Tokenized Stocks: How Tokenized Equity Trading Works

When you buy a tokenized stock, you usually do not own the stock. You own a token that promises to track its price. That gap, between what the thing looks like and what you actually hold, is the whole story here, and most explainers skate right past it.

The product is growing fast regardless. Backed Finance's xStocks crossed $25 billion in total transaction volume in under eight months, and tokenized equities printed a single-day record of $3.57 billion in May 2026. So it is worth understanding properly: what a tokenized stock is, how you trade one, and where the arrangement bites.

What tokenized stocks actually are

A tokenized stock is a digital token, issued on a blockchain, that mirrors the price of a real share. Apple does not mint it. Tesla does not mint it. A third-party issuer, often a fintech startup, does, then sells you a claim that moves up and down with the underlying asset.

Most tokens today follow a one-to-one backing model: for every token in circulation, the issuer holds one real share in custody. Backed Finance dominates this corner. Its bCSPX, bCOIN, and bNVDA tokens made up close to 90% of all tokenized-stock value by mid-2025, according to Chainlink. The category is still small but moving quickly. Total tokenized-stock market cap sat near $2 million when xStocks launched in June 2025 and reached roughly $486 million by the first quarter of 2026, per CoinGecko's RWA report. A tokenized asset class that barely existed two years ago now trades billions a month.

How stock tokenization works on a blockchain

Here is where the phrase "tokenized stock" starts hiding things. Three different structures wear the same label, and they do not carry the same risk.

The first is asset-backed, or wrapped. An issuer like Backed Finance buys the real shares, parks them with a regulated custodian, and mints matching tokenized shares on public blockchains. xStocks works this way. The token is only as good as the custody behind it, but there is a real share somewhere.

The second is native issuance. The token itself is the security, created directly on-chain as equity shares on a blockchain, with no separate share sitting in a vault. This is rarer and leans entirely on regulators accepting that a blockchain entry can be the legal record of ownership.

The third is synthetic. No real share exists at all. Smart contracts track stock prices using collateral and an oracle feed, and pay out based on where the price moves. Chainlink is the common price source. You get exposure without anything behind it but code. What keeps a backed token near its share price is the redemption path: authorized parties can mint and burn tokens against the real shares, so arbitrage closes any gap. When that mechanism is healthy, the peg holds. When it stalls, the token can drift.

The shared advantage across all three is speed. A normal trade settles in two business days. A token transfer settles in seconds, written to an immutable ledger that anyone can audit. That sounds like a clean upgrade, and in narrow ways it is. But the history should keep you honest. Binance offered stock tokens in 2021 and shut the product within months under regulatory pressure. Blockchain technology was never the hard part.

| Structure | What backs it | Who issues | Main risk |

|---|---|---|---|

| Asset-backed (wrapped) | One real share per token, in custody | Issuer (e.g. Backed Finance) | Custodian or issuer failure |

| Native | Nothing separate; token is the security | On-chain issuer | Legal recognition still thin |

| Synthetic | Collateral plus a price oracle | Smart contract protocol | No real share, oracle failure |

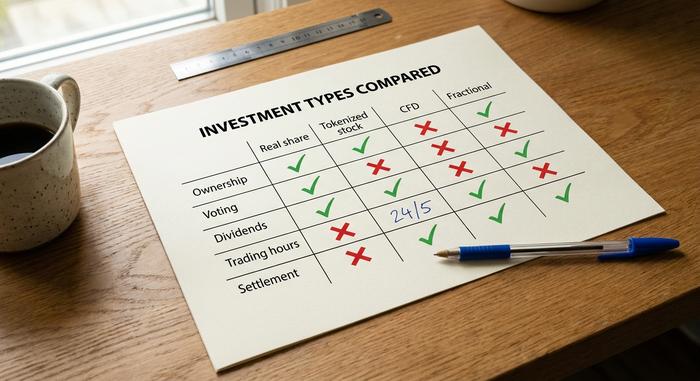

Tokenized stocks vs traditional stocks and CFDs

People blur three products that are not the same. A real share, a tokenized stock, and a contract for difference all give you price exposure to a company, but they hand you very different rights.

A traditional stock is ownership. You can vote, you collect a dividend, and in most regulated markets you get investor protection if your broker fails. A tokenized stock usually gives you the price and little else. Some issuers pass dividends through (Kraken reinvests them by raising your token balance), and some pass through nothing. Voting rights are typically gone. A CFD is different again: a leveraged contract with a broker on the other side, no token, no settlement on any ledger.

Some of the headline benefits already exist in an ordinary brokerage account. Fractional shares have been around since 2019. As TD Securities has noted, real institutional demand for round-the-clock equity trading is still thin. The novelty of tokenized equity is less "fractional and 24/7" and more "programmable and global."

| Feature | Real share | Tokenized stock | CFD | Fractional share |

|---|---|---|---|---|

| Ownership | Yes | No (claim) | No | Yes (partial) |

| Voting | Yes | Usually no | No | Yes |

| Dividends | Yes | Sometimes | Adjusted | Yes |

| Trading hours | Market hours | 24/5 | Broker hours | Market hours |

| Settlement | T+2 | Seconds | N/A | T+2 |

| Counterparty | Broker (regulated) | Issuer + custodian | Broker | Broker |

How to buy tokenized stocks on an exchange

If you want to trade tokenized stocks, strip away the marketing and the process looks a lot like buying any cryptocurrency. If you have used an exchange before, you already know most of it.

Start by picking a venue that actually lists them. Kraken's xStocks, Bybit, and Gate support the same Backed-issued tokens. Then clear KYC and, this is the part that trips people, check whether you are even allowed in. Kraken's xStocks are blocked in the United States and the European Economic Area. Europe broadly leads adoption, while US access is largely restricted to accredited investors because of how the SEC classifies these instruments.

