What Is FBTC? Fidelity’s Spot Bitcoin ETF Explained

When a 75-year-old asset manager that oversees trillions of dollars decides to put Bitcoin inside a brokerage wrapper, that is worth paying attention to. FBTC is Fidelity's answer. It lets you buy Bitcoin exposure through the same account you use for stocks, no crypto exchange and no private keys required. The interesting part is not just what FBTC is, but how it stacks up against the rest of the spot Bitcoin ETF field, especially BlackRock's IBIT.

This guide breaks down what FBTC actually holds, how a spot Bitcoin ETF works, what makes Fidelity's version different, and how it compares on fees and size. None of this is financial advice. It is the context you need before deciding whether a fund like this belongs in your portfolio.

What Is FBTC, the Fidelity Bitcoin Fund?

FBTC is the ticker for the Fidelity Wise Origin Bitcoin Fund, a spot Bitcoin exchange-traded fund that trades on the Cboe BZX exchange. It launched on January 11, 2024, the same day a wave of spot Bitcoin ETFs got the green light from US regulators. "Spot" is the key word. The fund holds real Bitcoin, not futures contracts, so each share represents a small slice of an actual pile of BTC sitting in custody. The fund's investment objective is simple: track the price of Bitcoin, minus costs.

That makes FBTC very different from the wrapped-Bitcoin tokens you find in DeFi. It is a regulated investment product, bought and sold like any stock during market hours. You do not hold the Bitcoin yourself. You hold shares of a fund that holds the Bitcoin for you. For a lot of people, especially those already inside a brokerage or retirement account, that trade-off is the whole appeal. The fund currently holds about 179,670 BTC on behalf of its shareholders, which is roughly 0.85% of all the Bitcoin that will ever exist. That is a striking amount of supply locked inside one regulated product.

How a Spot Bitcoin ETF Actually Works

The mechanics matter, because they explain why the share price tracks Bitcoin so closely. Behind the scenes, large firms called authorized participants create and redeem big blocks of shares. When demand rises, they deliver assets to the fund and receive new shares; when it falls, they hand shares back and take assets out. This constant arbitrage keeps the market price tethered to the fund's net asset value, the worth of the Bitcoin it holds. Unlike a mutual fund, which prices just once a day, FBTC trades intraday like an ordinary stock.

FBTC prices its Bitcoin against the Fidelity Bitcoin Reference Rate, then subtracts its small annual fee. The result is a share price that moves almost exactly with the spot price of Bitcoin, minus costs. One nuance worth knowing: until 2025, these funds settled creations and redemptions only in cash. In July 2025, US regulators approved in-kind creation and redemption for all spot Bitcoin ETFs, as CoinDesk reported, letting participants swap shares directly for Bitcoin. It is a plumbing change, but it made these funds cheaper and cleaner to run. FBTC also gained listed options in late 2024, which let institutions hedge and build strategies around the fund. Another sign it has graduated into mainstream market infrastructure rather than a novelty.

Fidelity's Self-Custody Difference

Here is where FBTC genuinely stands apart, and it is the detail most explainers skim past. Almost every other spot Bitcoin ETF, including BlackRock's giant IBIT, parks its Bitcoin with a third-party custodian: Coinbase. Fidelity does not.

Why custody matters for a Bitcoin ETF

An ETF is only as safe as the Bitcoin behind it, and Bitcoin is a bearer asset. Whoever controls the private keys controls the coins. So the custodian is not a footnote. It is the entity standing between investors and a catastrophic loss if keys are mishandled or stolen. With most spot Bitcoin funds, that responsibility sits with one company, Coinbase, which creates a quiet concentration risk across the whole sector.

Fidelity Digital Assets vs Coinbase Custody

Fidelity custodies the Bitcoin in-house, through its own subsidiary, Fidelity Digital Asset Services, a New York-regulated trust company. The Bitcoin is held mostly in cold storage, disconnected from the internet, with roughly 98% kept offline. This vertical integration means Fidelity is not outsourcing the single most sensitive part of the operation. For investors who already trust Fidelity with their retirement savings, having the same firm hold the keys is a real, if understated, selling point. It also means FBTC is not exposed to the same single custodian as most of its rivals.

