Best AI Stocks to Buy in 2026: Picks and Bubble Risk

Seven companies now make up about 35% of the entire S&P 500, and they drove roughly 42% of the index's gain in 2025. The ten largest stocks account for close to 40% of the market, higher than the 27% peak reached during the dot-com mania in 2000. If you own an index fund, you already own a large basket of AI stocks whether you chose them or not. So the useful questions are not "should I get exposure to AI" but which names to own on purpose, and whether the whole trade has run too hot.

This guide does both. It covers investing in AI stocks from the stack up: names the companies worth owning, and then runs the bubble math honestly, with numbers rather than vibes. I am not here to talk you into the trade or out of it. The aim is to hand you a framework and let you judge it yourself.

What artificial intelligence stocks really are

An AI stock is not one kind of company. It is a position somewhere on a stack, and the risk changes sharply depending on where you stand. A chipmaker, a cloud provider, a model lab, and a software vendor are all AI companies, and all "AI stocks," but they earn money in completely different ways. Gartner expects total AI spending to reach $2.59 trillion in 2026, up 47% in a year, and that flood does not reach every layer equally. Knowing which layer you are buying is the first real decision. The rest of this guide walks the stack, layer by layer.

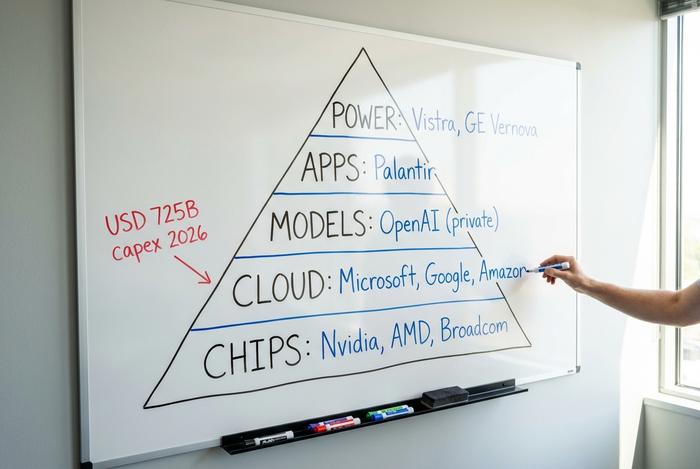

The AI stack: from AI chips to AI applications

Picture AI investing as five layers, stacked from the silicon up. The profits are not spread evenly across them. Right now the bottom layer keeps most of the money.

At the base sit the AI chips. Nvidia (NVDA) designs the GPUs that train the largest models, with AMD chasing and Broadcom (AVGO) building custom AI accelerators for the cloud giants. Behind them, Taiwan Semiconductor actually manufactures the chips and Micron supplies the high-bandwidth memory those accelerators are starving for. This is the layer that has captured the clearest profits so far, because every model, every cloud, and every app has to rent or buy this hardware first. When demand outruns supply, the people who own the supply set the price. That is why the chip layer, not the flashy app layer, has produced the biggest stock gains of the cycle.

One layer up are the cloud hyperscalers, the companies renting out AI compute and cloud services by the hour. Microsoft (MSFT) runs Azure and holds a large stake in OpenAI. Alphabet (GOOGL) pairs Google Cloud with its own Gemini models. Amazon (AMZN) has AWS. These firms are spending astonishing sums to build the data centers that everything else depends on. Combined hyperscaler capital spending is set to hit $700 billion to $725 billion in 2026, up about 77% from roughly $410 billion the year before.

Above the clouds sit the model labs — the companies that train large language models — and here is the catch for stock pickers: the leaders, OpenAI and Anthropic, are private. You cannot buy them directly, so the usual route is through their backers, mainly Microsoft and Amazon.

The top layer is software and applications, where companies like Palantir (PLTR) sell AI that does a specific job. This is the layer investors find most exciting and where, so far, the profits are thinnest relative to the hype. Selling a model is easy; charging enough for it to justify a high stock price is not.

