How Crypto Platforms Are Shaping the Future of Finance

A payment company most people have never heard of just became part of how artificial-intelligence agents will pay each other. Bridge, a stablecoin infrastructure startup, was bought by Stripe in early 2025 for $1.1 billion. By the autumn of that year, the same rails were carrying the first live transactions from AI agents on Amazon's Bedrock platform, in cooperation with Coinbase and Visa. None of this is what most people mean when they talk about how crypto platforms are shaping the future. The story is no longer about price predictions, ETF tickers, or whether a particular token survives the next cycle. It is about the quiet rebuilding of the world's payment plumbing, and about who operates the new pipes.

The Rails Crypto Platforms Run Are the Story

A useful way to read the past two years is to separate the coins from the rails they move on. The coins still get the attention; the rails are where the real money has shifted. Real-economy stablecoin payment volume reached $390 billion in 2025, according to a McKinsey analysis published in February 2026 using Artemis Analytics data. Asia accounted for $245 billion of that figure — about 63 percent — driven by Singapore, Hong Kong, and Japan. Business-to-business flows alone made up roughly $226 billion of the total. These are not speculative trades. They are invoices, payroll, supplier settlements, and treasury transfers that used to leave the cross-border financial system through SWIFT and the correspondent-banking network.

The Boston Consulting Group's 23rd annual Global Payments Report, published in September 2025, put the scale of the shift more sharply. B2B stablecoin flows grew from under $100 million a month in early 2023 to more than $6 billion a month by mid-2025, a sixtyfold increase in thirty months — and the trajectory has stayed roughly linear since. I keep coming back to that number. Almost no other category in payments moves that fast.

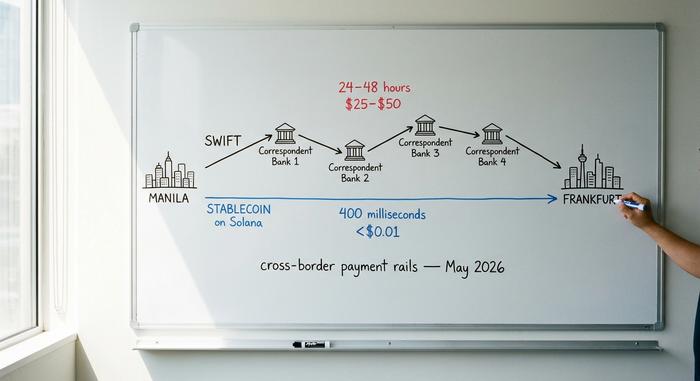

The reason is the unit economics. A typical SWIFT cross-border wire costs $25 to $50 and clears in one to two days. The same value on Solana settles in roughly 400 milliseconds for less than a penny. On Ethereum's mainnet, twelve seconds and a dollar or so. For a finance team moving a multimillion-dollar invoice between Manila and Frankfurt, the all-in cost falls from one to five percent to closer to one or two tenths of a percent. The Bank for International Settlements' Committee on Payments and Market Infrastructures has been documenting this gap for years.

| Settlement layer | Typical fee | Time to finality | Operating hours | FX overhead | Settlement risk |

|---|---|---|---|---|---|

| SWIFT correspondent banking | $25–$50 per wire | 24–48 hours | Business hours, weekdays | 1–3% spread, often hidden | Counterparty across each hop |

| Card networks (Visa/Mastercard) | 1.5–3.5% of the transaction | 1–3 business days to merchant | 24/7 authorisation, batched settlement | Built into FX margin | Issuer + acquirer + scheme |

| Stablecoin on public blockchain | $0.01–$1.00 per transfer | 0.4–12 seconds | 24/7, all year | Spot conversion, near zero | On-chain finality, no recall |

| Tokenised commercial bank deposits | Pilot pricing | Seconds to minutes | 24/7 in pilot | Bank FX rate | Issuing bank |

None of this means SWIFT is going away. It means the marginal new dollar of cross-border B2B payments is no longer flowing through it. The platforms that operate the new rails (Coinbase, Circle, Stripe, Visa's on-chain settlement layer, and a long tail of merchant gateways such as Plisio, BitPay, and NOWPayments) are the ones writing the rules for how value moves in the next decade. The digital asset classes traded on top of those rails are almost a secondary question.