FBTC Fees: the 0.25% Expense Ratio

FBTC charges an annual expense ratio of 0.25%, per Fidelity. On a $10,000 position, that works out to about $25 a year, skimmed gradually from the fund rather than billed to you directly, the way management fees work in any fund. At launch Fidelity waived the fee entirely, charging 0.00% through July 31, 2024, to attract early assets. After that, the standard 0.25% kicked in.

How does that stack up? It is squarely mid-pack. It matches IBIT's 0.25% exactly, undercuts Grayscale's GBTC at a steep 1.5%, and sits slightly above the cheapest funds from Bitwise and ARK. Bitwise's BITB at 0.20% and ARK's ARKB at 0.21% shave a little more off, and over a decade those hundredths of a percent do compound. But for a buy-and-hold investor, the difference between 0.20% and 0.25% is rarely the deciding factor. Custody, platform, and liquidity usually matter more.

FBTC vs IBIT, GBTC, ARKB and BITB

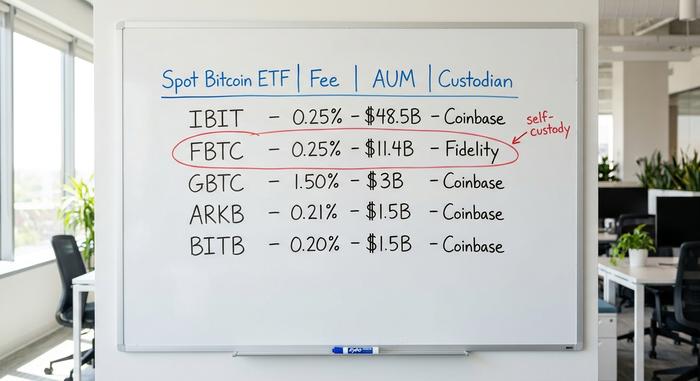

This is the comparison most readers actually came for. The spot Bitcoin ETF market is large and lopsided, with two funds dominating. As of June 2026, the eleven-plus US spot Bitcoin ETFs held a combined $79.4 billion in assets, according to Bitbo.

| ETF | Issuer | Fee | Custodian | AUM (Jun 2026) |

|---|---|---|---|---|

| IBIT | BlackRock | 0.25% | Coinbase | ~$48.5B |

| FBTC | Fidelity | 0.25% | Fidelity Digital Assets | ~$11.4B |

| GBTC | Grayscale | 1.50% | Coinbase | ~$3B |

| ARKB | ARK 21Shares | 0.21% | Coinbase | ~$1.5B |

| BITB | Bitwise | 0.20% | Coinbase | ~$1.5B |

Why IBIT pulled ahead of FBTC

FBTC and IBIT launched on the same day with nearly identical fees, yet IBIT now holds more than four times the assets. BlackRock's distribution muscle and its iShares brand simply pulled in institutional money faster. FBTC is a clear and comfortable number two, with roughly a 14% share of the market, but the gap with IBIT has widened, not closed, since 2024. Even so, FBTC has drawn more than $10.4 billion in cumulative net inflows since launch, according to Farside Investors. That is real, sticky money, not a rounding error.

Where FBTC has the edge

Size is not everything. FBTC's self-custody is a structural differentiator IBIT cannot easily copy, and for investors already living inside the Fidelity ecosystem, buying FBTC is frictionless. If you keep your IRA at Fidelity, FBTC is the native choice. That distribution advantage is quietly powerful.

