Best Blue-Chip Stocks to Buy in 2026: A Beginner’s Guide

Seven companies now make up roughly 35% of the entire S&P 500, and in 2023 and 2024 those seven returned about 156% while the other 493 stocks managed 25%. After a run like that, the old, steady blue chip stocks can feel forgotten, almost quaint. That is exactly when they are worth a second look. This guide explains what a blue chip actually is, names the ones worth owning in 2026, and stays honest about what you give up by holding them instead of chasing the next AI winner.

Blue chips are not exciting. They are the ballast in a portfolio, the part that keeps you steady when the fast money is running for the exits. Whether that is worth owning depends on what job you need your money to do.

What a blue-chip stock actually is

A blue-chip stock is a share in a large, well-established company that leads its industry and has paid its way through multiple economic cycles. The name comes from poker, where the blue chip carries the highest value at the table. These are not magic safe-stocks; they are durable businesses you buy for staying power rather than fireworks. These are large-cap stocks, most carrying a market cap in the tens or hundreds of billions, sitting inside a major index, with a long record of steady earnings. The great majority also pay a dividend, which for many investors is the whole point.

How to spot blue-chip companies

Plenty of big companies have a great year. A great year does not make them blue-chip stocks. Four markers separate the real thing from a temporary high-flyer, and a genuine blue chip usually checks all four.

Size comes first. We are talking about a large market capitalization, usually well above $10 billion and often many times that. Index membership matters next: a seat in the Dow Jones Industrial Average, the S&P 500, or the Nasdaq 100 means a company has already cleared a serious bar. Then there is financial stability that holds through downturns, not just booms, the kind of business that keeps generating cash when the economy turns ugly. And finally, market leadership paired with consistent dividends. Miss one of these and you probably have a big company, not a blue chip.

That last marker is where the gold-standard names live. The S&P 500 Dividend Aristocrats are the 69 companies that have raised their dividend every year for at least 25 straight years. Johnson & Johnson, to take one example, lifted its payout in 2026 for the 64th consecutive year, a streak that has run through recessions, oil shocks, and three different centuries of market panic. That kind of record of consistent dividend payments is hard to fake and harder to maintain.

The best blue-chip stocks to buy in 2026

The discipline here matters: a blue chip list should be real blue chips, not whatever mega-cap technology stock happened to triple this year. The names below split into two camps, the durable growers and the income classics.

Among the growers, Apple and Microsoft are cash machines with enormous balance sheets and businesses that survive most weather. JPMorgan is the leader of American banking, the one rivals are measured against. Berkshire Hathaway is a diversified holding company run for the long term, and notably pays no dividend, preferring to reinvest. On the income side sit the steady compounders: Johnson & Johnson in healthcare, Procter & Gamble and Coca-Cola in consumer staples, Visa in payments, and Walmart in retail.

| Ticker | Company | Sector | Dividend yield | Why it qualifies |

|---|---|---|---|---|

| AAPL | Apple | Technology | ~0.4% | Brand moat, vast cash flow |

| MSFT | Microsoft | Software | ~0.7% | Recurring cloud revenue |

| JPM | JPMorgan | Banking | ~2.0% | Leader of US banking |

| BRK.B | Berkshire Hathaway | Diversified | None | Buffett-built, reinvests |

| JNJ | Johnson & Johnson | Healthcare | ~2.3% | 64-year dividend streak |

| PG | Procter & Gamble | Staples | ~2.5% | Defensive, recession-resistant |

| KO | Coca-Cola | Beverages | ~2.8% | 60+ years of dividends |

| V | Visa | Payments | ~0.7% | Toll booth on global spending |

| WMT | Walmart | Retail | ~0.9% | Scale nobody can match |

A word on price, because it is where beginners trip. A great company is not the same as a great investment if you overpay for it. When a blue chip gets crowded with nervous money, its valuation can climb past what the business can grow into, and you end up waiting years for the price to catch up to the hype. The fix is not complicated: buy in pieces over time rather than all at once, and favour the names trading closer to their long-run earnings multiple than their euphoric highs. Patience is cheaper than a perfect entry.

