NVTS Stock: Is Navitas Semiconductor a Buy in 2026?

One announcement from NVIDIA did something remarkable. It turned a forgotten $350 million penny stock into a company worth nearly $7 billion, almost overnight, while the company's actual revenue was falling. That contradiction is the entire story of NVTS stock.

Everything else is detail around it. The technology is real. The catalyst is real. But the price already assumes the dream comes true, on a schedule nobody can guarantee. So the question is not whether Navitas makes good chips. It does. The question is whether you are buying a business or buying a bet on what NVIDIA might do for it. Be honest about which.

What NVTS Stock and Navitas Semiconductor Are

When you buy NVTS stock, you own a piece of Navitas Semiconductor Corporation, a small power-chip company that trades on the Nasdaq. Note the word small. This is not a chip giant. It is a niche specialist that, until 2025, almost nobody outside the power-electronics world had heard of. A backwater, basically. Then NVIDIA called.

Navitas went public the way many speculative names did, through a SPAC merger, joining Live Oak Acquisition in 2021. It is headquartered in Torrance, California, and has been led by CEO Chris Allexandre since August 2025. One thing to be clear about up front: Navitas does not make the brains of a computer. It makes the muscles. Its chips manage power, not processing, which is why the NVIDIA story matters so much and is also so easy to misread.

So when you see NVTS in the same headline as NVIDIA, do not assume Navitas is suddenly an AI chipmaker. It is a power-component supplier hoping to ride the AI build-out. Different role, very different investment risk.

What Navitas Semiconductor Actually Makes

The technology here is worth understanding, because it is the real asset. Navitas builds power semiconductors from two next-generation materials: gallium nitride, or GaN, and silicon carbide, or SiC.

What do they do? In plain terms, they move electricity more efficiently than the old silicon chips that have run power supplies for decades. Less energy wasted as heat. Smaller, cooler, faster components. For years the main use was mundane: the small fast phone chargers in your drawer, plus solar inverters and electric-vehicle systems.

Then AI changed the stakes. Modern AI data centers burn enormous amounts of power, and every watt lost in power conversion is a watt of cost and heat — which is exactly what pushed NVTS into the spotlight. Suddenly, chips that deliver power more efficiently are not a nice-to-have. They are a bottleneck-breaker. Navitas makes its GaN devices in partnership with TSMC, the world's top chip manufacturer, which lends real credibility, and it held an estimated 16% of the GaN power market as of 2023. The appeal for AI is concrete. GaN switches power faster and runs cooler than silicon, which lets data centers convert electricity at higher voltages with far less loss. At hyperscale, even a few points of efficiency translate into megawatts and millions of dollars saved. The technology is legitimate. Hold that thought, because the financials tell a harder story.

The NVIDIA Deal That Changed NVTS Stock

This is the moment that created the stock as you see it today. On May 21, 2025, NVIDIA announced it had selected Navitas to help build its next-generation 800-volt high-voltage DC power architecture for AI data centers. The market reacted instantly. NVTS jumped roughly 150% in a single session and finished the month up about 164%. Nineteen times its old size, on one press release.

Why such a violent move? Because of where it came from. Before the announcement, Navitas was worth around $350 million, a micro-cap nobody followed. The NVIDIA halo re-rated it to roughly $6.7 billion. That is not a normal stock pop. That is the market deciding, in a day, that a tiny company might sit inside the most important spending wave in technology, the AI infrastructure build-out.

Here is the part the headline glosses over. Being selected for a power architecture is a design win and a collaboration. It is a vote of confidence, and a genuinely big one. It is not the same as a flood of revenue arriving next quarter. The chips still have to ship in volume, the data-center standard still has to roll out, and competitors are chasing the same prize. The catalyst is real. The payoff is a promise, not yet a number on the income statement.

Timing matters too. The 800V architecture targets data centers being built over the next few years, not last quarter, so the real revenue, if it comes, shows up later. What investors bought in May 2025 was a credible seat at the table for the AI-power transition, and they paid up for it the same day.

NVTS Stock Price: From Penny Stock to $30+

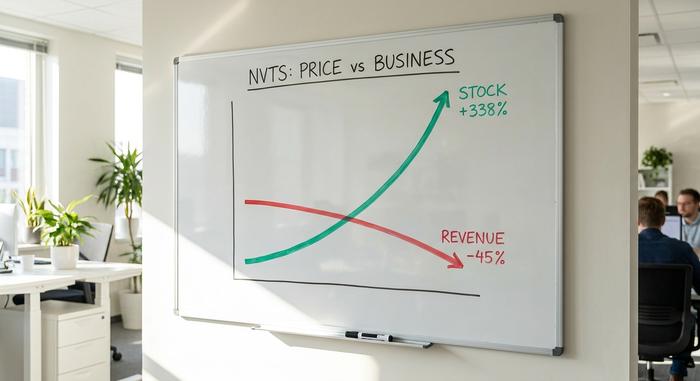

The NVTS stock price chart looks less like a company and more like a theme. Over the past year the stock ran from a low of $4.95 to a high of $33.82, a gain of more than 338%, and it recently trades around $28.50. That puts the market value near $6.66 billion.

| NVTS stock snapshot | Figure |

|---|---|

| Recent price | ~$28.51 (late May 2026) |

| 52-week range | $4.95 - $33.82 |

| 1-year return | +338% |

| Market cap | ~$6.66B |

| Short interest | ~18% of float |

A move like that is momentum, not valuation. With roughly 18% of the float sold short, NVTS also carries the fuel for violent swings in both directions. When an AI-power headline hits, it can squeeze higher fast. When enthusiasm fades, the drop is just as sharp. This is a stock that trades on a story, and stories move quickly.

