What Is an ARN Number and How to Track Transactions

A customer emails asking where their refund is. You processed it three days ago. The money left your account, the payment processor confirmed it, but the customer sees nothing. The answer to that impasse is usually four letters: ARN.

An ARN, short for Acquirer Reference Number, is a unique 23-digit code attached to every card transaction once it settles. It works across Visa and Mastercard networks and travels with the transaction as it moves from the merchant's bank to the cardholder's bank. Any party in that chain can use it to pinpoint exactly where a payment or refund stands. For merchants, it's the fastest way to end a "where's my money?" conversation. For customers, it's the only tracking number that actually means something at the bank level.

What Is an Acquirer Reference Number (ARN)?

Think of the Acquirer Reference Number as a tracking code the bank puts on a card transaction — not the merchant, not the customer. It's issued by the acquiring bank, which is the institution holding the merchant's account. Unlike an order ID from your shopping cart or a reference you assign yourself, this one follows the transaction all the way through the payment network.

The ARN is always 23 digits. Those digits aren't random. They encode:

- Bank identification code — identifies the acquiring bank that originated the transaction

- Julian date — the settlement date in day-of-year format

- Processing hour — the hour the batch was settled

- Sequence number — a serial that makes each ARN unique within that batch

One timing detail that trips people up: the ARN only exists after settlement, not after authorization. When a customer's card gets approved at checkout, there's no ARN yet. The code shows up one to two business days later, when the transaction settles. Refunds work the same way — each one gets its own separate ARN, completely distinct from the original purchase.

How Does an ARN Work in Payment Processing?

