Singapore Crypto Tax 2026: A Tax-Free Crypto Guide

Singapore's reputation as a tax-free home for crypto is real, but it comes with a condition most guides skip right past. You can buy Bitcoin, hold it for years, sell it at a profit, and owe nothing. The moment your activity starts to look like a business, though, the same gains become taxable income. The whole question of Singapore crypto tax turns on which side of that line you sit.

This guide explains what is genuinely free, what is not, and how crypto taxation in Singapore actually works once the Inland Revenue Authority of Singapore gets involved. The rules are clear in outline and grey at the edges, so knowing where the edges are matters more than memorizing a rate.

How crypto is taxed in Singapore

The headline gets repeated everywhere: Singapore has no capital gains tax on crypto — and it is the first thing most people look up when researching crypto tax in Singapore. That is true. It is also widely misunderstood. There is no crypto-specific exemption written into the law. Singapore simply does not levy a capital gains tax on anything, so personal investment gains on tokens fall outside the tax net the same way gains on shares do.

No capital gains tax on crypto

For an individual holding crypto as a personal investment, a profit on sale is not taxed. The rate is zero. This follows from general tax principles, set out in the IRAS e-Tax Guide on the income tax treatment of digital tokens, rather than from any special concession for cryptocurrency. The practical effect is the same: a long-term holder who buys and holds before selling crypto keeps the gain.

GST and digital payment tokens

The other tax people ask about is GST. Since 1 January 2020, the supply of digital payment tokens, the category that covers Bitcoin and similar tokens, has been exempt from goods and services tax. You do not pay GST for swapping or using a payment token itself. You do still pay GST, currently 9% since 2024, on the goods or services you buy, whether you pay in dollars or in crypto. The exemption is on the token, not on your shopping.

Three kinds of token

IRAS does not treat every token the same. Its guidance splits digital tokens into three types, and the type shapes the tax. Payment tokens, like Bitcoin, are the ones the no-capital-gains rule and the GST exemption cover. Utility tokens give access to a service and are usually treated as prepayments. Security tokens behave like financial instruments, so any return on them, such as a dividend-style distribution, can be taxable income. Most retail holders only ever deal with payment tokens, but knowing the categories explains why two tokens can be taxed differently.

When crypto stops being tax-free

Here is the part the rate alone never tells you. The zero applies to investment. It does not apply to income. If your crypto activities are judged to be a trade or a business, the profits become taxable income, and the difference between those two labels is where almost every real Singapore crypto tax question actually lives.

| Activity | Tax treatment |

|---|---|

| Buying and holding as investment | Not taxed (no capital gains tax) |

| Selling a long-term personal holding | Not taxed |

| Trading as a business | Taxed as income |

| Getting paid in crypto | Taxed as income at market value |

| Buying goods or services with crypto | 9% GST on the goods or services |

Investor or trader? The badges of trade

This is the question that decides your bill, and there is no simple test for it. IRAS does not count your trades and apply a threshold. Instead it weighs the whole picture against a set of factors known as the badges of trade, the same case-law principles courts use to separate an investor from someone running a business. Get classified as an investor and your gains are capital, untaxed. Get classified as a trader and they are income, taxed at up to 24%.

The five badges of trade

The factors IRAS and the courts look at include how often you transact and in what volume, how long you hold before selling, whether there is a clear profit-seeking motive, how the activity is financed, and whether you run it with the organization of a business, such as systems, tools, and record-keeping. No single badge is decisive. A frequent trader funding positions with borrowed money and watching screens all day looks very different from someone who bought once and held for three years.

What tips a holder into a trader

Patterns push you toward the trader side. Trading crypto daily, using leverage, dealing in high volume relative to your other income, and treating it as your main occupation all point to a trade. So does building infrastructure around it: dedicated capital, trading software, a deliberate strategy to profit from short-term moves. None of these alone makes you a trader, but together they paint a picture IRAS can act on.

Consider two people who each made S$50,000 on crypto last year. One bought Ether in 2022, held it, and sold once. The other placed hundreds of leveraged trades across the year, funded by a margin account, tracking the market full time. Same profit, very different tax outcome: the first keeps it as untaxed capital, the second is almost certainly trading and owes income tax on the lot.

Why there is no bright-line rule

People want a number, a holding period or a trade count that draws a clean line. It does not exist, by design. The badges of trade are applied case by case, on the facts, which gives IRAS flexibility and gives taxpayers uncertainty. The sensible response is to document your intent and behaviour: if you hold for the long term, your records should show it.

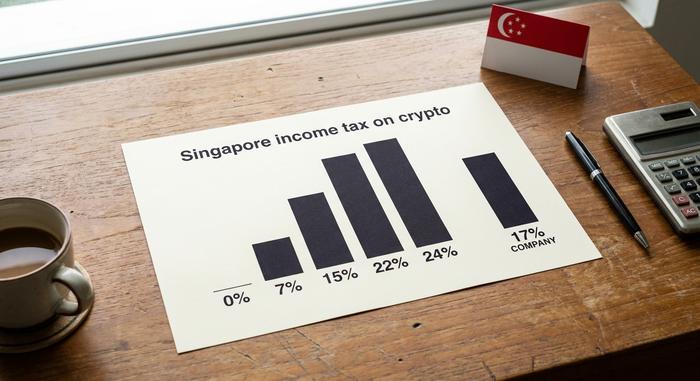

Crypto income tax rates in Singapore

Once crypto counts as income under Singapore's tax rules, the zero disappears and ordinary rates take over. For an individual, income tax is progressive: the first portion of income is taxed at 0%, and the rate climbs in bands to a top rate of 24% on income above one million Singapore dollars, a top rate that has applied since the 2024 assessment year. A company dealing in crypto is taxed at the flat corporate rate of 17%.