Why Stablecoins Quietly Won the Payments Argument

Stablecoins were the controversial cousin of crypto in 2022. By 2026 they are a boring infrastructure choice that institutional treasury teams understand. Total stablecoin market value sits at around $320 billion as of May 2026, per DeFiLlama. USDT leads at roughly $190 billion, USDC at $78 billion. PayPal's PYUSD has reached $4.1 billion, a 680 percent jump from January 2025. These are not exotic instruments any more.

The institutional plumbing tells the same story. Visa has settled more than $225 million on-chain across four blockchains using USDC, PYUSD, USDG, and EURC; its stablecoin-linked card programme with Bridge expanded to more than 100 countries during 2026. Visa's stablecoin-linked card spending hit a $3.5 billion annualised run rate by the end of fiscal 2025, up 460 percent year on year. That is nearly a fifth of all crypto-card settlement on the network, per Artemis Analytics. Mastercard, on the same timeline, switched on USDG, PYUSD, USDC, and FIUSD support across its global network. Stripe followed its Bridge acquisition with Open Issuance in September 2025, a platform that lets any business launch its own stablecoin with a few lines of code. Patrick Collison, Stripe's chief executive, has described stablecoins as "room-temperature superconductors for financial services."

Beyond payments, the same rails carry a growing pool of tokenised cash equivalents. BlackRock's BUIDL tokenised money-market fund reached $2.5 billion in assets in November 2025 after a tie-up with Binance. Franklin Templeton's on-chain FOBXX fund is in the $650 million range. The broader market of tokenised real-world assets, excluding stablecoins themselves, passed $32 billion in May 2026 according to RWA.xyz. A finance team that wants 24/7 access to yield on idle cash now has an on-chain option that did not exist three years ago.

The argument that stablecoins are too risky or too unregulated to use at scale has been overtaken by what banks and card networks have actually built around them. It does not mean the risks have disappeared. It means the operators now have liability frameworks, attestation reports, and regulatory cover. The old objection has run out of road.

The Regulators Got Out of the Way

The single biggest change of the past two years has been legal rather than technical. Three of the world's largest financial jurisdictions enacted stablecoin frameworks within a fourteen-month window, and the regulatory uncertainty that kept Tier-1 banks out of the room has been replaced by a compliance architecture they recognise.

The US GENIUS Act was signed into law on 18 July 2025. It requires payment stablecoin issuers to hold full one-to-one reserves in high-quality liquid assets. It also forces monthly attestations and a federal charter, or a state framework with similar oversight. Final implementing regulations are due by July 2026; the law takes effect no later than January 2027. The European Union's MiCA regulation has been fully in force since 30 December 2024. By the end of 2025, ESMA counted 30 licensed stablecoin issuers and 102 registered crypto-asset service providers across the bloc. Hong Kong's Stablecoins Ordinance passed on 21 May 2025 and took effect on 1 August. It requires 100 percent reserve backing and a paid-up capital floor of HK$25 million for any fiat-referenced stablecoin issued in or from the territory.

Whether one approves of the details or not, the practical effect for institutional players is the same: the lawyers can now sign off. A treasury team at a Fortune 500 company can move stablecoin transfers through a federally regulated issuer with the same diligence used for any other counterparty. That is the gating condition for the next phase of adoption, and it has already been met. The voluntary pilots of 2022 and 2023 are giving way to scheduled production deployments with named compliance owners.

AI Agents Are the Next Users of the Rails

The most interesting question in payments right now is not human at all. It is how software agents, large language models given the ability to act on a user's behalf, will pay for the things they do. They need to buy compute, fetch paid data, call APIs, and increasingly transact with one another. Cards do not work for this. There is no human to type a CVV; chargeback rules and authentication flows assume a person in the loop. Bank rails are too slow and too expensive for sub-dollar machine-to-machine spending. The legacy payment system was not designed for participants without a wallet, a phone, or a credit history. The decentralised, programmable side of crypto turns out to be a much better fit for that use case.

