Nvidia Stock: Is NVDA Priced for a Fall in 2026?

Here is the paradox that should frame how you think about Nvidia stock. NVDA is the most valuable company on earth, worth roughly $5.2 trillion, and in its most recent quarter it grew revenue about 85% from a year earlier. A company that large is not supposed to grow that fast. And yet, measured against next year's expected earnings, the stock trades at around 17 times profit, cheaper than plenty of slow-growing software names. The bull case almost writes itself. So the more useful question, the one most quote pages never touch, is the other side of the ledger: what could actually break this, and is the price already paying you to take that risk?

What Nvidia's Business Actually Looks Like Now

Nvidia stock is no longer a bet on graphics cards. The company has become something closer to a toll booth on artificial intelligence, and almost every line of the income statement now reflects that single shift.

From graphics cards to AI compute

Nvidia spent its first decades selling GeForce graphics chips — the graphics processing unit (GPU) that rendered video-game worlds — under CEO Jensen Huang. The same hardware turned out to be ideal for the heavy parallel math behind modern AI, the engine that trains and runs today's largest AI models, and the company pivoted hard into accelerated computing for data centers. The real moat is not just the silicon. It is CUDA, Nvidia's software layer, which developers have spent fifteen years building on top of. A rival can copy a chip far faster than it can copy that ecosystem, and that lock-in is the quiet engine under the stock. It is why customers keep paying premium prices when cheaper hardware exists: the cost of rewriting years of CUDA-based code usually dwarfs whatever they would save on the chip itself. Software, not silicon, is the part of Nvidia that is hardest to compete away, and it is the reason the company can charge the margins it does.

Data center is now about 92% of revenue

The concentration inside Nvidia Corporation is staggering. In the most recent quarter, data center products generated about $75.2 billion of Nvidia's roughly $81.6 billion in total revenue, according to the company's SEC filing. That is more than nine of every ten dollars coming from one product line sold mostly to a handful of giant customers. It is the source of the explosive growth, and also the source of the biggest risk. A few years ago gaming was the largest segment; today data center dwarfs everything else combined. That kind of pivot is rare for a company already this size, and it means the old way of valuing Nvidia as a chip cyclical no longer fits. You are valuing an AI-infrastructure supplier whose fortunes rise and fall with one spending cycle.

The leftovers: gaming, automotive, and networking

What used to be the whole company is now a rounding error. Gaming graphics still sells, the automotive segment supplies chips for assisted driving, professional visualization tools serve designers and studios, and networking platforms tie AI clusters together. From its Santa Clara headquarters, Nvidia still runs all of these computing platforms as real businesses. None of them moves the stock anymore. When people argue about Nvidia, they are arguing about data center demand and nothing else.

Nvidia Stock Price, Earnings and Valuation

The valuation is the single most misunderstood thing about NVDA. A five-trillion-dollar price tag sounds like the definition of an expensive stock. On forward earnings, it is not.

The numbers behind the $5 trillion

Pull up an Nvidia stock quote in early June 2026 and the price sat near $214.75, after a 10-for-1 stock split in June 2024 that made the shares look approachable again. That works out to a market capitalization around $5.2 trillion, the largest of any public company in the world. For fiscal 2026, which ended in late January, the company reported revenue of about $215.9 billion, up 65% year over year, with net income near $120.1 billion and a gross margin above 74%, per its annual 10-K filing. A 74% gross margin is software-company territory, extraordinary for a business that ships physical chips by the ton.

Why a $5 trillion stock can still look cheap

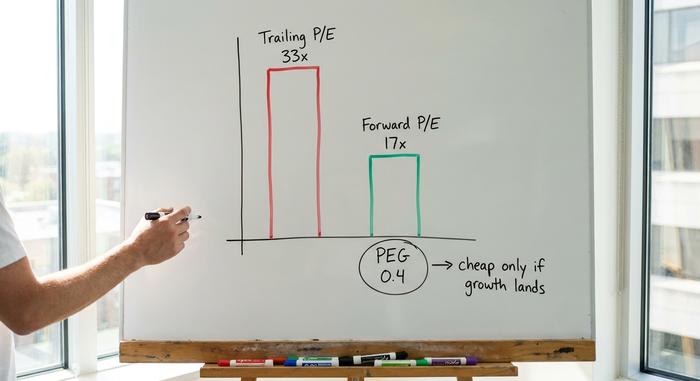

Here the measured view matters. On trailing earnings, NVDA trades near 33 times profit, which sounds rich. On next year's expected earnings, the multiple drops to roughly 17 times, and the PEG ratio, which weighs price against growth, sits near 0.4. A PEG below 1 traditionally signals a stock that is cheap relative to how fast it is growing. By that yardstick Nvidia is actually less demanding than peers like AMD or Broadcom. The catch is simple and important: the forward multiple only stays cheap if the forecast growth actually lands. Pay 17 times earnings that never arrive and you have overpaid badly. This is the heart of the Nvidia stock debate. The trailing number says expensive, the forward number says bargain, and the gap between them is entirely a question of whether analysts' steep growth estimates come true. A forward P/E is a forecast wearing the costume of a fact, and with NVDA the forecast is doing almost all the work.

| Nvidia valuation snapshot (early June 2026) | Figure |

|---|---|

| Share price | ~$214.75 |

| Market cap | ~$5.2 trillion (world's #1) |

| Trailing P/E | ~33x |

| Forward P/E | ~17x |

| PEG ratio | ~0.4 |

| Gross margin | ~74% |

| FY2026 revenue | $215.9B (+65% YoY) |

The tiny dividend and the split

For income investors, there is essentially nothing here. Nvidia pays a token dividend with a dividend yield rounding to roughly zero, a symbolic gesture rather than a reason to own the shares. The 2024 stock split changed the optics, not the value: ten cheaper shares are worth what one expensive share was. Your entire return from this stock comes from the price, which means you are buying growth, not income.

