Australia Crypto Tax 2026: ATO Rules, Rates & CGT

The Australian Taxation Office does not see your Bitcoin as money. It sees property. That one view turns almost every move you make, every sale, every swap, every coffee bought with crypto, into a taxable event. It is the starting point for understanding Australia crypto tax, and most confusion traces back to people who never internalised it.

Two stories are testing that view right now. A court in 2025 called Bitcoin "money," sparking talk of a billion dollars in refunds. And the ATO is running a data-matching program that quietly collects records on more than a million people a year. One of those stories changes your taxes today. The other does not. This guide sorts out which is which.

How crypto is taxed in Australia by the ATO

Start here, because everything else follows from it. The ATO has treated crypto as a capital gains tax (CGT) asset since 2014 — property, for tax purposes, in the same broad category as shares or an investment property, not a currency and not money.

That classification does the heavy lifting. When you dispose of a CGT asset, you trigger a CGT event, and any gain gets added to your assessable income for the year. There is no separate, gentler "crypto tax rate" sitting off to the side. Your crypto gain is taxed at your ordinary marginal rate — the same scale that applies to your salary.

Why does the property-versus-currency question matter so much? Because it is the fork in the road. A country that treats Bitcoin as foreign currency taxes it under entirely different rules. Australia chose property, and that choice is precisely what the 2025 court ruling, which we will come to, pokes at. For now, property is the law, and property means CGT.

Two paths exist, and which one you are on matters enormously. Most people are investors: they buy and hold, and their gains fall under CGT, which unlocks a valuable discount we will get to shortly. A smaller group are traders, people running a business-like operation with frequency, system, and a profit-making intent. Traders do not get the CGT discount. Their profits are ordinary income, full stop, though they can deduct business expenses in return.

The ATO decides which camp you are in by looking at how you actually behave, not what you call yourself. Volume, organisation, record-keeping, and intent all feed the judgment. For the large majority reading this, investor treatment applies, and that is the lens for most of what follows.

How much crypto tax you pay: CGT and rates

Here is the part people get wrong: there is no flat crypto tax rate in Australia. Your gain is sliced into your income and taxed at whatever marginal bracket it lands in. So the same profit can cost one person 16 cents on the dollar and another 45.

Most residents also pay the 2% Medicare levy on top, which nudges the genuine top rate closer to 47%. These are the resident rates for the 2025-26 financial year, before that levy:

| Taxable income (AUD) | Tax rate |

|---|---|

| 0 - 18,200 | 0% |

| 18,201 - 45,000 | 16% |

| 45,001 - 135,000 | 30% |

| 135,001 - 190,000 | 37% |

| 190,001+ | 45% |

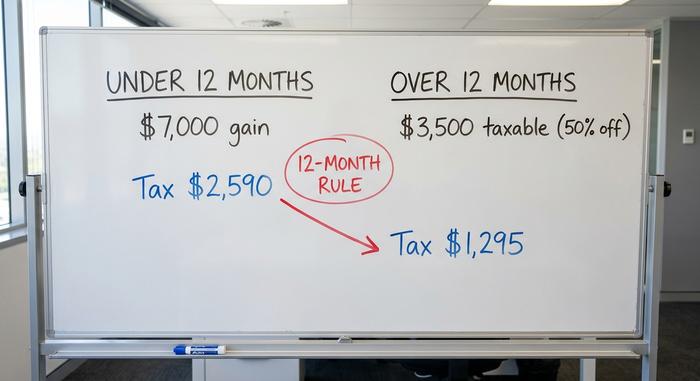

Now the lever that actually matters. Hold a crypto asset for more than 12 months before you dispose of it, and as an individual investor you qualify for the 50% CGT discount on long-term capital gains. Only half the gain is taxed. Self-managed super funds get a smaller one-third discount. This single rule, the 12-month line, is the most powerful tax decision most holders ever make, and it costs nothing but patience.

A quick worked example shows the gap. Say you earn $130,000, putting your top dollar in the 37% bracket, and you make a $7,000 gain on Ethereum.

| Holding period | Taxable gain | Tax at 37% |

|---|---|---|

| Under 12 months | $7,000 (full) | $2,590 |

| Over 12 months | $3,500 (50% discount) | $1,295 |

Same coin, same profit, half the tax bill. Sell a day early and you hand the ATO an extra $1,295 for no reason. The discount rewards holders and punishes the impatient, which is exactly what it was designed to do.

Which crypto transactions trigger CGT

The trap beginners fall into is assuming tax only happens when crypto turns into dollars. It does not. A crypto-to-crypto swap is a disposal. Spending crypto on goods is a disposal. Even gifting it counts.

| Taxable (CGT event) | Not taxable |

|---|---|

| Selling crypto for AUD | Buying crypto with AUD |

| Trading one crypto for another | Holding crypto |

| Spending crypto on goods | Moving between your own wallets |

| Gifting crypto to someone | Donating to a registered charity |

There is one narrow escape: the personal use asset exemption. Buy under $10,000 of crypto and spend it almost immediately on personal goods, and the gain can be exempt. But the bar is high. If you held it as an investment first, it does not qualify, and the burden of proof sits with you.

Staking, airdrops and crypto income tax

Not all crypto tax is capital gains tax. When you earn crypto rather than buy it, the rules switch tracks, and earned crypto often gets taxed twice across its life.

