Best Semiconductor Stocks to Buy in 2026: AI, ETFs, Risks

One company sells close to nine of every ten dollars of AI computing power. That same company is worth more than half of the ten largest chipmakers put together. Sit with that for a second, because it is the bull case and the bear case for semiconductor stocks in one number. Those ten giants were worth about $9.5 trillion at the end of 2025, up 46% in a year, on global chip sales of $791.7 billion. The money is real. The growth is real. So is the fragility.

This is not another ranked buy-list. It is a way to think about semiconductor stocks the way the sector actually behaves: a cyclical, chokepoint-driven business riding an AI wave that could keep running or snap back without warning. We will map the supply chain, name the leaders worth owning, weigh the ETFs that spread the risk, and stay honest about how far chips can fall.

What a semiconductor stock actually is

Buy a semiconductor stock and you own a slice of a company that designs, builds, or equips chips. Those chips sit inside phones, cars, data centers, even the power grid. Analysts call the sector an economic barometer, and they have a point: chip orders fall first when the economy cools and rebound first when it warms. That is why sales jumped 25.6% in 2025 to $791.7 billion, and also why the same stocks can crater the moment the cycle turns. You are buying a commodity business wrapped around brilliant engineering. Both halves matter, and most buy-lists only sell you the second one.

Inside the semiconductor supply chain and EUV

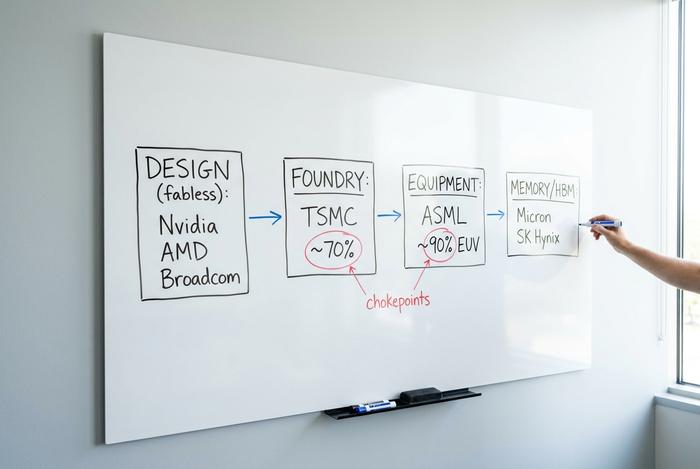

Here is the part most buy-lists skip, and it is the most useful thing to understand. Where a company sits in the supply chain decides how strong its moat is, and the strongest moats are not always the famous chip designers.

The industry splits into a few clear roles. Fabless designers create the chips but own no factories: Nvidia, AMD, Broadcom, Qualcomm, and Marvell live here. Foundries do the manufacturing for everyone else, and one company dominates that layer. Integrated device manufacturers, or IDMs, both design and build their own chips, which is the old Intel model and how Texas Instruments and Micron operate. Then there are the equipment makers who sell the machines that build the chips, and the memory specialists who supply the high-bandwidth memory that AI accelerators are starving for.

The real chokepoints sit at the edges of that map. Taiwan Semiconductor, the world's foundry backbone, holds roughly 70% of the leading-edge semiconductor manufacturing market, which means most advanced chips on earth are made by one firm on one island. ASML is even more concentrated: it is the only company that makes extreme ultraviolet lithography machines, the room-sized tools needed to print the smallest transistors, giving it about 90% of the lithography market. Lam Research, KLA, and Applied Materials round out the equipment layer that nobody can build chips without.

There is a third chokepoint forming that fewer people talk about: memory and advanced packaging. AI accelerators are starving for high-bandwidth memory, and only a few firms make it well, chiefly Micron and SK Hynix. The packaging step that stitches logic and memory together — TSMC's CoWoS process — has become its own bottleneck, with supply sold out well ahead of demand. When a single packaging line gates how many AI chips the world can ship, that line is worth watching as closely as the chips themselves.

