South Korea Crypto Tax 2026: Rate, Rules & Delays

South Korea passed a law to tax crypto profits in 2020. Six years later, it has not collected a single won on individual gains. The tax exists on paper, fully drafted, with a rate and a threshold and a filing form waiting in a drawer. It has just never been switched on.

That is the strange heart of any honest Korea crypto tax guide. The interesting question is not "what is the rate" but "will it ever actually take effect." The plan has been delayed four times. The latest start date is January 2027, and even that is now under fresh attack from a public petition and an opposition bill to scrap the whole thing. This guide explains what the tax would do, why it keeps slipping, and whether 2027 is real.

The crypto tax South Korea keeps not passing

Start with the timeline, because it tells the whole story. The legal framework was approved back in 2020. Since then, the start date has been pushed back again and again, each time landing just far enough away to be someone else's problem.

| Planned start | Outcome |

|---|---|

| 2022 | Postponed (reporting systems not ready) |

| 2023 | Postponed (industry opposition) |

| 2025 | Postponed (two-year deferral approved late 2024) |

| January 2027 | Current target; grace period ends Dec 31, 2026 |

Notice the pattern. Every deadline arrives, the infrastructure or the politics is not ready, and the can gets kicked down the road. Under Korean law the tax is filed as "other income" under the Income Tax Act, not as a capital gains tax in the Western sense. That distinction is not cosmetic. It shapes how losses and deductions are handled, and Korean lawmakers have spent years arguing over the details — including whether traders can carry losses forward at all, a protection stock investors take for granted. So far the debate has been academic, because the practical reality is simple: as of 2026, an individual in South Korea pays no tax on crypto trading gains. None. The law is real, the enforcement date is not.

How Korea's crypto tax would work: the 22% rate

When and if the tax finally lands, the mechanics are straightforward. Profits above an annual threshold are taxed at a flat rate. There is no progressive ladder like income tax, and no long-term discount like Australia or the United States offer.

| Component | Detail |

|---|---|

| National rate | 20% |

| Local surtax | 2% |

| Combined rate | 22% flat |

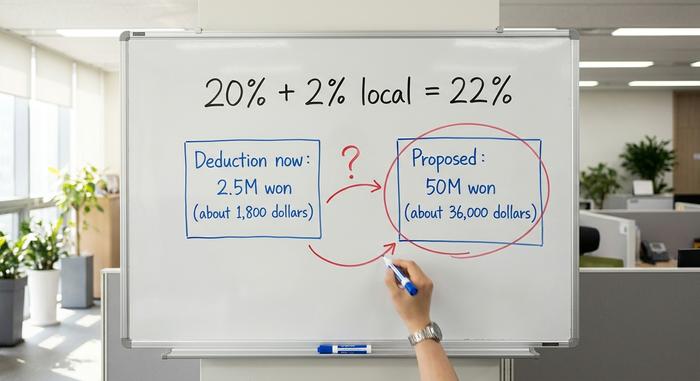

| Basic deduction | KRW 2.5 million (~$1,800) per year |

| Proposed deduction | KRW 50 million (~$36,000), for stock parity |

| First filing | May 2028 (for 2027 income) |

The headline is the 22% flat rate, but the real fight is over that threshold. The original deduction is a meager KRW 2.5 million, around $1,800, above which every won of profit is taxable. The Democratic Party has pushed to raise it to KRW 50 million, roughly $36,000, to bring crypto in line with the generous exemption Korean stock investors enjoy. That gap, between $1,800 and $36,000, is where most of the political energy sits.

A quick example shows how light the planned tax really is on small holders. Imagine a trader who books a KRW 10 million gain in a year, roughly $7,200. The first KRW 2.5 million is deducted, leaving KRW 7.5 million taxable, and 22% of that is about KRW 1.65 million, or near $1,200. Raise the deduction to KRW 50 million as the Democratic Party wants, and that same trader would owe nothing at all.

The fairness argument cuts both ways. The Finance Ministry has defended the 22% rate as fair. Its income tax official, Moon Kyung-ho, notes that taxation already falls unevenly across financial assets, and that a flat rate can actually beat a progressive one for high earners. Critics counter that retail stock investors pay nothing on most gains, so taxing crypto traders looks like singling them out — and some warn of double taxation, since assets can already attract other levies. Foreign investors face their own rule: a withholding of 11% of the sale price or 22% of the net gain, whichever is lower.

Which crypto transactions would be taxed

Under the South Korea crypto tax framework, the net would be wide. Selling crypto for won, swapping one coin for another, and spending crypto would all count as disposals once the rules switch on.

Earned crypto gets pulled in too. Mining rewards, staking income, and airdrops would be treated as "other income" at their fair market value on the day you receive them. The KRW 2.5 million annual deduction applies first, so small holders would likely owe nothing, while active traders above the line would feel it. The calculation itself, acquisition cost subtracted from sale proceeds, is the same arithmetic any tax system uses.

Why Korea's crypto tax keeps getting delayed

Four delays in a row are not bad luck. They are arithmetic. South Korea has roughly 16.29 million crypto accounts, equal to about 32% of the entire population. That is not a fringe hobby; it is a voting bloc, and a young, motivated one. No party wants to be the one that taxed it first.

