Crypto Tax in Italy: The 2026 Guide to What You Owe

Italy spent the end of 2024 trying to nearly double the tax on crypto gains. The proposal floated a 42% rate. It did not survive parliament intact, but what came out the other side is still stricter than most guides online will tell you. The flat rate climbed, a long-standing exemption disappeared, and the tax authority now gets your trading data whether you file or not.

So the crypto tax in Italy looks different in 2026 than it did even a year ago. If you hold, trade, or earn cryptocurrency and you are tax-resident in Italy, the number that matters has moved twice in two tax years, and the old "small investor is safe" assumption is no longer true. Here is what is actually owed, who owes it, and where the real planning room is.

How crypto is taxed in Italy in 2026

The headline most coverage gets wrong: the flat rate is no longer 26%, and there is no longer a small-gains free pass. Both changes came from the same law, Law 207/2024, the 2025 Budget Law published in the Gazzetta Ufficiale on the last day of 2024. Read that one statute and most of the confusion clears up.

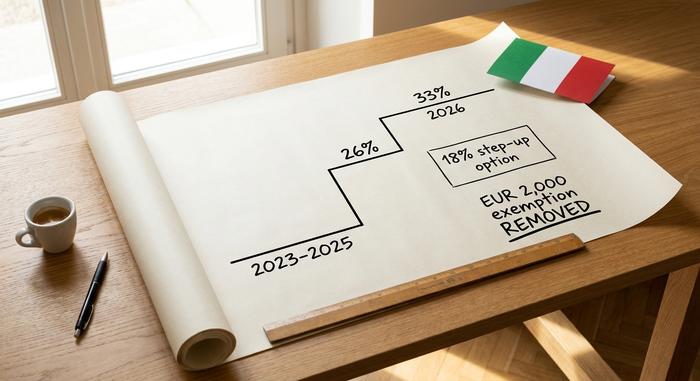

From 26% to 33%: the capital gains tax rate

For the 2023, 2024, and 2025 tax years, crypto capital gains were taxed at a flat 26% substitute tax, the same rate Italy applies to most financial investments. From 1 January 2026, that rate rises to 33%. The original draft asked for 42%; industry pushback and a parliamentary negotiation pulled it down, but not back to where it started.

Practically, this means gains you realized in 2025 still fall under the 26% rate when you file in 2026, while gains realized from 2026 onward carry the 33% rate. The capital gains tax rate is flat, not progressive, so it does not stack with your income tax bracket. It is a substitute tax — one rate, applied to the net gain, instead of folding crypto into ordinary income.

| Tax year | Crypto capital gains rate | Legal basis |

|---|---|---|

| 2023-2025 | 26% flat substitute tax | Law 197/2022 |

| 2026 onward | 33% flat substitute tax | Law 207/2024 |

| 2025 only (optional) | 18% step-up on portfolio value | Law 207/2024, co.26-27 |

The €2,000 exemption is gone

Until the end of 2024, the first €2,000 of annual crypto gains were tax-free. That threshold is abolished from 1 January 2025. Now every euro of gain is taxable, even one. The exemption still applies to gains from earlier tax years, so it is not retroactive, but going forward there is no buffer. For a country where, by Politecnico di Milano's 2024 figures, about 85% of the roughly 2.7 million crypto holders own less than €5,000 of assets, removing that floor touches far more people than the rate change does.

Taxable vs tax-free crypto transactions

Not every move is a taxable event. Selling crypto for euros is. So is spending it on goods or services, and, in most cases, swapping one cryptocurrency for another. The one nuance worth knowing: a crypto-to-crypto swap is only tax-free when the two assets share the "same characteristics and functions," per the Agenzia delle Entrate's Circular 30/E of October 2023. Trading Bitcoin for Ether is not a taxable disposal under that reading; converting crypto into an e-money token can be. Buying crypto with fiat, holding it, and moving it between your own wallets are all free.

Capital gains and losses with the LIFO method

Here is a detail that quietly raises most people's Italy crypto tax bill: Italy defaults to LIFO, last-in-first-out, not the FIFO that many investors assume. When you sell, the tax authority treats your most recently acquired coins as the ones sold first. In a rising market, the recent coins usually have a higher cost basis, which means a smaller paper gain per sale, but the method can cut either way depending on when you bought.

A quick example. You buy 1 ETH at €1,500 in January and another at €2,500 in June, then sell one ETH for €2,800. Under LIFO the June coin goes first, so your capital gain or loss is €300, not the €1,300 you would show if the January coin counted. Keep the dates and prices; the gain depends entirely on them.

Crypto losses are usable, but only against gains, and only carried forward for a limited window, generally up to four to five years depending on how your sources read the rule. With the €2,000 floor gone, there is no longer a small cushion to absorb minor losses automatically, so tracking gains and losses across the full year matters more than it used to.

The 18% flat tax step-up for your crypto portfolio

This is the lever the rate-panic headlines buried. Alongside raising the rate, Law 207/2024 offered a step-up option, the affrancamento, sometimes called the alternative portfolio tax: you can reset the cost basis of your crypto portfolio to its fair-market value on 1 January and pay a one-time 18% substitute tax on that value, instead of carrying a low basis into a future sale taxed at 33%.

For a long-held bag sitting deep in profit, the math can favor paying 18% now over 33% later on a much larger gain. For a portfolio near break-even, it rarely helps. The 2025 window set a payment deadline of 30 November 2025, payable in one shot or three instalments with 3% annual interest. Italy has re-offered versions of this step-up across successive budgets, so check whether a current-year window is open before assuming the door is shut. It is the one move genuinely worth modelling with real numbers.