Why does this matter to an investor? Because a fabless designer can be out-designed next year, but you cannot out-design a monopoly on the machine that makes the machine. TSMC is pouring $52 to $56 billion into capital spending in 2026 and has committed $165 billion to its Arizona fabs. That spending is a tax everyone else pays and a moat TSMC keeps widening. The lesson is simple: when you buy a semiconductor stock, you are really buying a position in one layer of this stack, and the layers do not carry equal risk.

How AI demand drives the semiconductor industry

AI lifted chip demand, sure. The bigger change was who the industry sells to. A decade ago the marquee customer was a phone maker. Today it is a handful of hyperscale data center operators buying graphics processing units by the rack, and that AI infrastructure build-out has been wild for revenue. Deloitte pegs AI chips at roughly $500 billion in 2026, about half of all semiconductor revenue. Half, from a product category that barely registered ten years ago.

Nvidia shows what that looks like up close. Of its $215.9 billion in fiscal 2026 revenue, about $193.7 billion, near 90%, came from data center sales alone, and that line grew 65% in one year. Read that again. A company already this enormous still accelerated. Where does it go from here? The forecasters cannot agree on the number. WSTS pencils in $975 billion of global chip sales for 2026; Gartner reaches past $1.3 trillion. On the direction, though, nobody dissents.

There is a twist this boom carries that earlier ones did not. The wall is no longer transistor density. It is electricity. A data center can only pull so much power and shed so much heat, which makes performance per watt the number that now sorts winners from also-rans. Whoever holds the best process technology and the cleanest hardware-software fit wins that race. So the field narrows, again, to the same few names.

And here is the catch we keep circling. When a single buyer profile drives half a market, every stock tied to it tends to move together. Artificial intelligence infrastructure spending is the engine today. Engines stall.

Beyond AI: the global semiconductor industry

Not every semiconductor stock is an AI bet, and the second engine in the global semiconductor industry gets almost no coverage. After a 2.5-year inventory destocking slump, the industrial and analog side is recovering. Texas Instruments reported industrial revenue up about 30% year over year in its first quarter. Analog Devices posted $3.16 billion in quarterly revenue, up 30%, with industrial up 38%. ON Semiconductor, a power-chip specialist, saw its AI data center revenue grow about 30% quarter over quarter even as its core auto and industrial markets recovered. Electric vehicles, factory automation, and grid upgrades are pulling demand for semiconductors that have nothing to do with chatbots. If you want exposure to the sector without betting everything on AI accelerators, this corner is where to look.

Best semiconductor stocks to buy in 2026

The megacaps are not one trade, and treating them like one semiconductor stock is how people get hurt. Pull them apart by what they actually sell and what would break each thesis.

Start with Nvidia (NVDA). It leads AI compute and embodies the purest version of the concentration story, worth around $5.1 trillion. Then there is Taiwan Semiconductor Manufacturing (TSM), near $2.2 trillion, which builds almost everyone else's best chips, a great strength and a single geopolitical pressure point at once. Broadcom (AVGO) plays a quieter hand, pairing AI networking with custom silicon co-designed alongside the hyperscalers, so it is less of a straight GPU bet. And AMD? The challenger, chasing Nvidia in accelerators while keeping real ground in CPUs.

| Ticker | Company | Market cap | What it sells | Key risk |

|---|---|---|---|---|

| NVDA | Nvidia | ~$5.1T | AI GPUs, data center compute | Demand concentration, valuation |

| TSM | Taiwan Semiconductor | ~$2.2T | Leading-edge foundry | Taiwan geopolitics |

| AVGO | Broadcom | mega-cap | AI networking, custom silicon | Customer concentration |

| AMD | Advanced Micro Devices | large-cap | CPUs, AI accelerators | Out-executed by Nvidia |

My honest read: NVDA is the highest quality and the highest risk at once, TSM is the closest thing to a pick-and-shovel play, and AVGO is the one I keep coming back to because custom silicon makes it harder to displace.