So both sides have spent years courting crypto holders rather than taxing them. The Democratic Party's position has been to ease the tax, lifting the deduction to KRW 50 million rather than scrapping it. The People Power Party went further and introduced a bill to abolish the tax outright, citing fairness and the practical difficulty of enforcement. Then the politics shifted again: Lee Jae-myung won the presidency in June 2025 on an openly pro-crypto platform that included spot crypto ETFs and a won-backed stablecoin. With his party also holding sway in the Assembly, the government that is supposed to flip the tax on is led by the man who campaigned hardest on crypto-friendly policy — an awkward position for a "proceed as scheduled" stance.

The pressure has not let up. In May 2026, a public petition calling to scrap the tax gathered 50,000 signatures in eight days, which under Assembly rules forces a mandatory legislative review. The Finance Ministry has held its line, insisting the tax will proceed as scheduled and that abolishing the separate stock tax created no obligation to exempt crypto. But the underlying problems that drove the earlier delays have not vanished. Exchanges still struggle to produce clean cost-basis records across platforms, and tracking gains on overseas and decentralized venues remains genuinely hard. The delays were never purely cynical. Some of the infrastructure simply was not ready.

Will the 2027 crypto tax actually happen?

Here is the honest answer: nobody knows, and the base rate points to another slip. The Finance Ministry says the grace period ends on December 31, 2026, and that taxation begins the next day, full stop. On paper, 2027 is locked.

But paper has been wrong four times already. A fresh abolition bill sits in the Assembly, a 50,000-signature petition has forced a review, and a president who campaigned on crypto friendliness now leads the government. Pull those threads together and a clean January 2027 launch starts to look optimistic. My read is that another postponement, or a sharp rise in the threshold to soften the blow, is more likely than the tax landing exactly as written. I would not plan my finances around 2027 being final, in either direction. The practical takeaway for a Korean investor is to keep clean records now and assume the rules could either bite at KRW 2.5 million or barely touch you at KRW 50 million, because both outcomes are still live and the difference is thousands of dollars.

The market behind the fight: Korea's crypto scale

To understand why the Korea crypto tax debate is so radioactive, look at the size of the market. Korea is a crypto superpower that punches far above its economic weight.

The headline figure of 16.29 million accounts overstates active participation a little, since the regulator's verified-user count sat closer to 10.77 million in the first half of 2025, but either number describes a market that touches a huge share of adults. The won was the second most-traded fiat currency in crypto in 2025, with about $663 billion in volume, behind only the US dollar. Local trading runs so hot that Korean prices often sit above global ones. Traders call it the "kimchi premium." The same Bitcoin can cost noticeably more in Seoul than in New York, simply because local demand outstrips easy supply. At the same time, capital is leaking out: Koreans sent an estimated $110 billion to overseas exchanges in 2025, partly to sidestep domestic friction. The government has leaned into the upside too, with a won-pegged stablecoin framework advancing in 2025 as part of the new administration's digital-asset push.

Regulation has been catching up fast. The Virtual Asset User Protection Act took effect in July 2024, forcing exchanges to hold most customer funds in cold storage and banning market manipulation. Through 2025, the long-standing ban on institutional crypto accounts was gradually lifted, opening the door to nonprofits, listed companies, and professional investors.

How South Korea will track crypto gains

Here is the part investors underrate: there may be no tax yet, but the machine to collect it is already running. The National Tax Service has built real-time monitoring that plugs directly into the major exchanges.

Upbit, Bithumb, and Korbit share transaction data with the authorities, a requirement reinforced by the Virtual Asset User Protection Act. The reach is expanding outward, too. South Korea is set to exchange data with other countries under the OECD's Crypto-Asset Reporting Framework from 2027, which would expose the overseas holdings that Koreans have used to stay out of view — estimated at $99 billion as far back as 2023. In 2026, tax officials began folding crypto holdings into property-deal checks to catch evasion, treating undisclosed coins as a hidden source of funds. Crypto is also already pulled into Korea's gift and inheritance tax, valued at market price when it changes hands, so the "no tax yet" rule applies only to trading gains, not to every transfer. Investors are expected to keep acquisition and transaction records for at least five years. The lesson is blunt: the surveillance does not wait for the tax.

South Korea crypto tax vs other countries

Step back, and the planned 22% looks mid-pack rather than punitive. Korea is neither a haven nor a Japan-style high-tax outlier.

| Country | Crypto tax on gains |

|---|---|

| Singapore | 0% (no capital gains tax) |

| Germany | 0% if held over 1 year |

| South Korea | 22% planned (not yet in force) |

| United States | Long-term capital gains 0/15/20% |

| Japan | Up to 55%, reform to ~20% |

A flat 22% above a real threshold would put Korea roughly alongside the United States and well below Japan's current ceiling. The catch, of course, is that every other rate in that table is actually being collected today. Korea's is the only one still sitting in a drawer.

The bottom line on Korea crypto tax

The headline number is 22%, but the real story is a tax that has been one year away for half a decade. The framework is drafted, the surveillance is live, and the political will to flip the switch keeps evaporating at the last minute.

So do not confuse "no tax yet" with "no tax ever." The records are already being kept, the data-sharing deals are already signed, and a flat 22% above KRW 2.5 million is what waits if the 2027 date finally holds. Whether it holds is a political question, not a technical one. Watch the threshold debate and the Assembly review, not the calendar, because in Korea the calendar has been wrong four times running. For now, the safest assumption is that South Korea's crypto tax is coming eventually, in some form, and that your trading history will be on file long before the first bill ever arrives.