FBTC Key Facts and Fund Details

A quick reference for the numbers that matter, all as of mid-2026.

| Detail | FBTC |

|---|---|

| Full name | Fidelity Wise Origin Bitcoin Fund |

| Ticker / exchange | FBTC / Cboe BZX |

| Issuer | Fidelity (FMR) |

| Custodian | Fidelity Digital Asset Services |

| Inception | January 11, 2024 |

| Expense ratio | 0.25% |

| Bitcoin held | ~179,670 BTC |

| Assets under management | ~$11.4B |

How to Buy FBTC in a Brokerage or IRA

Buying FBTC is deliberately boring, and that is the point. You purchase it like any stock or ETF, through a brokerage account, by entering the ticker symbol and placing a buy or sell order during regular market hours. No crypto exchange account, no wallet, no seed phrase to safeguard.

The retirement angle is where FBTC gets genuinely interesting. Because it is a registered security, FBTC can be held in tax-advantaged accounts that cannot touch Bitcoin directly, including many IRAs and other retirement accounts, plus some 401(k) plans. That lets investors get Bitcoin exposure inside an account built for long-term, tax-efficient growth. If you already run a Fidelity IRA, adding FBTC takes a couple of clicks. For a lot of mainstream investors, that accessibility is the entire reason these funds exist.

Risks of FBTC: Volatility and No SIPC

Let me be blunt about the risks, because the marketing rarely is. The first one is obvious: FBTC is Bitcoin, and Bitcoin is brutally volatile. The fund passes every swing straight through to you. As of June 2026, Bitcoin traded near $61,500, roughly half of its October 2025 all-time high above $126,000. An ETF wrapper does nothing to soften that ride. The whole sector feels that gravity: total US spot Bitcoin ETF assets have fallen from a 2025 peak above $169 billion to about $79 billion, dragged down with the price.

The subtler risk gets almost no airtime. SIPC and FDIC insurance, the protections you associate with brokerage and bank accounts, do not cover the Bitcoin inside FBTC against a fall in price, and SIPC does not insure the crypto holdings the way it does cash and securities. If Bitcoin drops, no one reimburses you. There is also custody and operational risk, plus the chance the share price drifts slightly from the fund's true Bitcoin value. None of this makes FBTC a bad product. It makes it a Bitcoin product, with all the risk that implies.

FBTC vs Holding Bitcoin Directly

So why buy FBTC instead of just buying Bitcoin? Convenience and access. You get exposure inside familiar, tax-advantaged accounts, with no keys to lose and no exchange to vet. For many people that is worth a quarter percent a year.

The trade-off is control. You cannot withdraw the actual Bitcoin, send it, or spend it. You only ever hold shares, you pay the fee for as long as you hold, and you can only trade during market hours, not the 24/7 crypto market. The old crypto mantra, not your keys, not your coins, applies in full. FBTC is Bitcoin exposure, not Bitcoin ownership. Which one you want depends on whether you care more about convenience or self-sovereignty.

Structurally, FBTC is organized as a grantor trust, per its SEC prospectus. For tax purposes that generally means you are treated as owning a share of the underlying Bitcoin, which can simplify reporting compared with juggling exchange records. Confirm the specifics with a tax professional, since your situation may differ.

Who Should Consider FBTC as an Investment

FBTC fits investors who want Bitcoin in a familiar wrapper: people building a long-term position inside a brokerage or retirement account, who would rather not manage wallets and exchanges, and who value Fidelity holding the keys in-house. It is a clean on-ramp for traditional portfolios.

It fits less well for anyone who wants to actually use Bitcoin, move it between wallets, spend it, or hold it without paying a recurring fee. Those investors are usually better served owning Bitcoin directly in a wallet they control. The right answer depends entirely on what you want the Bitcoin for, and there is no single correct choice that fits everyone.

FBTC as a Bitcoin Investment: the Verdict

FBTC is a well-built, fairly priced, cleanly custodied way to own Bitcoin through a brokerage, and its in-house custody is a genuine edge in a field that mostly leans on a single third party. The honest takeaway is that the choice between FBTC and IBIT comes down to fees that are identical, platforms that differ, and custody preferences, not to the Bitcoin itself, which is the same asset in both. The harder question is the one only you can answer: do you want exposure to Bitcoin, or do you want Bitcoin? FBTC is firmly the former.