What Is BlackRock BUIDL? The Tokenized Treasury Token

The world's largest asset manager has moved billions of dollars of US Treasuries onto public blockchains, and a qualified investor can now cash out of that position into a stablecoin at three in the morning. The product that does this is BlackRock BUIDL. It is not a meme coin, not a speculative bet, and not something most readers can actually buy. It is something more consequential: the clearest sign yet that Wall Street believes government debt belongs on-chain.

This article explains what BlackRock BUIDL is, how the token works, what it holds, who can own it, and why a fund that excludes almost everyone has become one of the most important objects in crypto. The short version is that BUIDL turned a money market fund into a tokenized fund a blockchain can carry, and the rest of the industry is quietly building on top of it.

What BlackRock BUIDL Actually Is

BUIDL is not a coin you trade on an exchange. It is a tokenized money market fund. Its full name is the BlackRock USD Institutional Digital Liquidity Fund, and each token is designed to hold a steady value of $1.00, backed by short-term US government assets rather than by hope.

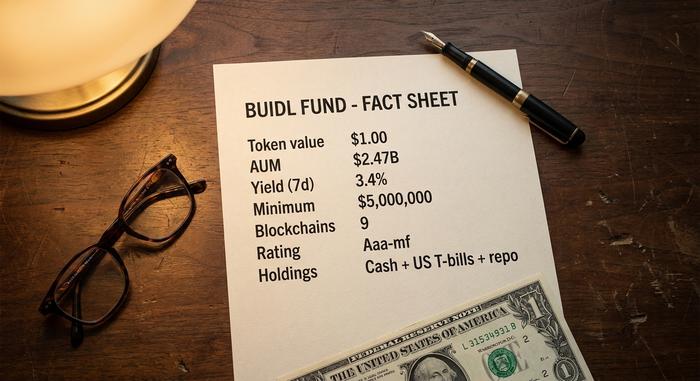

The fund launched on March 20, 2024, built with Securitize, the firm that handles its tokenization and acts as transfer agent. Since then it has grown into the second-largest tokenized-treasury product on the market, holding about $2.47 billion in assets, according to rwa.xyz as of June 2026. The fund crossed its first billion dollars within a year of launch, a pace that is fast for any new fund and almost unheard of for one settling on a blockchain.

Where a stablecoin gives you a dollar that sits there, BUIDL gives you a dollar that earns the yield on US Treasury bills while living on a blockchain. That single difference — a regulated fund share that moves like crypto — is what made BlackRock's experiment matter.

How the BUIDL Token Works On-Chain

The clever part of BUIDL is not the blockchain itself. It is that a regulated fund share can behave like a token on a public network while the actual assets sit safely in traditional custody off-chain. That split is the whole design.

One token, one dollar

When a qualified buyer subscribes, the fund mints BUIDL tokens at a rate of one token per US dollar. Redeem, and the tokens are burned. The price is engineered to stay at a stable value of $1.00 rather than float, so the token works as a unit of value rather than a speculative asset. In that sense it resembles a stablecoin, but the resemblance ends at the price.

Daily dividends paid as new tokens

Here is where BUIDL diverges from a plain stablecoin. The fund earns interest on its holdings, and that yield accrues to investors daily. Instead of pushing the token price above a dollar, the fund pays the yield out as additional tokens dropped straight into each holder's wallet, with these daily dividend payouts settled monthly. Cumulative on-chain dividend payouts passed $100 million by late 2025, as CoinDesk reported. You hold more tokens over time, each still worth a dollar.

Whitelisted transfers and custody

BUIDL is not freely transferable. A token can only move between wallets that have passed Securitize's onboarding checks, which keeps the fund inside its regulatory perimeter. Securitize acts as the SEC-registered transfer agent, BNY Mellon serves as custodian and administrator of the underlying assets, and approved digital-asset custodians including Anchorage, BitGo, Coinbase, and Fireblocks hold the tokens, giving large investors flexible custody options. The crypto part is visible onchain; the trust part is built on very traditional institutions.