What Analyst Ratings Say About NVDA

The analyst picture on Nvidia stock is unusual, and worth a skeptical read precisely because it is so positive. Across roughly 61 analysts, the consensus rating is a clear Strong Buy, and the average price target sits near $297, implying close to 38% upside from the recent price, according to StockAnalysis data as of June 2026. That is the opposite of the pattern you see in stretched, hype-driven names, where targets quietly sit below the market price. When the average analyst still sees nearly 40% more room after a stock has already become the largest on the planet, it tells you the Street believes the earnings will keep compounding fast enough to justify it.

Two other numbers fill in the picture. NVDA carries a beta around 2.2, so it tends to swing roughly twice as hard as the broad market, up and down. And short interest is tiny, near 1.3% of the float, meaning almost nobody is betting against it. That near-unanimous bullishness is itself a mild risk: when expectations are this high and skeptics this few, even a small disappointment can move the stock sharply, because there is little doubt left to convert into buying.

The Risks That Could Break the Nvidia Thesis

This is the section the quote pages skip when writing about Nvidia stock, and it is the one that actually earns its keep. The forward multiple looks cheap because the market is quietly pricing in real, stackable risks. Take them seriously, the way a careful analyst weighs vulnerabilities against a baseline.

Customer concentration and the capex question

Most of Nvidia's data center revenue flows from a small group of hyperscale cloud companies, the same firms expected to spend somewhere around $700 billion combined on AI infrastructure in 2026, based on CNBC's tally of their capex plans. That spending is the baseline everyone assumes. The vulnerability is that capex like this moves in waves. If these customers decide they have bought enough compute for a while, or if their own returns on AI disappoint, the digestion phase would hit Nvidia harder than almost any company in history, because so much rides on so few buyers. The filings do not even name them; they appear as a few unidentified customers, each large enough to swing a quarter on its own. That is concentration most companies would never survive, and Nvidia carries it at a $5 trillion valuation.

China and export controls

Policy can erase a market overnight. Export restrictions on Nvidia's China-bound H20 chips already forced a $4.5 billion inventory charge and cost the company roughly $8 billion in lost revenue in a single quarter. China was once a major slice of demand. A pen stroke in Washington can shrink it again, and Nvidia has little control over that lever.

Custom silicon and circular financing

The competition is not standing still, and it is not only AMD. Broadcom and Marvell design custom AI chips, or ASICs, directly for the hyperscalers, and those custom designs are projected to take a meaningful share of AI server shipments, on some estimates approaching a quarter or more by 2026. Nvidia's own chief executive has even floated Marvell as a future trillion-dollar company. On top of that, watch the circular financing: Through equity stakes and strategic partnerships, Nvidia has tied itself to customers like CoreWeave and to massive buildouts such as OpenAI's, where the same dollars can appear to flow in a loop, with Nvidia funding the customers who then buy Nvidia chips. Regulators in Europe have already started asking questions about how much of the demand is genuinely independent. None of this is fatal today. All of it is the kind of vulnerability that looks harmless in good times and obvious in hindsight after a downturn.

Nvidia vs Other AI Chip Stocks

Set against its rivals, Nvidia stock is both the most dominant and, oddly, not the most expensive on forward earnings. AMD trades at a far higher forward multiple while chasing a fraction of the AI revenue. Broadcom commands a premium for its custom-chip and networking franchise. TSMC, which actually manufactures most of these chips, is cheaper but carries direct geopolitical exposure to Taiwan. The table below frames the trade-off.

| AI chip stock | Forward P/E (approx.) | Note |

|---|---|---|

| Nvidia (NVDA) | ~17x | AI-compute leader, CUDA moat |

| AMD | far higher | smaller AI revenue base |

| Broadcom (AVGO) | premium | custom ASICs + networking |

| TSMC | lower | foundry, Taiwan risk |

The point is not that Nvidia is risk-free. It is that, among the obvious AI chip plays, the market is charging less for the leader's growth than for several of its chasers. That is rare. Usually the dominant company in a hot sector carries the fattest multiple, and investors pay up for safety. Here the leader is priced as though its dominance is already fading, which is either a gift or a warning, depending on how the next two years of AI demand play out. Reading that signal correctly is most of the job of owning this stock.

Is Nvidia Stock a Buy in 2026? The Verdict

Here is my honest read. NVDA is the cheapest-looking mega-cap relative to its growth, but that discount is not a free lunch. It is the market's way of saying the hyper-growth has to slow eventually, and that a single bad capex cycle, export shock, or ASIC breakthrough could bring the slowdown early. Buying Nvidia stock is a bet that the AI buildout has several more years left and that no rival cracks the CUDA moat before then. If you take that bet, size it for the volatility it carries, because a stock with a beta above 2 can hand you a 30% to 40% drawdown without the long-term story changing at all. A position you cannot hold through a scary quarter is the wrong size, no matter how convinced you are. The investors who do worst with Nvidia stock are usually the ones who bought too much at the top and sold in the panic, not the ones who were wrong about the company. The question to settle before you buy is not whether Nvidia is a great company. It plainly is. It is whether the next few years of AI spending live up to a price that already assumes they will.