And there is a fifth layer most listicles ignore: power. Data centers need gigawatts, which pulls in energy and equipment names like GE Vernova, Vistra, and Eaton. As Fidelity's analysts put it, the next wave of gains is happening at the system level, not just the chip level. That is where AI infrastructure spending, projected at $1.43 trillion in 2026, actually lands. The lesson for a stock picker is simple: decide which layer you are buying before you buy it, because a dollar of AI revenue is worth far more to a chipmaker than to an app that may face ten competitors next year.

The best AI stocks to buy in 2026

The megacaps are not interchangeable. Separate them by how directly AI drives the business and what would break the thesis.

Nvidia is the compute leader, and the numbers are hard to argue with: fiscal 2025 revenue of $130.5 billion, up 114%, with the data center segment alone at $115.2 billion, up 142%. Microsoft monetizes AI through Azure and its OpenAI partnership, the cleanest enterprise play, though the capex needed to keep up is starting to weigh on its margins. Alphabet is the cheapest of the megacaps and owns the full stack from its own chips to the Gemini models, which is why I think it offers the best value of the group. Amazon sells AI mostly as AWS capacity, the same picks-and-shovels logic that made it a winner in the last cloud cycle. Broadcom designs the custom silicon the hyperscalers use to cut their Nvidia bills. Then there is Palantir, the software pure-play growing fast, Q1 2026 revenue of $1.63 billion, up 85%, the kind of revenue growth that excites the market, but priced at a level we will come back to.

| Ticker | Company | AI role | Key risk |

|---|---|---|---|

| NVDA | Nvidia | AI GPUs, data center compute | Demand concentration, valuation |

| MSFT | Microsoft | Azure cloud + OpenAI stake | Capex weighing on margins |

| GOOGL | Alphabet | Google Cloud + Gemini models | Ad-revenue antitrust risk |

| AMZN | Amazon | AWS AI infrastructure | Thin retail margins, debt |

| AVGO | Broadcom | Custom AI accelerators | Customer concentration |

| PLTR | Palantir | Enterprise AI software | Extreme valuation |

My honest read: Alphabet is the best risk-adjusted megacap because you get the whole stack at the cheapest multiple, Nvidia is the highest quality and the highest expectation, and Palantir is a wonderful business at a frightening price.

Top AI stocks beyond the Magnificent 7

The crowded trade is the megacaps. The under-owned plays sit one layer out, and the most interesting of them is power. Training and running huge AI models burns electricity, so independent power producers like Vistra and equipment makers like GE Vernova have quietly become AI stocks. Micron rides the memory cycle that AI accelerators depend on, brutal on the way down and explosive on the way up. Marvell sells AI networking silicon, smaller than Broadcom but levered to the same trend. AMD remains the only real challenger to Nvidia in accelerators.

These names give you AI exposure without paying megacap prices, but be clear-eyed: they are higher-beta. Power stocks in particular have already re-rated hard on the AI story, so some of the easy gains are gone. There is also a quieter appeal here. If the AI software boom disappoints but the data centers still get built, the picks-and-shovels names, the power, the memory, the networking, still get paid. They are a way to bet on the build-out without betting on which app wins. Treat this layer as satellite positions around a core, not the core itself.

AI ETFs vs individual stocks: best exposure

For most readers, an AI ETF is the rational default. It hands you dozens of AI technology companies in one trade and spares you the job of picking the winner of a fast-moving race. The catch is in the label. Most AI ETFs are cap-weighted, so they pile into the same megacaps you may already own through an S&P 500 fund.

| Ticker | Fund focus | Note |

|---|---|---|

| BOTZ | Robotics and AI hardware | Concentrated in a few big names |

| AIQ | Broad AI and big tech | Heavy megacap overlap with S&P 500 |

| AIEQ | AI-selected active portfolio | Uses AI to pick the holdings |

A common warning from fund analysts is that the top three to five holdings can be 20% to 30% of an AI ETF. So before you buy one for diversification, check what it actually holds. If it is mostly Nvidia, Microsoft, and Alphabet, you are concentrating, not spreading.