Navitas Semiconductor Earnings: Revenue Is Falling

Now the part the chart conveniently ignores, so read it slowly. While NVTS stock quadrupled, revenue went the other way.

Navitas Semiconductor reported full-year 2025 revenue of $45.92 million. That was down almost 45% from $83.3 million the year before. The cause was the collapse of its legacy business: the mobile and consumer charger market, heavily tied to China, fell apart. So the company everyone re-rated for the future was, in the present, shrinking fast.

The newer data-center revenue is real, but it is tiny. First-quarter 2026 revenue was just $8.6 million, up 18% sequentially, with the next quarter guided to around $10 million. Navitas does not yet break out data-center sales as a separate line. In other words, 2026 is a transition year, not a ramp year. The old business is gone, and the new one has barely begun. Management frames this as a deliberate pivot, walking away from low-margin consumer chargers to chase higher-value data-center and EV power. That is a defensible strategy. It also means the income statement gets worse before it gets better, and investors are asked to look past the gap on faith.

| Navitas financials | Figure |

|---|---|

| FY2025 revenue | $45.92M (-44.9% YoY) |

| FY2024 revenue | $83.3M |

| Q1 2026 revenue | $8.6M (+18% sequential) |

| Q2 2026 guidance | ~$10M |

| Net income | Ongoing losses |

That is the tension in one table. A multi-billion-dollar valuation sitting on top of revenue that is both small and recently shrinking. The bulls are buying the next three years. The bears are reading this year.

NVTS Valuation: 165x Sales on Shrinking Revenue

This is the number that should anchor every decision you make about NVTS. The stock trades at roughly 165 times sales.

Let that sink in. A mature, profitable chip company might trade at 5 to 10 times sales. A fast-growing one, 15 to 25. NVTS trades at 165 times revenue that is currently falling. There is no version of standard valuation math that supports that price on today's business. You are not paying for what Navitas earns. You are paying entirely for a pipeline that has not yet converted to revenue.

The bull anchor for that price is a reported design-win pipeline worth around $2.4 billion, plus $221 million of cash that buys roughly seven quarters of runway. If even a fraction of that pipeline becomes real revenue, the multiple compresses fast and the stock could grow into its valuation. Compared with bigger, cheaper, profitable power-chip peers like Infineon, onsemi, and Power Integrations, though, NVTS is priced for a future none of them get credit for. That is the whole bet: that the small specialist wins the AI-power era outright. Put the gap in plain numbers. A company earning roughly $46 million in falling annual revenue is valued like one earning many times that. To justify $6.66 billion at a normal chip multiple, Navitas would eventually need sustained, profitable revenue in the hundreds of millions. That is years away, if it arrives at all.

Analyst Ratings and Forecast: Wall Street Sees Downside

This is something you rarely see. The analyst consensus on NVTS stock is openly bearish on price. The rating is a Hold, and the median price target sits near $13 to $14, roughly 50% below where the stock trades.

| Analyst view | Figure |

|---|---|

| Consensus rating | Hold |

| Median price target | ~$13-14 |

| Bull case | Needham, Buy, $21 |

| Bear case | Morgan Stanley, Underweight, $13.70 |

| Recent price | ~$28.51 |

Read that gap. A median target half the current price is Wall Street saying the NVIDIA excitement has pushed the stock far past what the numbers justify. The bulls argue the pipeline changes everything; the bears point at the valuation and the falling revenue. When the consensus target implies a halving, that is not a detail to skip past.

The Bull and Bear Case for NVTS Stock

The two sides here are not close. They are arguing about different time horizons.

The bull case is a genuine catalyst bolted to real technology. NVIDIA, the most important company in AI, picked Navitas for a core part of its next data-center power design. GaN and SiC are the efficient future of power electronics, the data-center build-out is enormous, the design-win pipeline is reportedly $2.4 billion, and $221 million of cash funds the wait. If the AI-power thesis plays out and Navitas captures even a slice, today looks cheap.

The bear case is simpler and lives in the present. Revenue fell 45%. The stock trades at 165 times sales. Analysts see roughly 50% downside. Share count has nearly doubled since 2021, diluting holders. And Navitas is a small player swimming against giants like Infineon and onsemi in a brutally competitive sector. The catalyst is real; the price ran far ahead of it.

| Bull case | Bear case |

|---|---|

| NVIDIA 800V design win | Revenue -45% in 2025 |

| ~$2.4B design-win pipeline | ~165x price-to-sales |

| GaN/SiC efficiency tailwind | ~50% analyst downside |

| $221M cash, ~7 quarters | ~95% dilution since 2021 |

Investors who want the AI-power theme with less single-stock risk can also find Navitas inside several semiconductor ETFs that spread the bet across the sector. My honest read is that NVTS is a real technology story wrapped in a stock price that already spent the next several years of good news. The company could absolutely succeed and still be a poor investment from here, simply because the entry price is so high. Catalyst and valuation are two different questions, and right now the valuation is the one doing the talking. There is also a middle path worth naming. You can believe the AI-power thesis completely and still wait for a better entry, because a stock priced for perfection tends to hand you cheaper chances later, when the hype cools and the numbers finally have to do the work.

Conclusion: Is NVTS Stock Worth It in 2026?

Navitas has something most speculative stocks lack: a named, enormous customer interested in its technology, and a product the AI era genuinely needs. That is not nothing. But at 165 times falling sales, with analysts modeling a 50% drop, the price already assumes the data-center ramp arrives on time and at scale, which is exactly the thing that has not happened yet.

So ask yourself the honest question before you buy NVTS stock. Are you buying the technology, or are you buying the hope, and can you sit through the steep drawdown the analysts are openly forecasting if the ramp slips even a year? If you believe in the AI-power thesis and can hold through volatility, NVTS is a credible way to express it. If you are chasing a chart that already tripled, that is usually where these stories turn in finance.