Coinbase's x402 protocol, launched in May 2025, addresses exactly this gap. It revives an obscure corner of the HTTP standard, status code 402, "Payment Required", and ties it to USDC settlement on Base, Polygon, Arbitrum, and Solana. An agent calling an API receives a 402 response, pays the required amount in USDC, and gets the resource on the retry. Finality is near-instant; cost is fractions of a cent. By September 2025 Coinbase and Cloudflare had co-founded the x402 Foundation; its core members now include Google, Visa, AWS, Anthropic, Circle, and Vercel.

In May 2026 Amazon brought the protocol into its core developer stack. AWS Bedrock AgentCore Payments shipped in preview with native x402 support, advertising sub-two-second settlement at roughly $0.0001 per transaction. Stripe's Agentic Commerce Protocol, launched with OpenAI in September 2025, is being tested by Microsoft Copilot, Anthropic, and Perplexity. Skyfire, a venture-backed agent-payment network, exited beta in March 2025 using USDC on Base and went on to publish a Know Your Agent framework, which is KYC for software, essentially.

| Method | Works for an autonomous agent? | Why or why not |

|---|---|---|

| Credit or debit card | Poorly | Built around human authentication, CVV, and chargebacks |

| Bank wire (ACH or SWIFT) | No | Too slow and too expensive for sub-dollar transactions |

| Stored value with a single platform | Partly | Closed system, locks the agent to one vendor |

| Stablecoin over x402 | Yes | Programmable, settles in seconds, fractions of a cent |

The numbers attached to this opportunity are large enough that they explain the rush. a16z estimates that non-human agents in financial services already outnumber human employees by roughly 100 to 1. In the firm's phrasing, those agents remain "effectively unbanked." McKinsey projects agentic commerce could account for $3 trillion to $5 trillion of global commerce by 2030. The first time I watched a model purchase API credits without a human in the loop, the disorienting part was not the technology; it was the realisation that nothing in the legacy stack would have let it happen.

How Crypto Platforms Became Operating Companies

A second-order effect of all this is that the leading crypto platforms have stopped resembling exchanges in any meaningful sense. Coinbase reported $7.18 billion in revenue for fiscal 2025. The mix spans spot trading, derivatives, staking, custody, a payments business, and its Base layer-two network. Base alone now holds about $5.2 billion in stablecoins and processes more than ten million transactions a day. Consumer trading volume on Coinbase ran at $78.1 billion in Q1 2025 and $43 billion in Q2; the asset-classes mix has tilted firmly toward derivatives and yield-bearing products alongside spot, with monthly active users in the 8.8 million range. Binance and Kraken, neither of which files public statements, run comparable product surfaces. The closest traditional-finance analogue is no longer a brokerage. It is a vertically integrated bank with a software-engineering culture, sitting somewhere between equity-trading platforms, custody banks, and stablecoin issuance — and treated by US regulators as all three at once. As blockchain technology matures, the leading crypto platforms now sit as the working layer between legacy finance and the new digital asset ecosystem, with product lines that twenty years ago would have required three separately chartered firms.

A second tier sits beneath them: merchant-facing payment processors such as Plisio, BitPay, and NOWPayments that handle the actual checkout integrations for the businesses moving onto stablecoin rails. Roughly 25 million merchants worldwide now accept some form of cryptocurrency, by industry counts — a figure that includes everyone from bitcoin-friendly retailers to treasury teams holding stablecoins as a cash equivalent. These are the platforms most consumers will brush against without noticing — the rails inside the rails.

What This Means for People Who Aren't Watching

For most people, none of this will feel like a revolution. That is the point. Mobile internet did not announce itself; it arrived inside the apps people already used, until one day a phone was the default. Stablecoin rails are following the same path. A merchant in Buenos Aires takes a USDC payment. A SaaS company pays Vietnamese contractors from a treasury wallet. An AI agent buys a few cents of computation on Bedrock. None of these are advertised as "using crypto." They are simply transactions that work better than the ones they replace.

The platform layer wins by becoming infrastructure, not by becoming a destination — and that is how crypto platforms are shaping the future of global financial services without most users ever noticing. When that transition is complete, the open question is whether the word "crypto" still does any useful work — or whether the rails will simply be called payments again, the way nobody calls TCP/IP an internet protocol any more.