Merchant Acquiring: Acquirers, Issuers, and Payment Processors Explained

Every time a customer pays by card, a chain of financial institutions fires into motion. The one that actually makes the merchant capable of accepting that payment is the merchant acquirer. Merchant acquiring is the infrastructure sitting behind every card transaction, whether the sale happens in a shop, on an e-commerce checkout, or through an app. For any business owner picking payment infrastructure, negotiating fees, or comparing alternatives, knowing how it works is worth the five minutes it takes.

What Is Merchant Acquiring

Put simply, merchant acquiring is what stands between a business and its ability to take card payments. A bank or licensed financial institution provides the service. That institution is the merchant acquirer, sometimes called the acquiring bank.

The acquiring bank isn't passive. It holds the merchant account, which is the holding account where card payment proceeds land before the business can actually use the money. It also registers the business with card networks — Visa, Mastercard — and takes on financial responsibility for whatever happens with the merchant's transactions. That includes chargebacks and fraud losses.

Which is why this isn't just a technical arrangement. Before any merchant acquirer accepts a new client, it underwrites the business. It checks transaction volumes, what industry the business is in, chargeback history, financial health. Gambling platforms, travel companies, and subscription businesses tend to get tougher scrutiny and end up paying more. The acquirer is taking on risk, so it prices accordingly.

