EigenLayer Restaking: EIGEN, EigenCloud, and Risk

Two years ago, EigenLayer was the most hyped idea in crypto. Over $20 billion poured in to "restake" ETH, the promise being that you could take coins already securing Ethereum and rent that same security out to dozens of other apps for extra yield. Then the bill arrived. The EIGEN token is down roughly 97% from its peak, the money locked in the protocol has more than halved, and in April 2026 a $292 million exploit in a connected project showed exactly what the skeptics had been warning about. This is what restaking actually does, how EigenLayer works, and what happened when the risks stopped being theoretical.

What EigenLayer and Restaking Actually Do

EigenLayer is a protocol built on Ethereum that lets staked ETH do double duty. It was created by Sreeram Kannan, a former University of Washington professor, through a company called EigenLabs, and it rolled out on Ethereum mainnet in stages across 2023 and 2024. The core idea has one moving part, and almost every benefit and every danger flows from it.

Restaking: reusing staked ETH

When you stake ETH on Ethereum, your coins help secure the network and earn a yield. Restaking lets you opt in to a second job for those same staked assets. You point your staked ETH, or a liquid staking token that represents it, at EigenLayer's smart contracts, and from there it can also back other services. In return you earn extra rewards on top of normal staking. Nothing is free, though. By agreeing to secure more things, you also agree to be punished if any of them decide you misbehaved. The single coin now carries several promises at once — and that is the whole story in one sentence.

AVSs, operators, and rewards

The "other services" have a name: Actively Validated Services, or AVSs. An AVS is any system that needs its own security but does not want to bootstrap a fresh set of validators and a token from scratch. Instead of begging the market to stake a brand-new coin, it rents security from ETH that is already staked. Bridges, oracles, and data-availability layers were the early customers. Stakers supply the capital, operators run the actual software that does the work for each AVS, and the AVS pays both for the service. The operators are not all anonymous either; infrastructure names like Google Cloud and Coinbase Cloud have run nodes, which tells you the model was taken seriously. EigenDA, a data-availability layer that lets Ethereum rollups post their data cheaply, became the flagship example of an AVS that does something genuinely useful rather than just printing rewards. It is a marketplace for trust, and on paper everyone wins: services launch cheaper, and stakers earn more from capital they already had locked up.

The EIGEN Token and Intersubjective Faults

Most slashing is mechanical. Break a clear on-chain rule and code cuts your stake automatically. But some faults cannot be proven in code, only judged. If an oracle reports a price everyone knows is wrong, no single line of code can prove the intent. EIGEN exists for these "intersubjective" faults. The token can be forked, splitting into a version that keeps misbehaving actors and one that does not, so the honest majority can punish bad behavior the chain cannot settle on its own. In practice EIGEN comes in two forms, a tradeable EIGEN and a staking-focused bEIGEN, to keep that forking risk away from ordinary holders.

That is the theory. The market told a blunter story. Before any token existed, EigenLayer ran a long points program, rewarding people who deposited early with "points" that everyone assumed would convert into an airdrop. It worked almost too well, pulling in billions of dollars of ETH chasing a token that had no price yet. EIGEN finally launched in October 2024, hit an all-time high of $5.65 that December, and has since fallen about 97%. A lot of the capital that arrived for points left once the points turned into a falling token.

| EigenLayer snapshot | Figure |

|---|---|

| EIGEN launch | October 2024 |

| Initial supply | 1.673 billion (45% community / 55% insiders) |

| EIGEN all-time high | $5.65 (December 2024) |

| EIGEN price now | about $0.18 (around $134M market cap) |

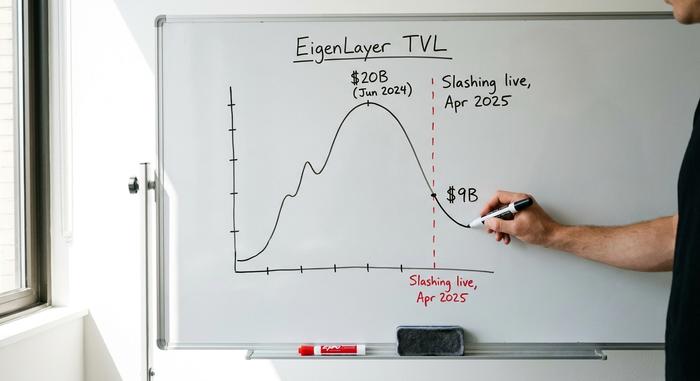

| TVL peak | about $20 billion (June 2024) |

| TVL now | about $9 billion |

When EigenLayer Slashing Went Live

For its first eighteen months, restaking had no teeth. You could earn the extra rewards, but the punishment side, slashing, was not switched on yet. That changed in April 2025, and the timing matters.

How slashing works

Slashing means the protocol can take part of your restaked ETH if you break the rules of an AVS you signed up to secure. The catch is that every AVS writes its own rules. There is no shared standard for what counts as a fault or how harsh the penalty is. One service might cut a few percent for downtime; another could, in theory, take far more. A staker backing several AVSs is exposed to all of their rules at once, and an operator who runs many services can drag the people staking with them into a penalty triggered somewhere else entirely.

