Netherlands Crypto Tax: How Box 3 Really Works in 2026

Most countries tax the profit you make on crypto. The Netherlands does something stranger. It largely ignores your actual gains and instead taxes a number the government imagines your assets earned. Sell Bitcoin for a 300% profit and a Dutch resident may owe nothing on that profit directly. Watch your portfolio fall all year and you can still get a tax bill. This is the logic of the Netherlands crypto tax, and once you see how it works, the rest of the Dutch system stops looking random.

This guide walks through the machine. Why crypto lands in Box 3 rather than Box 1, how the deemed return and the 36% rate actually pencil out, why the Supreme Court keeps striking the whole thing down, and the line that flips you into far harsher income tax. Roughly 10% of Dutch adults hold crypto, around 1.5 million people, according to AFM-commissioned research, so this is not a niche problem.

Why Dutch crypto sits in Box 3, not Box 1

Almost every strange thing about Dutch crypto tax comes from a single classification call. The tax office treats your crypto as wealth you hold, not income you earned. Get that one idea and the rest follows.

The three boxes in one minute

Dutch income tax is split into three boxes. Box 1 covers income from work and your own home, taxed at progressive rates. Box 2 covers profits from a substantial shareholding in a company. Box 3 is the one that matters here: it covers savings and investments, the wealth you are simply sitting on. Each box has its own rules and its own rate, and an asset lives in exactly one of them.

Crypto counts as an "other asset"

The Belastingdienst, the Dutch tax authority, places cryptocurrency in Box 3 as an investment, in the same broad bucket as shares, a second property, or a savings account. For most people, this is good news. There is no separate capital gains tax on crypto in the Netherlands. You are not taxed when you sell, swap, or spend a coin. The taxable event is simply owning the asset on one specific day.

The 1 January snapshot that decides your bill

That day is 1 January. The value of your entire crypto holding at the start of the tax year, converted to euros at the exchange rate on that date, is what counts. It does not matter what happens afterward. A holder who owned 100,000 euros of crypto on 1 January and watched it crash to 20,000 by March is still taxed on the January figure. This snapshot, called the peildatum, covers crypto on exchanges and in self-custody wallets alike. The tax office does not care where the keys are.

How the deemed return and 36% tax rate work

Here is where the system earns its reputation. The Netherlands does not ask what your crypto actually did. It assumes a return, taxes that assumption, and moves on. The gap between the assumed return and your real one is the source of nearly every complaint, and a decade of litigation.

The deemed-return percentages

The state sets a fictitious yield each year for each asset category. Crypto falls into the "investments and other assets" group, which carries by far the highest assumed return. For 2025 that deemed return is 5.88%, and for 2026 it rises to 6.00%, according to the Belastingdienst (as of 2026). On top of that notional gain sits a flat tax rate of 36%.

| Asset category | Deemed return 2025 | Deemed return 2026 |

|---|---|---|

| Bank and savings balances | 1.37% | 1.28% (provisional) |

| Investments and other assets (incl. crypto) | 5.88% | 6.00% |

| Debts | 2.70% | 2.70% |

| Flat tax rate on the deemed return | 36% | 36% |

| Tax-free allowance per person | €57,684 | €59,357 |

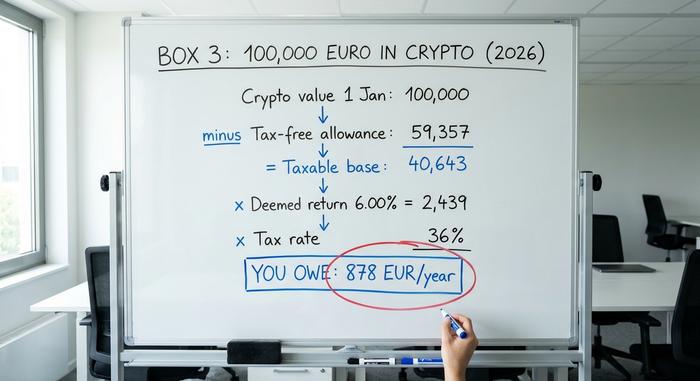

A worked example on €100,000 of crypto

Say you are a single Dutch resident holding 100,000 euros of crypto on 1 January 2026, and nothing else in Box 3. First, subtract the tax-free allowance of 59,357 euros, which leaves a taxable base of 40,643 euros. Apply the 6.00% deemed return and you get an assumed gain of about 2,439 euros. Tax that at 36% and you owe roughly 878 euros for the year.

The headline number to remember is this: every euro above the allowance is effectively taxed at 6.00% times 36%, or about 2.16% of its value, every single year. Whether your crypto doubled, halved, or sat untouched changes nothing.

The tax-free allowance

That allowance does real work. In 2026 it shields 59,357 euros per person, and fiscal partners can combine theirs to 118,714 euros. For a couple, that means a sizeable crypto stack can sit largely below the line. The flip side is harsh for big holders: once you clear the allowance comfortably, the deemed return assumes a fat 6% gain in years when your portfolio may have produced nothing at all.

The court rulings that broke Box 3

This is the part the slick tax guides skim over, and I think it is the most important thing to understand about Dutch crypto tax. The system is running on borrowed time. The Hoge Raad, the Dutch Supreme Court, has ruled the fictitious-return model unlawful not once but twice, and that is exactly why a workaround now exists for anyone whose real return came in lower than the fiction.