There is a second way crypto becomes income: getting paid in it. If you receive tokens as payment for work or in the course of business, that is taxable at the market value of the tokens on the day you receive them, the same as being paid in cash. A later rise or fall in the token's price is a separate matter.

| Taxable income (individual) | Rate |

|---|---|

| First S$20,000 | 0% |

| S$40,001 to S$80,000 | 7% (on the band) |

| S$320,001 and above (to S$1M) | up to 22% |

| Above S$1,000,000 | 24% |

| Company crypto profits | 17% flat |

Staking, mining, and airdrops in Singapore

This is the genuinely grey area of Singapore crypto tax, and honesty serves you better than false precision here. IRAS has not published a standalone guide on staking or DeFi, so the treatment is inferred from the same general principles that govern everything else: is this income, or is it not?

Mining or staking carried out in a systematic, business-like way produces taxable income. The same activity done occasionally, as a hobby, by an individual is generally treated as capital and left alone. DeFi lending and liquidity rewards follow the same logic: if they look like a recurring profit-seeking operation, expect them to be income. Airdrops sit slightly apart. When you receive an airdrop without rendering any service for it, it is usually not taxed at the point of receipt, though a later sale could be income if you are trading.

One figure worth ignoring is the oft-repeated claim that staking under a few hundred dollars is automatically tax-free. That threshold is not an IRAS crypto rule, and repeating it has misled a lot of readers. When the guidance is genuinely thin, the safe move is to ask whether the activity is business-like rather than to lean on a number nobody official has published.

How to report and file crypto taxes in Singapore

For most holders, the filing story is short: you made an investment gain, there is no capital gains schedule, and you report nothing on it. The mechanics only matter when some of your crypto is income.

If it is, you self-report it in your annual income tax return to IRAS, alongside other income, with the usual filing deadlines falling in mid-April, around 15 April for paper and 18 April for e-filing. There is no special crypto form; the income goes in as trade or business income. What protects you, for tax purposes, is the paperwork: keep the dates, the cost basis, the counterparties, and the Singapore-dollar value of each transaction. When IRAS asks how you arrived at a number, the records are the answer.

Businesses have an extra layer. A company dealing in crypto may need to register for GST once its taxable turnover crosses the registration threshold, even though the payment tokens themselves are exempt. And under-reporting carries a cost: IRAS can impose penalties on tax that should have been paid, so the gap between an honest mistake and an aggressive position is one you do not want to test. Self-assessment puts the burden of getting it right on you.

CARF and MAS: the rules tighten by 2028

The tax-free status is not an invisibility cloak, and this is the context almost no guide includes. Singapore has signed up to the OECD's Crypto-Asset Reporting Framework, putting its name to the multilateral agreement in November 2024, with the first automatic exchange of crypto account information confirmed for 2028. Platforms will report holder data, and that data will cross borders.

The Monetary Authority of Singapore has been tightening the platform rules in parallel. From October 2024, new Payment Services Act measures banned retail lending and staking by licensed providers and required customer assets to be held on statutory trust, and operators serving overseas from Singapore had to be licensed by mid-2025. None of this changes the no-capital-gains-tax position, but it does mean the runway for staying quiet is finite and dated.

Singapore's 2028 start date sits a year behind the EU and UK cohort, which begins reporting in 2027. That extra year buys time to get organized; it does not make the obligation disappear. The practical move is to treat 2028 as a deadline that is already here: reconcile your wallets, keep clean records, and make sure your tax position would survive someone else reporting the same numbers to IRAS.

Singapore vs other crypto tax free countries

Singapore is genuinely one of the better homes for crypto, and locals have noticed: by the Independent Reserve Cryptocurrency Index 2026, around 32% of Singaporeans held crypto that year. But the headline tax advantage is shared. The United Arab Emirates levies no personal income tax on crypto gains. Hong Kong, like Singapore, has no capital gains tax while taxing trading carried on as a business. The no-capital-gains edge is common to all three; the real difference between them is how each draws the investor-versus-trader line and how its regulator treats platforms. On that combination, Singapore tends to rank near the top of crypto-friendliness tables, helped by a clear framework rather than just a low rate. Before relocating for the tax, though, remember that residency rules and your home country's exit and reporting requirements usually matter far more than the headline rate.

What Singapore crypto tax means for you

The takeaway on Singapore crypto tax is simpler than the grey areas suggest. If you buy and hold crypto as a personal investment, you almost certainly owe nothing in Singapore. If you trade like a business or get paid in tokens, that is income and it is taxed, up to 24% for individuals or 17% for a company. And with CARF reporting arriving in 2028, the records you keep today are what will defend your position later. So the honest question to ask yourself before next tax season is the one IRAS would ask: looking at your last twelve months, are you an investor or a trader?