Are AI stocks in a bubble? The 2026 math

Here is the question everyone dances around. The honest answer is: parts of it, yes. The hardware looks fairly priced; the speculative software names and the spending-versus-revenue gap are where the danger lives. Weigh both sides.

Start with the bear case. Hyperscalers are on track to spend $700 billion to $725 billion on AI in 2026, yet Sequoia Capital estimated the industry faces a $500 billion to $600 billion annual gap between that spending and the AI revenue actually coming in, up from a $125 billion gap in 2023. Deloitte surveyed 1,854 firms and found only 15% report significant, measurable returns from generative AI, with typical payback running two to four years. Market concentration above the 2000 peak, and Palantir at roughly 97 times forward earnings, more than 400% above the software-industry median, both rhyme uncomfortably with past manias.

Now the bull case, and it is stronger than the doomers admit. This boom is funded with cash, not the debt and flimsy IPOs of 2000. The companies doing the spending are among the most profitable in history. Nvidia generated about $96.6 billion in free cash flow in a single year; Cisco, the poster child of the dot-com top, traded near 200 times earnings on just $2.67 billion of net income. And Nvidia's own forward price-to-earnings ratio sits around 24, below the semiconductor median. The leader of this cycle is cheaper than its peers, which was emphatically not true in 2000.

What would actually pop it? Watch for hyperscalers cutting capital spending, which would signal they no longer believe the demand is there, or a stretch of quarters where enterprise AI revenue keeps missing. If the $500 billion-plus spending-to-revenue gap stops closing, the market will eventually stop paying for promises. None of that has happened yet, but it is the scenario to track rather than the daily price swings.

| Measure | AI in 2026 | Dot-com in 2000 |

|---|---|---|

| Top-10 share of S&P 500 | ~39-40% | ~27% |

| Leader forward P/E | Nvidia ~24x | Cisco ~200x |

| Funding source | Cash from profits | Debt and IPO hype |

| Leader cash flow | Nvidia ~$96.6B FCF | Cisco ~$2.67B net income |

So is it a bubble? The froth is real in the speculative names and in the capex running ahead of revenue. The foundation, profitable companies funding real infrastructure, is not 2000. Both things are true at once.

Strategies for investing in AI stocks safely

Once you decide to invest in AI, a few rules keep any AI investment from wrecking a portfolio. Size the position for volatility; a holding that can drop 40% should never be one you are forced to sell in a panic. Spread your money across layers rather than betting everything on one chip designer. Use an ETF as your core and a few individual stocks as satellites, not the other way around. And because nobody can time a cycle this charged, buy in over time instead of all at one price. The mechanics are simple: open a brokerage account, search the ticker, choose a market or limit order, and place it. The discipline is the hard part. It is easy to buy an AI stock; it is much harder to hold a sensible amount of it through a 40% drawdown without either panic-selling at the bottom or doubling down at the top.

AI stocks to watch in late 2026

Two numbers will settle the bubble debate. First, the next round of hyperscaler capital spending guidance: if the giants keep raising it, the build-out has legs; if they trim, the market will flinch. Second, enterprise AI revenue and ROI data through the second half of 2026, the figure that tells us whether the spending is finally turning into profit. Watch Nvidia's data center guidance as the single cleanest read on AI demand. Those releases, not the headlines, are what matter next.

The bottom line on investing in AI stocks

Own AI stocks deliberately. Decide which layer you want, lean toward the cash-rich leaders over the story stocks, and size the position for the chance that the bubble worriers are partly right. The AI build-out is real and enormous, but real and enormous is not the same as cheap. Buy the infrastructure, respect the math, and let the speculative end of the market be somebody else's lottery ticket.