Staking rewards, most airdrops, referral bonuses, crypto salary, and income from business mining are all treated as ordinary income at their fair market value on the day you receive them. That value is taxed immediately at your marginal rate, even if you never sell. People forget this half completely, then get surprised by the assessment.

The second half comes later. The market value you were taxed on becomes your cost base, so when you eventually dispose of those coins, a separate CGT event applies to any further gain. Receive a staking reward worth $200, get taxed on the $200 as income, and if you sell it later at $300, the extra $100 is a capital gain.

There are wrinkles. The ATO carves out an exception for initial-allocation airdrops, which can carry a zero cost base rather than income on receipt. Hobby mining is treated differently from business mining. But the core principle holds: earn it, and you owe income tax the moment it lands.

Crypto capital losses and the trader line

Losses are the one place the rules cut in your favour. A capital loss on crypto can offset capital gains, and if your losses exceed your gains, the net loss carries forward indefinitely with no expiry — a fact many crypto investors discover only after a painful bear year. A brutal year can shelter a good one years later. Lose $8,000 in a bear market with no gains to absorb it, and that $8,000 simply waits — ready to wipe out the first $8,000 of capital gains you make in some future year, whether that is next year or five years out.

Two catches matter. First, a capital loss can only offset capital gains, not your salary or other ordinary income. Second, the ATO has explicitly warned against wash sales, selling at a loss and rebuying the same asset purely to manufacture a deduction. Do that and the loss can be denied.

Trader status flips the whole picture. If the ATO classes you as carrying on a trading business, your profits become ordinary income with no 50% discount, but your losses and expenses become deductible against other income, and you are generally locked into the FIFO cost method. For active operators that can help; for long-term holders it usually hurts.

The ATO knows: crypto data-matching crackdown

If you take one thing from this article, take this: the belief that crypto is anonymous is the most expensive myth an Australian investor can hold in 2026.

The ATO runs a crypto asset data-matching program that has been operating across the 2014-15 to 2025-26 financial years. Each year it collects records on an estimated 700,000 to 1,200,000 individuals and entities. The data comes straight from designated service providers, the crypto exchanges, which hand over names, addresses, dates of birth, IP addresses, and transaction histories. The ATO retains this data for around seven years and cross-checks it against lodged returns.

When the numbers do not line up, letters go out. The ATO has sent waves of "nudge" and warning letters to holders it believes have under-reported — and penalties for failing to declare can stack on top of the unpaid tax, plus interest. As one ATO line put it, there is no game of hide and seek, because the agency already has the information.

The net is about to get tighter. Australia is implementing the OECD's Crypto-Asset Reporting Framework (CARF), with domestic data collection starting in January 2026 and the first exchange of information with other countries expected around 2028. Australia sits in the first wave of roughly 27 jurisdictions. In plain terms, offshore exchanges will stop being a blind spot. Keep your records for at least five years, because reconstructing years of trades after a letter arrives is far harder than logging them as you go.

Is Bitcoin "money" now? The 2025 ruling

This is the headline that launched a thousand refund dreams. In the case of R v Wheatley, involving a former federal officer and 81.6 Bitcoin, a Victorian magistrate remarked in May 2025 that Bitcoin looked "more akin to Australian dollars" than to shares or gold. If Bitcoin were money rather than property, the argument runs, disposals might escape CGT entirely, and one tax lawyer floated as much as a billion dollars in potential refunds.

Cool your jets. The ATO's guidance has not changed. The remark came in a criminal matter, not a tax ruling, the decision is under appeal, and tax specialists at firms like BDO and academics at Curtin University have warned against filing CGT-free claims on the strength of it. Interesting, yes. Actionable today, no. I would not file a CGT-free return on the back of one remark in a criminal case, and the experts agree. Treat it as a story to watch, not a strategy to bank on.

How to report crypto tax in Australia

The practical mechanics are strict but simple. The Australian tax year runs from July 1 to June 30. If you lodge your own return, the deadline is October 31; go through a registered tax agent and you generally get until around May 15 the following year, provided you register before October 31.

To calculate your crypto taxes, you report disposals in the capital gains section of your return and earned crypto as ordinary income; if the numbers are complex, a crypto-experienced accountant can prevent costly mistakes. If you buy and sell across several platforms, your whole crypto portfolio has to be reconciled, and for working out gains across many parcels, investors can generally choose a cost-base method such as FIFO or HIFO, while traders are restricted to FIFO. Exchange and network fees can be added to your cost base, which trims the taxable gain.

This is mainstream territory now, not a niche concern. Around 31 to 33% of Australian adults have owned crypto, according to Independent Reserve's 2025 and 2026 index surveys, which is part of why the ATO has invested so heavily in tracking it. One forward-looking note: a budget proposal has floated removing the 50% CGT discount from 1 July 2027. It is not law, and may never be, but it is worth watching if you are planning long holds.

The bottom line on Australia crypto tax

Australia's crypto tax rules are settled and tightening, not loosening — and understanding your tax obligations before you lodge is far cheaper than fixing mistakes after. Disposal triggers CGT, earned crypto is income on receipt, and the 50% discount for holding past 12 months is the main lever you control. Above all, the ATO already has your data.

So weigh the two stories honestly. The Bitcoin "money" ruling is a maybe still sitting on appeal — a fascinating legal argument that may yet be overturned. The data-matching program is a certainty already running, year after year. The cheapest, safest move is not a refund theory you read about online. It is clean records, an honest return, and the patience to cross that 12-month line.