How the Merchant Acquiring Process Works

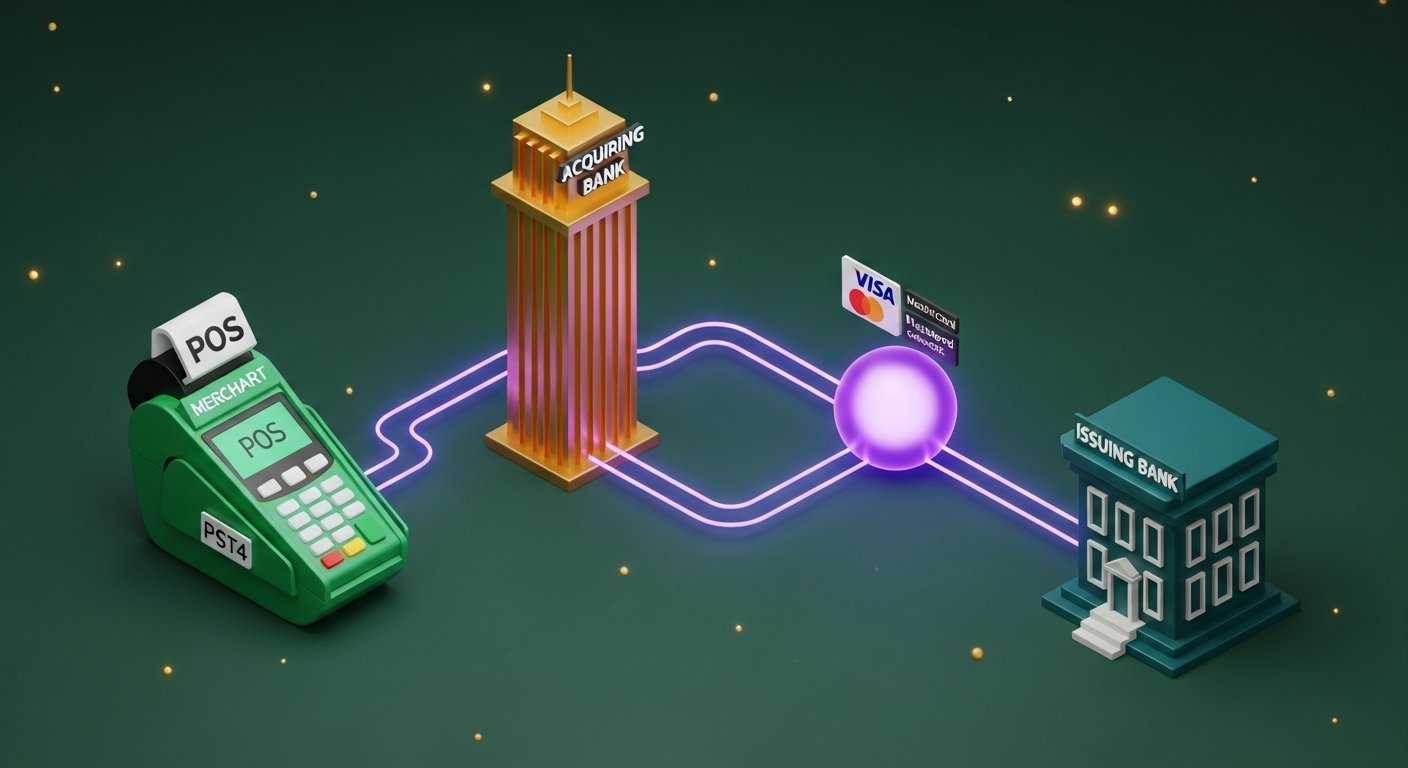

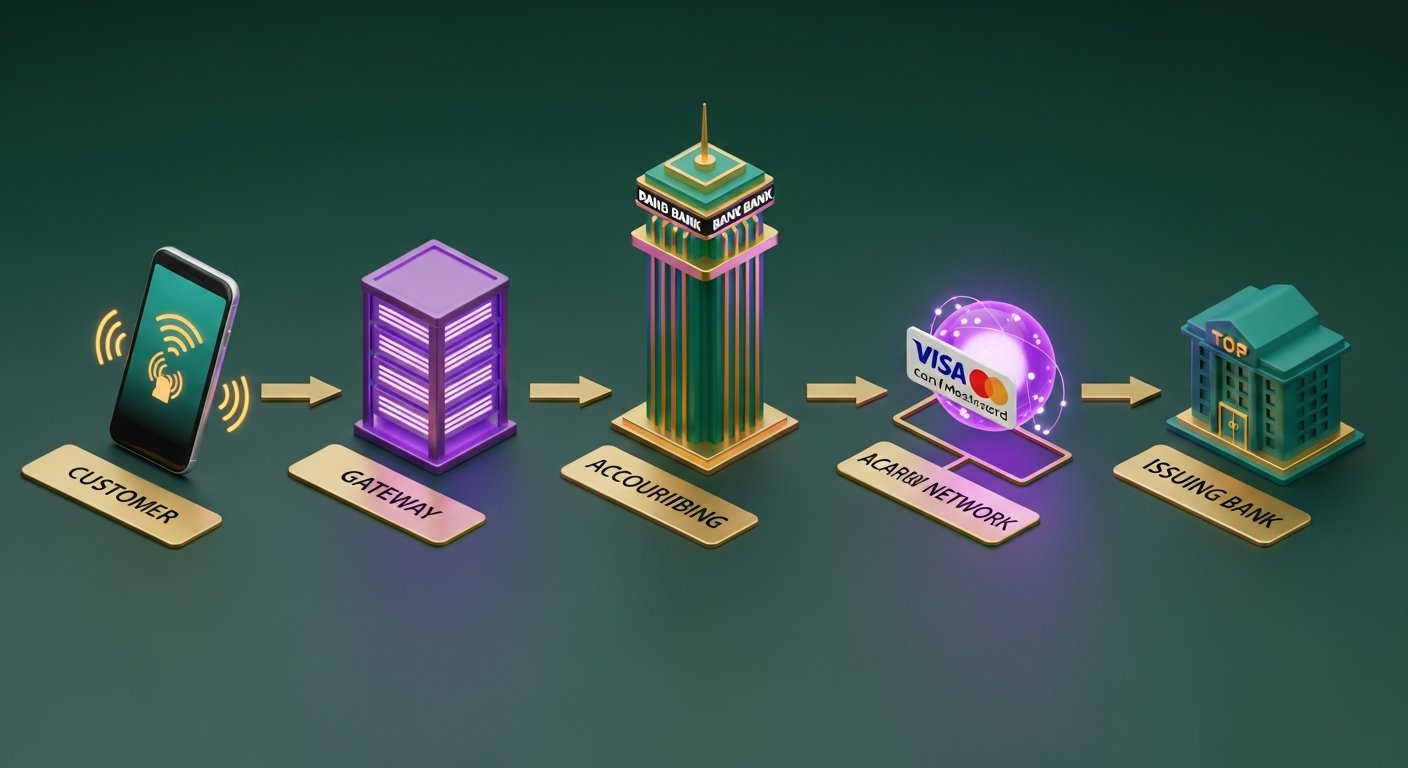

A card payment looks instant from the buyer's end. Behind the screen, five steps happen in roughly two seconds.

- Customer initiates payment — taps a card, inserts a chip, or types card details online. The terminal or payment gateway captures the data.

