Figma Stock (FIG): Buy Figma After the 84% Crash?

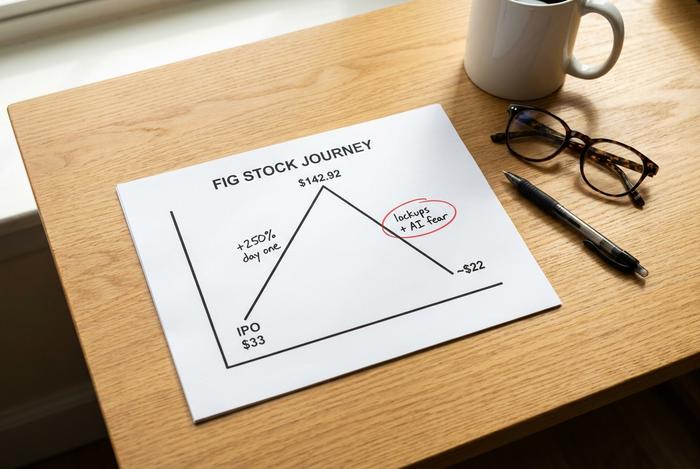

Figma priced its IPO at $33 a share, watched the stock open to a 250% pop and close its first day at $115.50, then ride all the way to $142.92. Less than a year later, Figma stock trades around $22, below the price it sold at on day one. The hottest software IPO of 2025 turned into one of the market's sharpest lessons, and the reason comes down to a single fear: artificial intelligence. This is a clear-eyed look at whether FIG is worth buying now, and that question hinges almost entirely on whether the AI fear that gutted the stock is actually justified.

Spoiler: the business and the share price are telling two completely different stories.

What Figma does and where FIG stock stands

If you have designed an app or a website in the last few years, you have probably touched Figma. It is the browser-based canvas where designers, engineers, and product managers build interfaces side by side, in real time, without emailing files back and forth. Dylan Field co-founded it and still runs it. The company got big enough that Adobe agreed to buy it for $20 billion in 2022, then watched the deal fall apart in 2023 when European and UK regulators dug in. So Figma went public on its own instead, listing on the NYSE as FIG. Its market cap today sits near $11.9 billion. That is a long way below what Adobe offered, and a long way below what FIG stock fetched on its first wild afternoon of trading.

The Figma IPO and FIG stock price crash

The crash looks terrifying on a chart and far less so once you understand what drove it. This was mostly mechanics and mood, not a business falling apart.

Figma went public on July 31, 2025, pricing shares at $33 and raising about $1.22 billion. Demand was frantic. The stock opened far above its IPO price and closed the first day at $115.50, a 250% pop that briefly handed the company a fully diluted valuation near $47.9 billion. The next day it touched an all-time high of $142.92. For a few weeks Figma was the proof that software IPOs were back.

Then gravity arrived. The stock slid for months, bottomed near $16.60, and now sits around $22.58, roughly 84% below its peak and beneath the $33 it first sold for. Two forces did the damage. The first was supply: early investors and employees were locked up at the IPO, and as those lockups expired through 2026, a wave of new shares hit the market just as enthusiasm cooled. The second was the AI scare, which turned a richly priced growth stock into a target. None of that euphoria was the company's fault; an IPO that pops 250% has simply been priced for a perfection no business can deliver on schedule.

| Date | Event | Share price |

|---|---|---|

| Jul 31, 2025 | IPO priced | $33.00 |

| Jul 31, 2025 | First-day close | $115.50 |

| Aug 1, 2025 | All-time high | $142.92 |

| 2026 | 52-week low | $16.60 |

| May 28, 2026 | Recent price | ~$22.58 |

It is worth being precise about what actually changed, because almost nothing about the company did. Figma did not miss a quarter on the way down. It did not lose a flagship customer or watch growth collapse. What changed was the float and the narrative. More shares became available to trade exactly as the AI worry took hold, and a stock priced for a flawless future got repriced for a frightening one. That gap between story and substance is precisely where opportunity tends to hide, though it is also where value traps live, so the rest of this matters.