Wealth tax on your crypto in Italy

Even if you never sell, holding crypto in Italy triggers a yearly bill, and this is the part casual holders miss entirely. A 0.2% annual levy applies to the value of your crypto assets, assessed on the figure at 31 December. When your crypto sits with an Italian intermediary, it shows up as imposta di bollo, a stamp duty deducted for you. When you hold abroad or in self-custody, the equivalent wealth tax falls on you to calculate and pay, with a minimum charge in some cases.

It is a small percentage, but it is a tax on holding, not on profit. A €50,000 portfolio that did nothing all year still owes about €100. The Agenzia delle Entrate confirmed the mechanics in its Risposta 181/2024 ruling, which is worth knowing because the naming across guides is inconsistent and the obligation is easy to overlook.

Income tax on crypto: staking and mining

Capital gains rules under crypto tax in Italy are clear. Income rules are not, and anyone telling you otherwise is overstating the current guidance. Staking rewards, crypto mining proceeds, and similar earnings do not slot neatly into the 26/33% substitute tax, and the Agenzia delle Entrate has not published detailed, crypto-specific rules for all of them.

The cautious read, and the one most advisers take, is that this income from crypto is taxed as personal income under IRPEF when received, then subject to capital gains rules again when later sold. IRPEF, the personal income tax, is progressive: roughly 23% up to €28,000, 35% to €60,000, and 43% above that, plus local surcharges. Airdrops and hard forks are generally treated as taxable on disposal rather than receipt. DeFi is greyer still: lending interest and liquidity-pool fees probably count as income, but the Agenzia delle Entrate has not spelled out the timing, so two careful accountants can reach different answers on the same wallet. I am not convinced the current guidance is settled enough to bank on a single answer for staking, so if a meaningful share of your activity is income rather than trading, this is the part to take to a tax professional.

How to report and file crypto taxes in Italy

The mechanics trip people up more than the rates do. The single most common mistake is assuming that no gain means no filing. In Italy, you declare your holdings even when you made nothing, and the form you pick changes what you can report.

Which tax forms you need (Redditi PF, RW, RT)

Most crypto investors file their tax return on the Modello Redditi PF. Inside it, Quadro RW declares your holdings, including foreign and self-custodied assets, and Section RT reports your capital gains. The simpler Modello 730 suits straightforward employment income but does not handle the full crypto picture, so active traders usually need the Redditi PF.

Deadlines and how to pay

Deadlines shift slightly year to year and sources disagree on the exact date, so treat these as a guide and confirm against the Agenzia delle Entrate calendar. The Modello 730 generally falls due around the end of September; the Modello Redditi PF lands in mid-to-late October. Tax due is paid through the F24 form. The wealth-tax payment and any step-up instalments follow their own dates.

Penalties for not declaring

This is where it gets expensive. Failing to declare holdings in Quadro RW carries a penalty of roughly 3% to 15% of the undeclared asset value, per year, with a reduced flat charge of around €258 if you correct the omission within 90 days. And there is a trap in the cost basis: if you cannot prove what you paid, the tax authority can default your basis to zero, which makes your entire sale a taxable gain. Records are not optional.

| Form | What it reports | Rough deadline |

|---|---|---|

| Modello 730 | Simple income, employees | End of September |

| Modello Redditi PF | Crypto gains + holdings | Mid-to-late October |

| Quadro RW (in Redditi PF) | Holdings, incl. foreign/self-custody | With Redditi PF |

| Section RT (in Redditi PF) | Capital gains and losses | With Redditi PF |

DAC8: reporting crypto transactions in 2026

Here is what almost no guide mentions, and it changes the whole calculus. From 1 January 2026, the EU's DAC8 rules require crypto service providers to collect and report data on their Italian users straight to the Italian tax authority. Italy transposed the directive through D.Lgs. 194/2025. The first cross-border data exchange is due by 30 September 2027, and providers that fail to comply face penalties between €1,500 and €15,000.

What this means in plain terms: the exchanges already have your name, and soon the Agenzia delle Entrate will too. Sitting on undeclared crypto transactions and hoping nobody notices stops being a strategy. Combined with MiCA and the global CARF framework, the information gap that made non-declaration survivable is closing fast. Voluntary compliance has gone from optional to the only sensible plan.

Crypto in Italy vs the rest of the EU

For context, under Italian tax law the 33% rate puts Italy in the mid-to-high band of EU crypto tax, not at either extreme. Germany and Portugal exempt long-held crypto entirely after a year. France runs a 30% flat tax; Spain uses progressive rates from 19% to 30%. So Italy is now pricier than the long-hold havens and roughly level with its large neighbours. The gap that matters most is with Germany: a coin held a year and a day is taxed at 33% in Milan and at nothing in Munich. That is the kind of difference that tempts people to move, and it is a reason to plan carefully rather than to pack a bag without advice; residency moves carry their own tax implications that dwarf a few points of rate.

What crypto tax in Italy means for you

The two changes that define crypto tax in Italy today are simple. The €2,000 hiding spot is gone, so small holders now have real tax liabilities, and DAC8 removes the option of staying invisible. Against that, the one genuinely useful move for long-term crypto investors is the 18% step-up, modelled with your actual numbers, ideally with a tax advisor, before you ever sell. Everything else is record-keeping and meeting a deadline. Which raises the only question that really matters before your next sale: are your cost-basis records good enough to survive a zero-basis default?