What BUIDL Holds and the Yield It Pays

BUIDL is boring on purpose, and that is the point. It does not chase yield in risky corners of the market. It holds short-dated US government debt, and it pays whatever that debt pays.

| Detail | BUIDL |

|---|---|

| Token value | $1.00 (stable) |

| Assets under management | ~$2.47B (Jun 2026) |

| Yield (7-day) | ~3.4%, rate-dependent |

| Holdings | Cash, US T-bills, repo |

| Minimum investment | $5,000,000 |

| Blockchains | 9 |

| Launched | March 2024 |

| Custodian | BNY Mellon |

| Transfer agent | Securitize |

| Rating | Moody's Aaa-mf |

The portfolio

The fund invests its assets in cash, US Treasury bills, and repurchase agreements, with maturities kept short. There is no credit risk hunting and no exotic collateral. This is the same plumbing that underpins a conventional institutional money market fund, simply wrapped so a blockchain can carry the shares.

Short maturities are the safety mechanism. Because the bills mature within roughly three months, the fund is never far from cash, which is what lets it hold a steady dollar and meet redemptions without selling at a loss. It is the least exciting way to earn yield in crypto, and that is precisely why a cautious treasurer can defend holding it.

The yield, and why it changed

The yield is whatever short-term Treasuries pay, which means it moves with interest rates. As of June 2026 the seven-day rate sat near 3.4%, per rwa.xyz, down from the 4.5% to 5% figures quoted when the fund launched in the higher-rate environment of 2024. This matters: BUIDL is not a fixed promise of return. When the Federal Reserve cuts, BUIDL pays less, the same as the bills it holds.

Fees and the Aaa rating

BlackRock charges a unitary fee in the range of 0.20% to 0.50% a year, netted out of the yield. In May 2026, Moody's assigned the fund a top Aaa-mf rating, as CoinDesk noted, a credential that matters more to a pension desk than to a degen, and that is exactly the audience BlackRock is courting.

Which Blockchains Does BlackRock BUIDL Use?

BUIDL did not stay on one network for long. It launched on Ethereum and now runs across nine blockchains, including Solana, Avalanche, Aptos, Arbitrum, Optimism, Polygon, and BNB Chain, with cross-chain, peer-to-peer transfers handled by the Wormhole bridge. Spreading across chains lets the fund sit wherever institutional liquidity already lives.

The genuinely new feature is the exit. Through a Circle smart contract introduced in April 2024, holders can redeem BUIDL for USDC instantly, around the clock, without waiting for a traditional settlement window. A later facility, Grove Basin, added up to $1 billion a day of additional USDC liquidity from May 2026.

Think about what that means against the old system. A conventional money market fund redeems on business days, during business hours, with cash hitting your account a day or two later. BUIDL turns that into an on-chain transfer that clears in seconds, at any hour, on any day. A Treasury fund that settles on weekends and at midnight simply did not exist before this, and that combination of government-grade safety with always-on liquidity is the part traditional finance finds hard to dismiss.

Who Can Invest in the BUIDL Token

Here is the catch for most readers: you almost certainly cannot buy it. BUIDL is a private placement under Reg D, sold only to US qualified purchasers who are also accredited investors, plus eligible non-US buyers. Subscriptions run through Securitize Markets, the registered broker-dealer arm that handles the paperwork, identity checks, and wallet whitelisting before a single token is issued. The minimum investment is $5,000,000, and even redemptions carry a $250,000 floor.

A qualified purchaser, in plain terms, is an entity or person with at least $5 million in investments, a bar set far above the accredited-investor threshold that already excludes most households. So BUIDL is not gated by a paywall you can clear with effort; it is gated by a wealth test written into US securities law.