The lesson is old and keeps repeating: a great company and a great stock are not the same thing at every price.

Can Figma stock survive the AI design threat?

This is the whole ballgame, so let me put both sides honestly. The bear case is real. The bull case is winning so far.

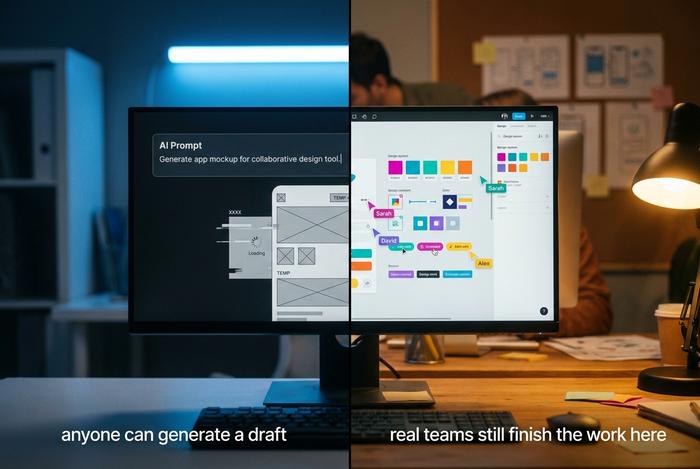

The bears argue that AI eats Figma from below. A new class of AI app builders, tools like Lovable, Vercel's v0, and Cursor, lets someone type a prompt and get a working app or website without ever opening a design canvas. If anyone can generate a usable interface in seconds, the worry goes, why pay for a specialist design tool at all? When the market decided that story was true, it sold FIG down to a fraction of its peak.

Here is what that thesis misses. Figma is not standing still while AI happens to it; it is shipping AI of its own and charging for it. Its AI-powered features, led by Figma Make, turn a prompt into an editable first draft inside the tool you already use. The adoption is not theoretical. Roughly 60% of Figma's customers spending over $100,000 a year now use Figma Make every week, and when those customers blew past their usage credit limits, about 95% of them kept right on using it. That is real AI monetization, the behavior of a feature people need, not a gimmick they try once.

There is also a quieter point the doomers skip. Generating a rough draft is the easy 20%. When a real team has to refine the details, collaborate across functions, manage permissions and design systems, and hand finished work to engineers, the platform they still open is Figma. Even Google, often named as a company that could build a Figma killer, shows up as a customer use case on Figma's own earnings calls.

History rhymes here too. When new tools made it easier for anyone to publish, to build a website, to edit video, the incumbents that owned the professional workflow mostly grew rather than vanished, because more creation meant more work that needed refining, managing, and shipping. AI lowering the barrier to a first draft could expand the number of people who design, and Figma sits at the exact point where rough ideas become finished products. My read is blunt: the market priced Figma as an AI casualty, and so far the numbers say it is an AI beneficiary. That can change, but it has to actually show up in the financials first, and right now it has not.

Figma financials: revenue growth and losses

Strip out the share-price drama and look at what the business actually did, because the crash in Figma stock ignored most of it.

Growth is not just holding. It is speeding up. Figma closed fiscal 2025 at $1.056 billion in revenue, up 41%, then opened 2026 with a $333.4 million first quarter, up 46%. Read those two numbers in order: the company is growing faster now, at a bigger size, than it was a year ago. Net dollar retention reached 139%, its best in over two years, which is a fancy way of saying existing customers keep spending more. Paid customers climbed to roughly 690,000, up 54%. And this is no cash-incinerating startup. Free cash flow came in at $242.7 million last year, a 23% margin, with non-GAAP operating income of $129.5 million.

| Metric | Figure (latest) |

|---|---|

| FY2025 revenue | $1.056B (+41%) |

| Q1 2026 revenue | $333.4M (+46%) |

| Net dollar retention | 139% |

| Paid customers | ~690,000 (+54%) |

| FY2025 free cash flow | $242.7M (23% margin) |

| FY2025 GAAP net loss | $1.25B (mostly stock comp) |

About that scary $1.25 billion net loss: it is almost entirely stock-based compensation tied to the IPO, an accounting charge, not cash going out the door. On a cash basis Figma is profitable. That distinction is the single most misunderstood number in the whole story. Management also nudged full-year guidance higher after the strong first quarter, which is not what a company under genuine AI assault usually does. A business losing to disruption sees retention slip and deals shrink; Figma is seeing the opposite, with customers spending more and expanding onto new products.