The 2021 Christmas ruling

On 24 December 2021, in a decision now known as the Kerstarrest, the Supreme Court found that taxing people on an assumed return breached their rights under the European Convention on Human Rights, specifically the right to peaceful enjoyment of possessions and the ban on discrimination. Taxing a fiction, the court held, unfairly burdens people whose actual return is lower than the state's guess. Parliament scrambled to patch the law.

The June 2024 follow-up

The patch did not hold. On 6 June 2024, the Hoge Raad ruled in a cluster of cases that both the temporary Restoration Act and the Bridging Act that replaced it still violated the same Convention rights whenever the deemed return exceeded the real one. The remedy it ordered is the one that matters to you: where your actual return is demonstrably lower, the tax must be reduced so only that real return is taxed.

Electing your actual return, and its catch

Since 2025, the option to declare your actual return sits inside the annual income tax return itself, rather than on a separate form. If your crypto genuinely underperformed the assumed 6%, you can elect to be taxed on what you really made. It is not a free pass, though. Choose this route and the tax-free allowance falls away, unrealised gains count toward your return, and there is no negative floor, so a losing year cannot create a deductible loss to carry forward. For many holders it still beats the fiction. Run both numbers before you choose.

When crypto becomes Box 1 income tax

Now the dangerous grey zone of Netherlands crypto tax. Everything above assumes you are an ordinary investor holding assets. Cross a fuzzy line into active, business-like behaviour and your crypto leaves Box 3 entirely for Box 1, where progressive income tax reaches 49.50% in 2026. That is not a small jump from an effective 2.16%.

What pushes you across? The legal test is whether you do "more than normal asset management", what the Dutch call extra arbeid, extra labour. Day trading with systematic profit intent, mining where your income outstrips your costs, using special tools or foreknowledge, or being paid a salary in crypto can all land income in Box 1, taxed under categories like "result from other activities" or "profit from enterprise". The honest catch is that there is no official number. The Belastingdienst publishes no threshold of hours or euros that draws the line; Dutch courts decide it case by case, weighing effort, intent, and expertise. If you are running anything that smells like a trading business, get advice before you file.

How to report crypto to the Belastingdienst

In practice, Netherlands crypto tax compliance is simpler than the theory suggests. You report crypto once a year, as part of your regular income tax return, during the filing window that runs from 1 March to 1 May through the Mijn Belastingdienst portal.

The work is mostly valuation. Take every coin you held at 00:00 on 1 January, convert it to euros at that moment's exchange rate, and add it to your Box 3 total alongside any other savings and investments. Include holdings on exchanges and in private wallets; the location of the asset does not change its treatment. Keep your own records, because the burden of proof sits with you, especially if you elect the actual-return route. Failing to declare crypto is not a clever strategy. Penalties for undisclosed assets are steep, and the days of the tax office not knowing are ending.

DAC8: crypto tax reporting changes in 2026

For years, a quiet truth shaped Dutch crypto tax behaviour: the authorities often could not see what they could not be told. That era is closing. The European Union's DAC8 directive, adopted on 17 October 2023, forces crypto platforms to report their users' activity to tax authorities across the bloc, and the Netherlands has now written it into law.

The Dutch implementing rules took effect on 10 April 2026, retroactive to 1 January 2026, making 2026 the first reporting year. Crypto-asset service providers, meaning the exchanges and brokers most people use, must collect data on their Dutch customers and hand it to the Belastingdienst by 30 September 2027. After that, "they can't see my wallet" stops being a plan. The reporting gap that ran through the entire Box 3 era is being stitched shut, and the smart move is to assume your numbers are already visible.

What the 2028 real-return crypto tax brings

The permanent fix for the Dutch crypto tax system keeps slipping. After the court losses, the government committed to scrapping the fiction and taxing real returns through a new law, the Wet werkelijk rendement box 3. It was first aimed at 2026, then 2027, and is now penciled in for 1 January 2028, with the delay blamed on the tax authority's IT overhaul and a need for hundreds of extra staff. The lower house of parliament passed the bill on 12 February 2026; approval by the upper house was still pending as this was written, so the date is not yet locked. When it lands, it will tax actual gains, including some unrealised ones, which reshapes the calculus for buy-and-hold investors versus active traders.

Netherlands crypto tax vs nearby countries

A quick reality check on whether the Dutch model is a good deal. It rewards long-term holders sitting on large unrealised gains, since those gains are never taxed directly, but it punishes anyone parking a big idle balance through a flat yearly levy. Neighbouring countries lean the other way, taxing the gain when you sell, which is broadly how Germany, Belgium, and Portugal handle it.

| Country | Model | Headline treatment for individuals |

|---|---|---|

| Netherlands | Wealth tax (Box 3) | ~2.16% of holdings per year above the allowance; no tax on the gain itself |

| Germany | Capital gains | 0% if held over one year; otherwise taxed as income |

| Belgium | Capital gains | New tax of around 10% on financial gains from 2026 |

| Portugal | Capital gains | 28% on gains held under a year; 0% if held longer |

Treat these as general rules for private investors, not personal advice; each country has conditions that can change the outcome.

The bottom line on Dutch crypto tax

Until 2028, the Netherlands crypto tax remains a tax on a fiction. You owe tax on a return the state assumes you made, calculated from a single January snapshot, regardless of what your crypto actually did. The two things worth acting on are simple. First, if your real return was lower than the assumed 6%, you can now demand to be taxed on reality instead, so run the comparison before you file. Second, DAC8 means the tax office will soon have your transaction data whether you volunteer it or not. So here is the question to sit with: if the rules are about to tax what you genuinely earned, and the authorities are about to see exactly what that is, why would you plan around the old assumption that no one is looking?