The TVL exodus

EigenLayer's slashing went live on April 17, 2025, with 39 services active and roughly $7 billion restaked at the switch. Once the risk became real, a lot of capital decided the extra yield was not worth it. Total value locked, which had peaked near $20 billion in June 2024, slid toward $9 billion. The neat way to describe what happened is that capital fled and builders stayed. The yield farmers who had parked ETH for points and airdrops left once losses became possible, while the teams actually building services mostly remained. The hype number shrank; the working core did not vanish.

Why Restaking Risk Stacks Up Fast

Here is the part the 2024 explainers tended to wave away. The danger in restaking is not one AVS failing. It is that the same ETH is backing many things at once — which is leverage, and leverage cascades.

Rehypothecation and leverage towers

Critics compared restaking to the repackaged debt of 2008 for a reason. The same collateral gets pledged again and again. One ETH becomes a liquid staking token like stETH, that becomes a liquid restaking token like eETH, that gets deposited somewhere to borrow a stablecoin, which buys more ETH. Each layer looks fine on its own. Stacked, they mean a single shock can unwind several positions at once. Even Vitalik Buterin warned against this shape of risk in 2023, arguing that Ethereum's consensus should not be overloaded with extra jobs it was never designed to carry. If one AVS gets its governance compromised and pushes through a malicious slashing rule, thousands of validators could lose stake they never knowingly put at risk.

The Kelp DAO $292 million exploit

The argument stopped being theoretical in April 2026. Kelp DAO, a liquid restaking project built on top of EigenLayer, had a bridge compromised in an attack later attributed to the Lazarus Group. About $292 million was drained, and wrapped ETH tied to the project was left stranded across some twenty chains. The damage did not stay contained. Lending markets including Aave and SparkLend froze related assets to protect themselves, which is contagion working exactly as the skeptics drew it on a whiteboard. The collateral underneath several protocols turned out to be the same collateral, and when it broke in one place, everything touching it had to react.

| Liquid restaking token | Standing |

|---|---|

| ether.fi (eETH) | Largest LRT, about $7.8 billion |

| Renzo (ezETH) | Major LRT by deposits |

| Puffer (pufETH) | Mid-sized LRT |

| Kelp DAO (rsETH) | Exploited for $292M in April 2026 |

From EigenLayer to the EigenCloud Pivot

When restaking growth stalled, EigenLayer's parent company EigenLabs changed the pitch. In mid-2025 it rebranded the wider effort as EigenCloud and redefined AVS from "Actively Validated Services" to "Autonomous Verifiable Services," signaling that the real product was meant to be verifiable cloud-style services, not just yield on staked ETH. The company cut about 25% of its staff in July 2025 to focus on that bet. Money still backed it. The venture firm a16z had put $100 million into EigenLayer in February 2024 and added a $70 million token purchase in June 2025 to support the EigenCloud direction. EigenDA, a data-availability layer that lets rollups post data cheaply, remained the flagship example of what restaked security is actually good for. The reframing is honest in a way: rent-a-security is more useful as plumbing than as a yield machine. The harder question is whether a "verifiable cloud" can win paying customers in a market already owned by Amazon and Google, or whether the pivot is a smaller, sturdier business dressed up as a bigger one. Either way, the message to stakers changed from "earn more" to "secure things that matter," which is a quieter and more defensible promise.

EigenLayer vs Symbiotic and Karak

EigenLayer did win the restaking war. It still holds well over 90% of all restaking value locked, dwarfing its rivals. Symbiotic, the main challenger, sits around $412 million, and Karak takes a smaller slice. The competitors differ mainly in design. Symbiotic is more permissionless about which assets and networks it supports, accepting a wider range of collateral rather than centering on ETH, while EigenLayer started ETH-focused and more curated about what it would secure. Karak pushed a similar restaking pitch with its own twist. None of them changed the basic shape of the trade, which is that rented security is only as safe as the weakest service renting it. But dominance is the lesson here, not safety. Holding the lion's share of the ecosystem did not protect EIGEN's price or stop deposits from leaving. Being the biggest restaking protocol and being a good investment turned out to be two very different things, and anyone who bought the token expecting the first to guarantee the second learned that the hard way.

Is EigenLayer Actually Safe to Use?

It depends on which layer you touch. EigenLayer's own contracts have not been the thing that blew up; the damage has come from the leverage and bridges stacked on top, as Kelp showed. Native restaking, where you restake your own ETH directly and pick AVSs carefully, is the lower-risk path. Liquid restaking tokens, which wrap that exposure and route it through extra protocols, add convenience and risk in the same move. My rule is simple: only restake what you can afford to watch get slashed, and treat any double-digit yield as a warning label, not a feature. If you cannot explain where the extra return comes from, you are the yield.

What EigenLayer's Reset Means for ETH

The core idea behind EigenLayer is sound. Letting new services rent Ethereum's security instead of building their own is genuinely useful, and EigenDA shows it working. The 2024 version simply stacked too much leverage on top of that idea and called the result yield. The reset since then has been brutal on the token and the TVL, but it may leave the survivors built on real demand rather than airdrop farming. The open question is whether AVS revenue ever grows large enough to pay for the risk stakers take on. Until it does, the honest move is to treat restaking as an experiment you can lose money in, not a savings account. Can you actually price the risk you are being paid for? If not, wait.