Funding comes next. Tokenized stocks settle in stablecoins, usually USDC or USDT, so you convert fiat or crypto into the settlement asset first. Then you buy the ticker token, something like TSLAx, AAPLx, or NVDAx, often with a minimum as low as one dollar. That fractional access is real, even if the spread you pay is not always better than a normal broker's.

The last decision is custody, and it is the one that matters most. You can leave the token on the exchange, or withdraw it to your own Solana or Ethereum wallet. Self-custody is where the interesting part lives. Once the token is in your wallet, you can use it inside decentralized finance, without ever touching a stock exchange. Kamino became the first major DeFi lender to accept tokenized equities as collateral. Selling runs nearly 24 hours a day on weekdays and clears almost instantly. No T+2, no waiting for Monday morning.

Tokenized equity platforms and real-world examples

The market for tokenized stocks has a quiet structural feature: most of it runs on one issuer's rails. That is why it works smoothly, and also why it is fragile.

xStocks, built by Backed Finance and acquired by Kraken at the end of 2025, supplies the equity tokens that Kraken, Bybit, and Gate all list — covering individual US stocks, ETFs, and tokenized funds. It launched with 60 tickers in mid-2025, runs about 100 now, and targets more than 500 by the end of 2026. It already counts over 80,000 holders, roughly $225 million in assets, and more than $3.5 billion in on-chain volume. The one rival of real size is Ondo, which by RWA.xyz's May 2026 figures held about 62% of tokenized-stock value ($1.0 billion) against Backed's 27% ($442 million). Robinhood went its own way, launching tokenized stocks on a proprietary chain in 2025, and eToro and KuCoin run their own offerings. Most of this activity lives on Solana, picked for cheap, fast settlement. These are the real-world examples that actually have volume behind them, rather than press releases.

Why tokenized stock adoption is accelerating

So why now, when Binance tried tokenized stocks in 2021 and walked away? Two things changed: the money and the rules.

The money is institutional. Total tokenized real-world assets reached roughly $19.3 billion by the first quarter of 2026, according to research flagged by Crowdfund Insider, and the wider forecasts are loud. HSBC analysts have floated a tokenized market worth $24 trillion by 2027, and BlackRock's chief executive has called tokenization "the next generation for markets." When the largest asset manager on earth says that out loud, exchanges listen. The adoption of tokenized equity stopped being a fringe experiment and became a product roadmap.

The rules moved too, just unevenly. Europe's framework gave issuers a place to operate legally, which is why Backed, Kraken, and Bybit built there first. Deeper liquidity followed the clarity: once a few venues shared the same Backed-issued tokens, order books thickened and spreads tightened on the popular names. That is the quiet flywheel behind the headline volume numbers. Clarity brings issuers, issuers bring liquidity, and liquidity brings the next wave of users. The same tokenization rails can carry private equity, bonds, and real estate too, which is why issuers treat equities as just the first market rather than the whole prize.

The upside: fractional ownership and liquidity

The honest case for tokenized stocks is access and composability, not price. Spreads can be worse than a discount broker's.

Trading does not stop at the closing bell. Where a US exchange runs from 9:30 to 4:00, these tokens trade around the clock on weekdays, and fractional ownership puts expensive names within reach — a slice of Apple above $180, or a sliver of Berkshire Hathaway, which trades north of $400,000 for a full share. Settlement is near-instant. And because the token is a blockchain-based digital asset, you can do things a paper share cannot: post it as DeFi collateral, earn yield on it, move it across borders without a local brokerage account. For someone shut out of US markets by geography, that last point is the entire pitch, not a marketing slogan. Liquidity, for the popular tickers at least, is now deep enough to matter.

The risks: dividends, custody and securities law

This is the part the brochures shrink to a footnote, and it is where I am not convinced for most people. You are taking on crypto risk in order to hold a stock. That can be the worst of both worlds.

Start with ownership, because you mostly do not have it. Hold a wrapped token and you are an unsecured creditor of the issuer. If that issuer or its custodian fails, you stand in line with everyone else, holding a claim rather than a share. Counterparty risk is not abstract in this industry. WOO X lost about $14 million to a Lazarus Group social-engineering attack in July 2025, and a 2023 incident tied to Kronos Research drained $22-25 million from the same network. Those are the kinds of intermediaries standing between you and your "stock."

Then the missing rights. Dividends are often absent or only loosely reflected, and voting is usually gone. Regulation is the bigger cloud. The SEC's January 2026 guidance was blunt: wrapping a share in a token does not change the fact that it is a security under federal law. In May 2026 the agency shelved a proposed tokenized-stock exemption indefinitely, which is why issuers crowd into friendlier European rules instead. These are securities, not a loophole around securities, and the laws and regulations governing them are still being written; local laws differ sharply from one country to the next. Liquidity also thins outside peak hours, so tokenized securities can drift in price from the real share while the underlying market is closed. And tax does not get easier — selling one is still a taxable disposal, the same as selling other cryptocurrencies. Security token offerings learned these lessons the slow way years ago.

Are tokenized stocks worth it for you?

For the right person, yes. If your local market locks you out, if you live inside DeFi, or if you need to trade at 2 a.m., a tokenized stock solves a real problem. For nearly everyone else with normal brokerage access, the math is harder: you give up ownership, dividends, and investor protection to gain convenience you may rarely use. So the question worth asking before you buy is not whether you can get exposure to Tesla on-chain. You clearly can. It is what you are giving up to get it, and whether that trade fits how you actually invest.