Top semiconductor stocks and dividend payers

Beyond the AI darlings sit the stories that need patience. Intel (INTC) is a turnaround that lives or dies on manufacturing execution, not slideware. Texas Instruments (TXN) is an analog cash machine with steady industrial demand and, unusually for this sector, a real dividend. Qualcomm (QCOM) is pushing past smartphones into automotive and edge computing. Marvell (MRVL) rides the same AI networking trend as Broadcom but smaller. Micron (MU) is the memory cycle in pure form, brutal on the way down and explosive on the way up; its stock returned roughly 1,195% over three years through early 2026, which tells you everything about both the reward and the whiplash.

A word on income: most semiconductor stocks are growth plays, not yield vehicles. If you are screening for a dividend, the field narrows fast. Texas Instruments and Broadcom are the two names where payouts are a genuine part of the case. For the rest, you are buying capital appreciation and accepting the volatility that comes with it.

Semiconductor ETFs: SOXX, SMH and your portfolio

For most readers, a semiconductor ETF is the rational default. It spreads single-stock risk across the most volatile corner of tech, which is exactly where diversification earns its keep. The two big funds are the iShares Semiconductor ETF (SOXX) and the VanEck Semiconductor ETF (SMH).

| Ticker | Fund | AUM | ~12-month return | Note |

|---|---|---|---|---|

| SMH | VanEck Semiconductor | $66.9B | +151.6% | More top-heavy in NVDA/TSM |

| SOXX | iShares Semiconductor | $36.0B | +180.2% | Slightly broader US tilt |

Know what you are buying, though. Both funds are cap-weighted, so they lean hard on the same megacaps. An ETF labeled "diversified" that puts a fifth of its weight in one stock is not as spread out as it sounds. For a portfolio, that is fine as a core holding; just do not assume it cancels out the concentration risk we keep circling back to.

Benefits and risks of semiconductor stocks

Semiconductor stocks carry structural upside that is easy to sell. The downside is where I want to spend time, because the listicles bury it.

Risk one is cyclicality. The Philadelphia Semiconductor Index has fallen 82% (2000), 52% (2008), and 35% (2022). The 2022 drawdown recovered in about 14 months, but a 35% fall tests anyone's conviction, and the dot-com crash took years. This sector falls harder than almost any other in tech.

Risk two is geopolitics, and it is no longer hypothetical. US export controls cut Nvidia's China revenue by 63% year over year to about $3 billion in one quarter, and the company took a $4.5 billion inventory charge on its H20 chips, roughly $8 billion in total China damage across 2025. Every major fabless name carries some version of this exposure, and TSMC's home in Taiwan is the largest single geopolitical question in the entire market.

Risk three is concentration and price. The top ten companies are worth $9.5 trillion, with Nvidia alone near 55% of that. The industry's average price-to-earnings ratio sits around 53, which prices in years of flawless growth. Supply chain disruptions, a single weak earnings call, or a cooling of AI capital spending could reset those multiples fast. Strong free cash flow and pricing power cushion the best names, but they do not make them cheap.

There is a subtler trap worth naming, because the cyclicality and the valuation interact. Chip earnings tend to look cheapest right at the top of the cycle, when profits are peaking and the price-to-earnings ratio briefly compresses. Buy into that apparent bargain just as demand rolls over, and the multiple expands again on falling earnings while the share price drops. Veterans call it the peak-earnings trap, and it is the single most common way investors misread this sector. A low P/E on a chip stock is not automatically a discount; sometimes it is a warning.

Investing in semiconductor stocks: how to start

Practical close. First, pick your lane: individual names if you want to express a view, an ETF if you want the sector without the single-stock landmines. Second, size the position for volatility, because a holding that can drop 35% should not be one you need to sell in a panic. Third, open a brokerage account, search the ticker, choose how many shares, and place the order. The mechanics are easy. The discipline is the hard part.

The bottom line on semiconductor stocks

The semiconductor sector is in a real AI-led supercycle, and the numbers backing it are not hype. But the right question is not "which semiconductor stock to buy." It is "how much concentration and cyclicality can my portfolio actually carry." Answer that honestly, decide whether you want the chokepoints, the cycle plays, or just the ETF, and the individual picks get a lot simpler.