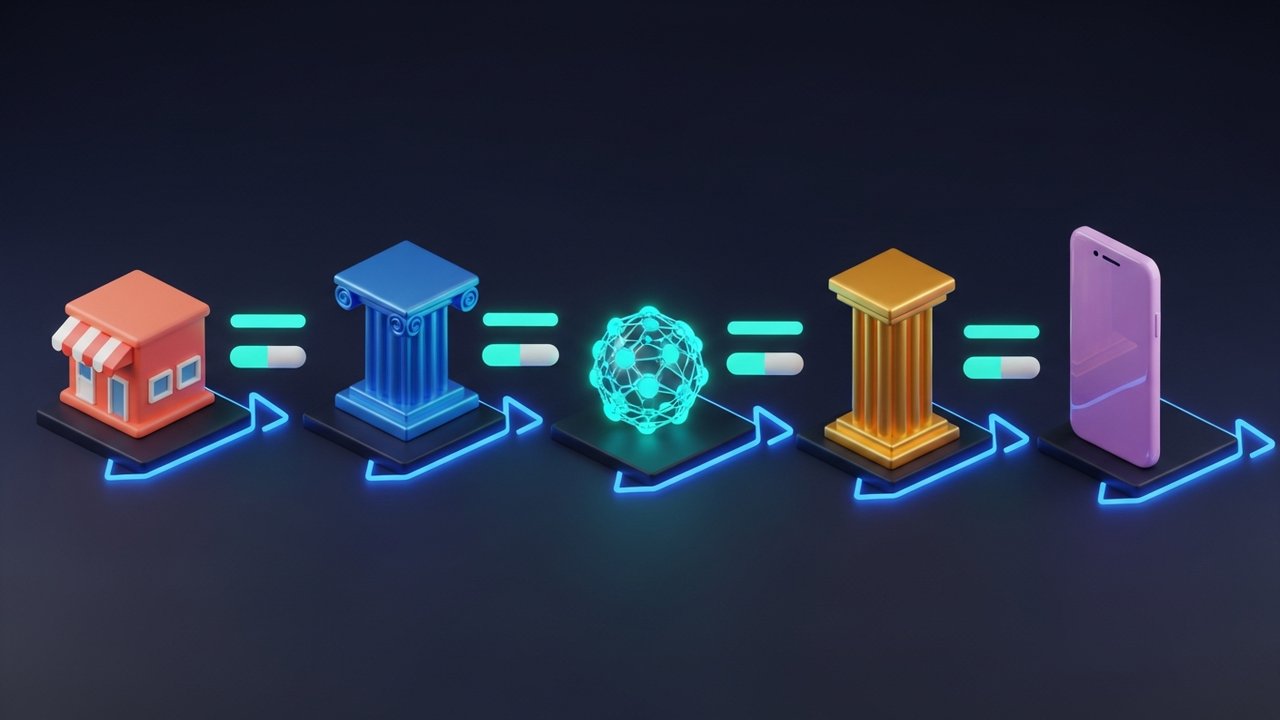

The ARN moves through the payment infrastructure alongside the funds. Here's how that works for a standard card refund:

- Merchant initiates the refund — your payment processor sends a refund request to your acquiring bank.

- Acquiring bank creates the ARN — during the next settlement cycle, the acquirer assigns a unique 23-digit ARN to the refund transaction.

- Transaction routes through the card network — the acquiring bank passes the ARN along with the funds to Visa or Mastercard's network.

- Card network relays it to the issuing bank — the cardholder's bank receives both the funds and the ARN.

- Issuing bank posts the credit — the refund appears in the cardholder's account, and the ARN is logged in the bank's records.

Every party in this chain, including the merchant's processor, the card network, and the issuing bank, can look up a transaction using its ARN. That cross-institutional reach is what makes it the most reliable way to trace a payment across the full system.

What Are ARNs Used For in Payments?

The ARN's main value is traceability. Once a transaction leaves one institution and enters another, internal IDs stop working across boundaries. The ARN doesn't. Three use cases come up most often:

- Refund tracking — a customer reports a missing refund, the merchant provides the ARN, and the customer takes it to their bank. The bank queries the card network and confirms when the funds arrived and whether they've been posted.

- Chargeback disputes — a cardholder files a chargeback claiming they never got a refund. The merchant submits the ARN as proof it was processed and settled. That's often enough to close the dispute without further escalation.

- Fraud investigation — banks and payment processors use ARNs to trace unauthorized transactions, verify that legitimate ones completed, and spot patterns that flag fraud.

ARNs also help with day-to-day reconciliation. Finance teams use them to match settlements to individual transactions in accounting systems. Dispute automation platforms pull ARN data to check real-time refund status and cut down on manual case handling.

Where and How to Find Your ARN Number

Where you find the ARN depends on whether you're the merchant or the cardholder.

For merchants, it typically shows up in one of three places:

- Payment gateway dashboard — in Stripe, go to Payments, select the transaction, and scroll to the Timeline or Details section. In PayPal, open the transaction details and look for the "Acquirer reference number" field. Most major gateways expose it somewhere in the transaction detail view.

- Acquiring bank portal — if your gateway doesn't surface the ARN, log in to your acquiring bank's merchant portal. ARNs are usually visible in settlement reports, searchable by transaction date and amount.

- API response — when using a payment processor API, the ARN often comes back in the transaction object after settlement. Common field names include arn, acquirer_reference_number, and network_reference_id, depending on the provider.

Not every payment processor shows the ARN in their standard UI. This is a known frustration. If it's not visible in your dashboard, contact your acquirer's support team directly. They can pull it from settlement records using your internal transaction ID, date, and amount.

For cardholders, the process runs through the merchant:

- Contact the merchant and ask for the ARN on your refund transaction.

- Once you have it, call your card-issuing bank's customer service and give them the 23-digit code.

- Ask them to trace the refund using the ARN. They'll check with Visa or Mastercard and report back.

Cardholders cannot query an ARN on the Visa or Mastercard website. That access is reserved for member financial institutions. Your bank is the only way in.

How to Track a Refund with an ARN Number

If a refund isn't showing up, here's the step-by-step process:

- Get the ARN from the merchant. Ask them to locate it for the specific refund. It should be in their gateway dashboard or acquiring bank records.

