross-chain event attestation | Mainnet 2022 (as State Connector) | Underlies FAssets + cross-chain dApps |

| FAssets (FXRP) | Synthetic asset minting from non-smart-contract chains | Sep 24, 2025 | 5M cap filled in 4h; 90M+ FXRP minted by May 2026 |

FLR tokenomics: from FlareDrops to MEV burns

FLR's economic design has shifted twice. The genesis design was built to bootstrap a community: 100 billion FLR at launch, roughly 10 percent annual inflation, a 58.3 percent public allocation, and monthly FlareDrops distributing the original XRP airdrop over three years. With FlareDrops concluded in January 2026, that phase is over.

The new economic chapter sits in FIP.16, a governance proposal published in early April 2026. Two changes matter most. First, annual inflation is hard-capped at roughly 3 billion FLR per year, down from a previous trajectory near 5 billion. That is a 40 percent cut. Second, the protocol introduces MEV-capture burns: a share of the maximal extractable value generated on Flare blocks is destroyed rather than paid out, redirecting that value back to existing holders. Flare's own estimates put the burn growing from around 7.5 million FLR per year today to roughly 300 million per year as MEV activity matures. CoinDesk covered the proposal on April 10, 2026.

The token's day-to-day utility has not changed. FLR pays transaction fees, denominates governance votes, and serves as collateral inside FAssets. Wrapping FLR into WFLR remains the prerequisite for delegating to FTSO data providers and earning the associated rewards. For token holders, the practical effect of FIP.16 is that passive supply growth slows while burn pressure ramps up over time — a meaningful change from the FlareDrops era.

| Metric | Value (May 2026) | Source |

|---|---|---|

| Price | ~$0.0084 | CoinGecko |

| Market cap | ~$727M | CoinGecko |

| Circulating supply | 86.27B FLR | CoinGecko |

| Total supply | 105.87B FLR | CoinGecko |

| Max supply | No formal hard cap (FIP-defined schedule) | Flare Dev Hub |

| All-time high | $0.1501 (Jan 10, 2023) | CoinMarketCap |

| All-time low | $0.007261 (Apr 7, 2026) | CoinMarketCap |

| 24h volume | ~$2.9M (CoinMarketCap) | CMC |

| Top exchanges | Kraken, Coinbase, Bitvavo, KuCoin, Bitget | CoinGecko |

The structural argument bears repeating: with FlareDrops ended and FIP.16 active, FLR supply growth flips from "tilted upward by scheduled distribution" toward "balanced against MEV burns and capped inflation." Whether that shifts the supply/demand picture meaningfully depends on real MEV activity, which depends on real on-chain usage.

Flare Network ecosystem: TVL, SparkDEX, and the USD₮0 spike

The numbers that matter on Flare in 2026 are not the price chart. Total value locked on the network sits around $200 million, having grown roughly 410 percent between February 2024 and February 2025 according to Flare's own DeFi reporting. The growth is concentrated in a handful of native dApps — small in absolute terms relative to top-tier ecosystems, but a working set of decentralized applications nonetheless.

SparkDEX is the largest. DeFiLlama lists its TVL near $29.89 million in May 2026, with cumulative DEX volume above $2.52 billion since launch. Kinetic Market handles lending. Enosys and Bunny operate as DEX/aggregator products. The mix is small relative to Ethereum or Solana, but it is a working DeFi stack with real users.

A specific moment worth noting is the USD₮0 launch in early 2025. The stablecoin's circulating supply on Flare jumped from about $37 million to $155 million inside two weeks. Whether that liquidity stays depends on yields and integrations, but the spike showed the network can absorb stablecoin flow quickly when the rails exist.

FXRP belongs in this section too. Ninety million-plus minted units, with the initial cap absorbed in four hours, suggest pent-up demand for XRP-into-DeFi access. The next test is whether those FXRP units circulate inside Flare DeFi or sit dormant in wallets. Minting volume alone does not prove utility — daily transfer counts, share of FXRP routed through SparkDEX, and share posted as collateral in lending markets are the real tells. Those numbers are not yet at the scale where they would force a re-rating, but the trajectory between now and the next quarter will be the cleanest read on whether FAssets is a structural product or a one-week launch story.

Where Flare stands against Chainlink and other oracles

The oracle market for cryptocurrencies is not a contest of equals. Chainlink holds something close to 70 percent of the oracle market by integrations, with total value secured north of $100 billion across networks and a market cap around $6.5 billion. Flare's $727 million market cap is roughly a ninth of Chainlink's. Pyth, Band, and RedStone fill the remainder, each with a niche.

Flare's pitch is not "displace Chainlink." It is structural: on Flare, the oracle is the chain. Native dApps read FTSO feeds without paying per call, which removes a recurring operating cost that pure-oracle integrators absorb. The catch is that the pitch only works if developers choose to build natively on Flare rather than use Chainlink on Ethereum or Solana, and integrators rarely switch oracles once committed.

The second piece of Flare's argument is that FAssets is something Chainlink does not ship. Pure oracle networks do not issue synthetic assets. If FAssets actually becomes a meaningful route for XRP holders, Bitcoin holders, or Dogecoin holders to access DeFi, that is a distinct product category, not a head-to-head fight with the data oracle incumbent.

Risks and signals worth watching on Flare Network

Five concrete risks deserve a place on any Flare watchlist.

First, sector beta. FLR's chart over the past three years has tracked altcoin and oracle sector flows more closely than its own product milestones. Even FAssets mainnet did not produce a sustained re-rating. A weak sector keeps FLR weak regardless of execution.

Second, the FXRP demand-supply gap. Minting 90 million-plus FXRP looks impressive, but the next test is whether those tokens transact and earn yield inside Flare DeFi, or sit dormant in wallets. Circulation, not minting, is the real signal.

Third, FIP.16 execution risk. MEV-capture burns are a relatively novel protocol-level mechanism. The Flare team's burn projections grow from around 7.5 million FLR per year today to about 300 million per year over time — but the upper end of that range depends on actual MEV opportunities materialising on Flare blocks. If on-chain activity stays modest, the burns stay modest.

Fourth, the Chainlink moat. Integrators rarely switch oracles. Flare needs new dApps that are Flare-native, not migrants from Ethereum or Solana — and native developer recruitment is slow work in a competitive L1 market.

Fifth, post-FlareDrops engagement. Through January 2026, monthly drops gave existing FLR holders a real reason to stay engaged. From February 2026 onward, the only reasons are delegation rewards, FAssets utility, and governance participation. If those alone fail to retain holders, dormant supply could move to exchanges.

Final thoughts on Flare three years in

Flare's chart says "delayed promise." The FTSO uptime, the FAssets mainnet absorbing its initial cap in four hours, the Google Cloud validator, and the FIP.16 economic redesign say "still building." Both reads are accurate. The next twelve months — FXRP circulation inside DeFi, MEV-burn execution, post-FlareDrop holder retention — will determine which signal carries. The structural pieces of the Flare Network oracle-and-cross-chain L1 are in place. Whether the FLR token captures the value those pieces produce is now the only open question.