- Gateway sends data to the acquiring bank — the payment gateway encrypts the transaction details and routes them to the merchant's acquiring bank. This goes through the acquirer's own gateway or a third-party one.

- Acquirer routes to the card network — the acquiring bank forwards the transaction to the relevant card network: Visa, Mastercard, or Amex. The card network identifies the issuing bank — the one that issued the customer's card.

- Issuing bank authorises or declines — the card network passes the request to the issuing bank, which checks funds, fraud signals, and card status. An approval or decline travels back through the same chain in 1–3 seconds.

- Clearing and settlement follow — once authorised, the transaction enters clearing, where the acquirer and issuing bank reconcile the details. Settlement moves the actual funds. That part usually takes 1–3 business days, though some acquirers now offer T+1 or same-day options.

The merchant gets an approval code. The customer gets a receipt. Done.

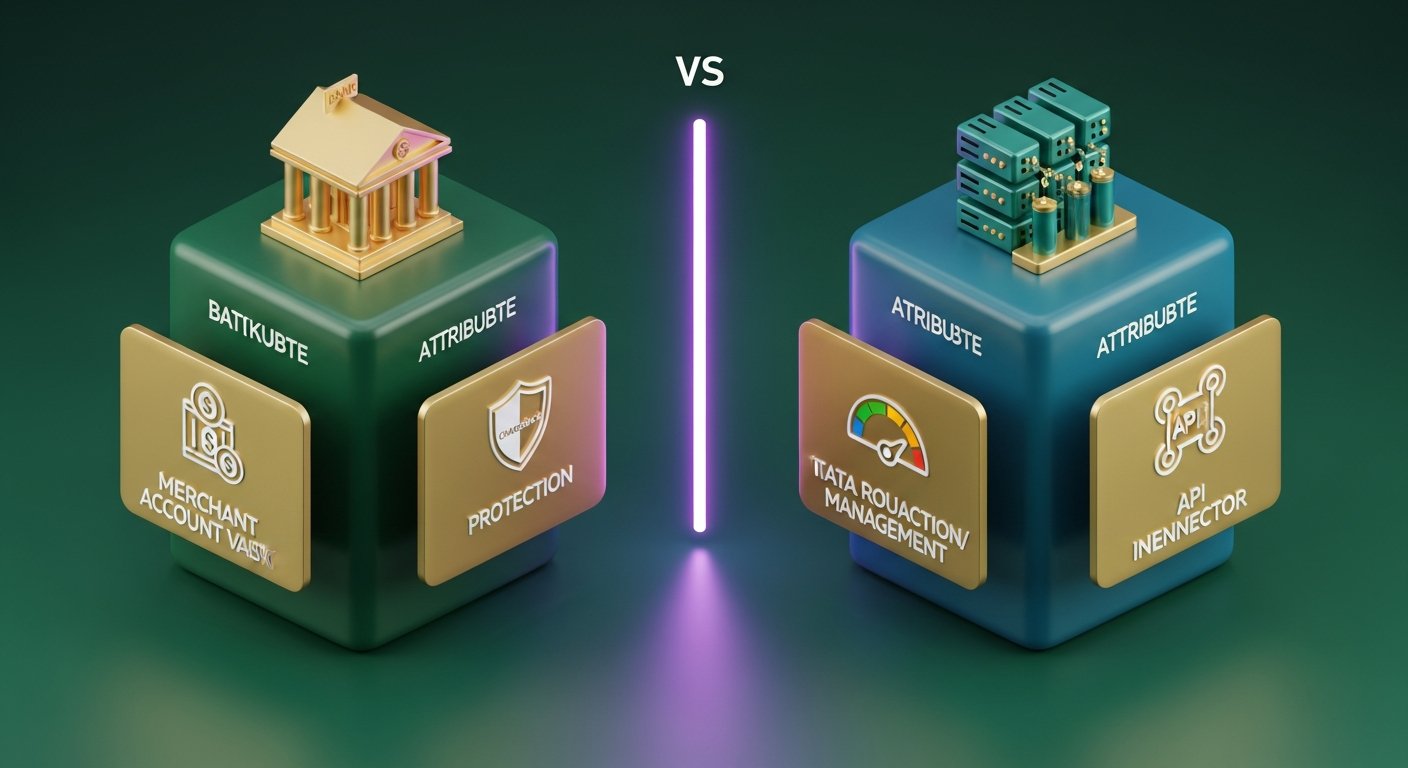

Merchant Acquirer vs Payment Processor: Key Differences

"Merchant acquirer" and "payment processor" get used interchangeably, but they're not the same thing. The confusion is understandable since many providers now handle both, but the distinction matters when you're reading a contract or working out your actual cost per transaction.