That excludes essentially all retail investors by design. BlackRock built BUIDL for institutions, corporate treasuries, and crypto-native firms that need a yield-bearing dollar they can hold on-chain and move between counterparties. If you are an individual reading this, your realistic path to BUIDL is indirect, through the growing list of products that use it as a building block. Which brings us to why this matters far beyond its investor list.

Why BUIDL Matters: Collateral and DeFi

What I find most striking about BUIDL is not its size. It is that the token is quietly becoming the risk-free yield layer underneath crypto, the thing other products are built on rather than the thing people hold.

Tokenized Treasuries as the new collateral

The wider market for tokenized US Treasuries reached about $14.81 billion in June 2026, according to rwa.xyz, and BUIDL accounts for roughly 17% of that market cap. In November 2025 Binance began accepting BUIDL as off-exchange collateral for institutional trading, so a desk can post a yield-bearing Treasury token instead of an idle stablecoin. That single shift, earning while you trade, is why institutions keep asking for more of this. Idle collateral is dead weight; collateral that pays the Treasury rate is not.

Backing stablecoins and DeFi yield

BUIDL has also crept into the foundations of decentralized finance. Ethena's USDtb is backed roughly one-to-one by BUIDL reserves, Ondo's OUSG launched with a large BUIDL allocation, and Frax approved BUIDL as backing for its frxUSD stablecoin. A wrapped version, sBUIDL, lets the token plug into DeFi lending protocols. Each integration turns BlackRock's Treasury fund into collateral that other dollars are minted against.

What it signals for tokenization

Strip away the detail and BUIDL is a statement that real-world asset tokenization has cleared its most important credibility test. The largest asset manager on earth decided it was worth doing with its own name attached, and regulators, custodians, and auditors went along with it. That is a different signal from a startup promising the future. It is the establishment building the rails itself.

It also reframes a long-running argument in crypto. For years the pitch was that public blockchains would route around banks and asset managers. BUIDL points the other way: the incumbents are adopting the technology and keeping the trust relationship, the custody, and the compliance. Whether you find that reassuring or disappointing depends on what you wanted crypto to be. Either way, it is now the direction the money is taking.

BUIDL vs a Stablecoin: The Key Difference

BUIDL is often mistaken for a yield-bearing version of USDC. Legally, it is closer to the opposite. Both tokens aim to hold a dollar, but one is open money and the other is a restricted security.

| Feature | BUIDL | USDC | Bank MMF |

|---|---|---|---|

| Value | ~$1.00 | ~$1.00 | ~$1.00 |

| Pays holder yield | Yes | No | Yes |

| Who can hold | Qualified only | Anyone | Brokerage clients |

| On-chain transfers | Whitelisted | Permissionless | None |

| Legal wrapper | Securities fund | E-money/reserve | Mutual fund |

A stablecoin like USDC is permissionless and pays its holders nothing; the issuer keeps the interest. BUIDL pays the yield to its holders but locks down who can hold it and where it can move. That trade — yield in exchange for permission — is the whole distinction, and it explains why the two products are converging in practice even as they stay opposite in law. Stablecoin issuers increasingly park their reserves in instruments like BUIDL, so the yield a stablecoin refuses to pay you often ends up earned on a Treasury token behind the scenes. If you want a dollar anyone can send, you want a stablecoin. If you want a regulated dollar that earns, and you clear the $5 million bar, you want BUIDL.

The Bottom Line on BlackRock BUIDL

BUIDL is TradFi's biggest bet that Treasuries belong on-chain. It took the dullest, safest instrument in finance, a short-term government bond fund, and proved it could live on a blockchain with daily yield and instant redemption, while keeping the custody and compliance that institutions demand.

Most people will never hold a single BUIDL token. That is fine, because its real influence runs through everything built on top of it: the stablecoins it backs, the collateral it becomes, the yield it passes into DeFi. So the question worth watching is not whether you can buy BUIDL. It is what gets built on it next, because that is where the rest of us finally meet it.