- Contact your card-issuing bank. Call the number on the back of your card or use live chat. Ask to speak with the payments or disputes team.

- Provide the full 23-digit ARN. Read it out or paste it in. Ask the agent to trace the transaction using the ARN.

- Wait for the bank to query the card network. Visa and Mastercard have internal refund status tools that only banks can access. Expect a response in one to three business days.

- Review the status. You'll get one of three results: in transit (funds left the acquirer but haven't posted), posted (funds arrived at the issuing bank), or not found (see the troubleshooting section below).

A few timing things to keep in mind before you start: the ARN itself won't exist until one to two business days after the refund is initiated. That's just how settlement cycles work. From there, give the credit up to 10 business days to actually appear in the customer's account. Most refunds land faster — three to five days is more typical. The 10-day mark is the hard outer limit under card network rules, not the expected timeline.

ARN vs Other Transaction Identifiers

The payment ecosystem runs on several different reference numbers, and they're easy to mix up. Each one has a specific scope:

| Identifier | Full Name | Assigned By | When | Purpose |

|---|---|---|---|---|

| ARN | Acquirer Reference Number | Acquiring bank | At settlement | Cross-network tracing, refund tracking |

| STAN | System Trace Audit Number | Payment terminal | At authorization | Internal routing within a bank or processor |

| RRN | Retrieval Reference Number | Issuing bank | At authorization | Bank-side lookup for the issuer |

| Order ID | — | Merchant | At checkout | Internal e-commerce reference, no network access |

The core difference is scope. An order ID only works inside your platform. A STAN or RRN is recognized within a single institution. The ARN travels the full length of the payment chain, from acquirer to card network to issuer. That makes it the only identifier that can definitively confirm a transaction or refund actually reached its destination.

Benefits of ARN for Merchants and Customers

The ARN isn't just a technical record. It has real business value on both sides of a transaction.

For merchants:

- Faster dispute resolution — presenting an ARN in a chargeback response immediately shifts the question from "did you refund it?" to "when did the funds arrive?" That's a much stronger position.

- Reduced chargeback losses — documented proof that a refund was processed and assigned an ARN often closes the dispute before it escalates.

- Better customer experience — giving a customer an ARN instead of "please wait 5–10 business days" signals transparency and builds trust.

- Cleaner reconciliation — ARNs connect your internal transaction IDs to network-level settlement data, which simplifies month-end reconciliation.

For customers:

- Certainty over waiting — an ARN tells you the refund actually left the merchant's bank. You're not guessing.

- A real escalation tool — if your bank pushes back, the ARN is your evidence. Not "I think the merchant refunded me," but a traceable code that proves it.

- Shorter resolution timelines — banks act faster with an ARN to query than when investigating a vague missing refund claim.

If reducing payment friction altogether is the goal, Plisio gives merchants instant settlement confirmation and clean transaction records, cutting down the scenarios where ARN tracing becomes necessary.

Common ARN Issues and How to Resolve Them

Even when things go right, ARN-related problems still surface. Here are the most frequent ones:

- ARN isn't available yet — it only exists after the refund settles, which takes one to two business days after processing. Wait 48 hours before following up.

- Bank doesn't recognize the ARN — most common at smaller regional banks without deep integration into Visa or Mastercard tracing tools. Escalate to the fraud or disputes team; they're more likely to have the right access.

- ARN shows "processed" but funds haven't arrived — the acquirer sent the money and the card network accepted it, but the issuing bank hasn't posted it yet. This is a posting delay. Give the issuing bank up to five business days.

- Merchant can't provide the ARN — not all payment service providers surface ARNs in their merchant dashboard. If your PSP doesn't show it, ask them to pull it from the acquirer. Every settled transaction has one; it just isn't always visible in the UI.

- ARN appears truncated — Visa ARNs are always 23 digits. If you receive something shorter, it's a partial display from the gateway. Get the full number from the acquiring bank before trying to trace it.