| Merchant Acquirer | Payment Processor | |

|---|---|---|

| Core role | Holds merchant account, assumes financial risk | Routes transaction data between parties |

| Regulatory requirement | Requires banking license or card network membership | Lower regulatory threshold — no banking license needed |

| Relationship to merchant | Holds funds, sets acceptance terms, underwrites risk | Handles transaction technology and data transfer |

| Risk exposure | Chargebacks, fraud, merchant insolvency | Minimal direct financial risk |

| Examples | Barclaycard, Worldpay, Lloyds Cardnet | Stripe (as processor), Braintree, Adyen (as processor) |

In practice, the payment processor sits between the payment gateway and the acquiring bank, handling the technical routing of card data. The acquirer holds the money and the relationship.

Payment service providers like Stripe, Adyen, Checkout.com, and Square act as both processor and acquirer. They put merchants under their own acquiring license, which is why onboarding with them takes minutes instead of the weeks a direct acquiring relationship typically requires.

Acquiring Bank vs Issuing Bank: What's the Difference

Every card transaction touches two banks. Most people know one of them — they just don't realise it.

The acquiring bank is the merchant's bank. After a transaction settles, it receives the card payment proceeds from the card network and deposits them into the merchant account.

The issuing bank is the cardholder's bank — the institution that issued the Visa or Mastercard the customer swiped. When a payment request comes through, the issuing bank decides whether to approve or decline it based on available funds, fraud scoring, and card status.

| Acquiring Bank | Issuing Bank | |

|---|---|---|

| Whose bank is it? | The merchant's | The cardholder's |

| Role in a transaction | Receives and holds payment proceeds | Approves or declines the transaction |

| Who bears chargeback risk? | Acquirer (initially) | Issuer enforces chargeback rules |

| Examples | Barclaycard, Worldpay, Chase Merchant Services | HSBC, Lloyds, Monzo, Chase (as card issuer) |

Both banks are registered card network members. That shared membership is what allows them to exchange data and funds in real time across millions of transactions daily.

What Services Does a Merchant Acquirer Provide

Acquirers do more than park a merchant account. A standard acquiring relationship covers:

- Merchant account setup and management — the dedicated account receiving card payment proceeds

- Payment gateway access — either the acquirer's own gateway or integration support for third-party ones

- Fraud monitoring — real-time risk scoring to catch suspicious transactions before they clear

- Chargeback handling and dispute management — running the process when a cardholder disputes a charge with their issuing bank

- PCI DSS compliance guidance — helping merchants meet Payment Card Industry Data Security Standard requirements

- Settlement and reconciliation reporting — daily or weekly breakdowns of transactions, fees, and net payouts

- Multi-currency and international acquiring — taking card payments in multiple currencies across different markets

- Currency conversion — dynamic currency conversion (DCC) for international cardholders who want to pay in their home currency

Chargeback management quality varies a lot between acquirers. For businesses operating in higher-risk categories, it's often the thing that tips the decision.

Merchant Acquiring Fees and Pricing Models

Merchant acquiring fees come in three layers, even when your statement shows a single percentage.

| Fee Component | What It Is | Who Gets It | Typical Range |

|---|---|---|---|

| Interchange fee | Core transaction cost, set by card networks | Issuing bank | 0.2%–2%+ per transaction |

| Scheme fee | Network access fee | Visa / Mastercard | 0.1%–0.3% |

| Acquirer margin | The acquiring bank's profit on the transaction | Acquiring bank | 0.1%–0.5% |

| Blended rate | All three combined into one rate | Merchant pays all | 1.5%–3.5% |

Most small merchants get a blended rate: one flat percentage that bundles interchange, scheme fees, and the acquirer's cut together. Simple to budget, but opaque. You can't tell how much of that 2.5% is flowing to the issuing bank versus staying with your acquirer.

Bigger merchants negotiate interchange++ pricing (cost-plus). The actual interchange and scheme fees pass through at cost, with a fixed acquirer margin added on top. Harder to reconcile, but significantly cheaper at volume. It also surfaces something blended pricing hides: when a customer pays with a premium rewards card, the interchange rate on that card is higher than a standard debit card.