FIG stock valuation after the reset

A year ago Figma was priced for flawless execution. After the crash, the math looks very different, and that is the heart of the bull case.

At a market cap near $11.9 billion, FIG stock trades at roughly 8.5 times forward sales. Comparable SaaS companies growing far slower trade closer to 13 times, so the post-IPO reset has left Figma cheaper than its peers despite faster growth. In other words, the market is now paying less for Figma's 46% growth than it pays for the average software name. There is no meaningful price-to-earnings ratio yet because the company is unprofitable on a GAAP basis, and the forward P/E screens absurdly high at around 82, but for a software business growing this fast, sales multiples and cash flow tell the truer story. The valuation reset did not just lower the price; it lowered the bar the company has to clear. When a stock is priced for perfection, even great results disappoint. When it is priced for failure, merely doing fine can send it higher. Figma has shifted from the first camp toward the second, and that change in expectations is often worth more to future returns than any single quarter of revenue.

Analyst ratings, targets, and FIG forecast

Wall Street cannot make up its mind on FIG stock, and that hesitation tells you something.

The consensus rating is a Hold. Not a cheer, not an alarm. Yet analyst price targets average around $36.88 over 12 months, about 63% above where the stock trades now, a forecast that assumes steady execution rather than a nasty AI surprise. Look at the individual calls and you can watch the argument happen: Morgan Stanley is Equal-Weight at $38, JPMorgan leans bullish at $42, Piper Sandler is Overweight at $30. When a cautious consensus still points to big upside, it usually means the analysts believe the business but cannot yet call the mood.

| Firm | Rating | Price target |

|---|---|---|

| Consensus | Hold | ~$36.88 |

| Morgan Stanley | Equal-Weight | $38 |

| JPMorgan | (bullish) | $42 |

| Piper Sandler | Overweight | $30 |

Beyond Figma Design: Make, Sites, and more

The quote pages tracking Figma stock miss the actual growth engine: Figma stopped being one app a while ago. It is becoming a suite, and every new surface makes the platform harder to leave.

The flagship is still Figma Design, but around it the company has built Dev Mode for the handoff from designers to developers, FigJam for whiteboarding, Figma Slides for presentations, Figma Draw for illustration, Figma Sites for publishing live websites, Figma Buzz for on-brand marketing assets, and Figma Make for AI generation. Each addition is a piece of product development aimed at the same goal: pull more of a team's work onto one platform. That is how a software company widens its moat and lifts net retention at the same time, and it is the clearest structural answer to the fear that a single AI tool could replace it.

How to buy Figma stock the smart way

Buying FIG is simple; sizing it is the part that matters. Open a brokerage account, search the ticker FIG on the New York Stock Exchange, and decide whether you want the single name or broader exposure through a software fund that holds it. Because this stock can move violently, treat it as a high-beta growth position, not a core holding. Keep an eye on the remaining lockup overhang running into the second half of 2026, which can add selling pressure on any given week. And rather than chasing a single price, average in over time so a volatile stock quote does not dictate your emotions.

The verdict on Figma stock right now

Figma is that rare case where the business is accelerating while the stock has been left for dead. The AI threat is the genuine risk, and anyone buying has to accept it could still play out badly. But the early evidence, reaccelerating growth, 139% retention, and real money flowing into Figma Make, says the company is monetizing AI rather than being erased by it. At a below-peer valuation with a lockup overhang still clearing, FIG is a high-conviction name to watch and a reasonable nibble for risk-tolerant investors. It is not a sure thing, and the next two earnings calls, starting with the Q2 report, will tell you far more than today's Figma stock price does.