Other fees to watch: monthly fees, minimum monthly charges, PCI non-compliance fees, and chargeback fees running around £10–£25 per disputed transaction. Those are where acquirers quietly recover margin on smaller accounts.

How to Choose the Right Merchant Acquirer

Not every acquirer fits every business. Seven things worth checking:

- Geographic coverage — does the acquirer directly acquire in the countries your customers are in? Direct acquiring in a market costs less and settles faster than cross-border.

- Supported payment methods — Visa and Mastercard are table stakes. Check for Amex, JCB, local options like iDEAL or Bancontact, digital wallets (Apple Pay, Google Pay), and BNPL.

- Pricing model transparency — blended rates are predictable; interchange++ saves money at volume. Ask for a full fee schedule before committing to anything.

- Settlement speed — T+1 matters for cash flow. Some acquirers default to T+2 or T+3, which adds unnecessary lag.

- Chargeback management tools — representment support, early warning systems (Visa RDR, Mastercard CDRN), and pre-chargeback alerts reduce dispute losses meaningfully.

- Contract terms — long-term lock-in (12–36 months with early termination fees) is common. Rolling monthly contracts give you more room to move.

- Integration options — REST API, hosted payment page, POS terminal support, and plugin availability for WooCommerce and Shopify.

PCI DSS Compliance in Merchant Acquiring

PCI DSS is the Payment Card Industry Data Security Standard, a mandatory security framework for any business or financial institution that touches card data. Your acquiring bank enforces compliance, and ignoring it comes with real costs.

Four compliance levels exist, based on annual transaction volume:

- Level 1 — more than 6 million card transactions per year. Annual on-site audit by a Qualified Security Assessor (QSA).

- Level 2 — 1–6 million transactions. Annual self-assessment questionnaire (SAQ) plus quarterly network scans.

- Level 3 — 20,000–1 million e-commerce transactions. SAQ and quarterly scans.

- Level 4 — fewer than 20,000 e-commerce transactions. Simplified SAQ and quarterly scans.

Most small online businesses sit at Level 4. Use a hosted payment page or a PSP like Stripe that handles card data on its own servers, and your PCI scope shrinks considerably — you're not storing or transmitting raw card data.

Non-compliance consequences: card network fines passed through by your acquirer (typically $5,000–$100,000 per month), higher transaction fees, and eventually losing the right to accept card payments at all. Acquirers enforce compliance hard because a breach on a merchant's system lands on their books.

Crypto Payments as an Alternative to Merchant Acquiring

Getting set up with a traditional merchant acquirer takes time and comes with strings: a banking relationship, an underwriting process, interchange fees on every transaction, chargeback liability, PCI DSS obligations. For businesses selling across borders, currency conversion charges pile on top.

Crypto sidesteps the acquirer entirely. There's no bank in the middle, no card network, no interchange. And because blockchain transactions are irreversible, there are no chargebacks — which is a meaningful shift for merchants in high-risk industries or those with customers scattered across multiple countries.

Money moves directly from buyer to seller. No one holds it overnight. Fees don't change based on where the customer lives or what currency their wallet is in. For a business where cross-border card fees are quietly shaving margins, that adds up.

Getting a cryptocurrency payment gateway running takes a fraction of the time a direct acquiring relationship does. If you're weighing the option seriously, reading up on the benefits of a crypto payment gateway — no chargebacks, lower cost per transaction, faster settlement internationally — gives you a useful baseline for comparison.

On the question of which provider, choosing a crypto payment gateway with multi-asset support, automatic fiat conversion, and a clean API is what most developers and merchants end up optimising for.

Plisio handles Bitcoin, Ethereum, Litecoin, USDT, and more than a dozen other assets at 0.5% flat. No merchant KYC, no monthly fees, and chargeback risk is structurally impossible.

Conclusion

Merchant acquiring is the financial layer that makes card payments work. The acquiring bank holds the merchant account, absorbs the risk of chargebacks and fraud, and moves funds to the business after each transaction settles. Knowing where the merchant acquirer fits — separate from the payment processor, on the opposite side from the issuing bank, accountable to card networks like Visa and Mastercard — gives any business owner a clearer read on their costs and options.

For most businesses, merchant acquiring is the right model for domestic card acceptance. It gets heavier for international payments, high-risk categories, and anyone who wants to eliminate chargeback exposure. Crypto payments won't replace acquiring in every situation, but for the right merchant they offer a genuinely simpler path to accepting payments globally.