No single name on that list will double in a year. Together, held for a decade, they are the kind of portfolio you do not have to babysit.

Blue-chip stocks versus the AI growth trade

Here is the comparison almost nobody runs honestly. Over the past ten years, blue chips have lagged the growth trade, and that is the entire point of owning them. They are insurance, not a lottery ticket.

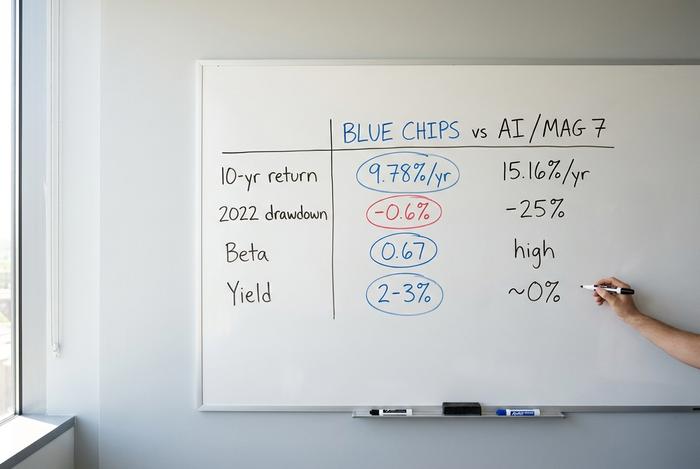

The numbers are stark. The Magnificent Seven now account for about 34.8% of the S&P 500's value. In 2023 and 2024 they returned 156.1% as a group while the remaining 493 companies returned 25.2%. Over a full decade, the Dividend Aristocrats compounded at roughly 9.78% a year against the S&P 500's 15.16%. If you owned blue chips through the AI boom, you left real money on the table. There is no soft way to say that.

But look at the other side of the cycle. In the 2022 selloff, when the S&P 500 fell about 25%, consumer staples — the heart of the blue chip world — were essentially flat at -0.6%. The staples sector carries a beta near 0.67, meaning it moves about two-thirds as hard as the market in either direction. You give up some of the up to skip most of the down.

| Trade | 10-yr return | 2022 drawdown | Beta | Yield |

|---|---|---|---|---|

| AI / Magnificent Seven | far higher | deep | high | near zero |

| Blue-chip Aristocrats | ~9.78%/yr | about flat | ~0.67 | 2-3% |

So which is right? Neither, on its own. The growth trade builds wealth in good years and tests your nerve in bad ones. Blue chips do the reverse. Most sensible portfolios hold both, and the only real question is the mix.

A simple way to think about it is a barbell. Put a stable core in blue chips for the income and the downside protection, then add as much growth as your time horizon and your stomach can handle on the other end. A younger investor with decades ahead can tilt heavily toward growth and treat blue chips as a small anchor. Someone near retirement flips that ratio, leaning on the dividends and the lower volatility. The blue chip allocation is not a bet on blue chips beating the market; it is a deliberate choice to smooth the ride and get paid while you wait.

Why invest in blue-chip stocks

Strip away the excitement and the case comes down to two quiet things: compounding and sleep. Start with compounding, because the number surprises people. Reinvested dividends have made up about 85% of the S&P 500's total return since 1960. Read that again. Not the price gains everyone watches, but the dividends, plowed back in year after year. That is where most long-term growth actually comes from.

It matters more now than usual. The S&P 500 yields only about 1.04% today, near record lows, because the index is stuffed with mega-cap tech that pays little or nothing. Against that backdrop, a blue chip throwing off 2.5% to 3% looks generous, and a payout that climbs every year quietly fights inflation. Near retirement, that income is what lets you cover the bills without selling shares into a falling market.

There is also the track record itself. The 69 Dividend Aristocrats did not earn that title in a calm market; they raised payouts straight through the dot-com crash, the 2008 financial crisis, and the 2020 shutdown. A company that keeps increasing its dividend across all of that is telling you something real about the durability of its cash flow, something a flashy revenue chart cannot.

The second thing is temperament. Spreading money across a handful of financially stable market leaders in different sectors means no single bad headline wrecks you. You can diversify with a few blue chips in a way you cannot with one hot growth name. The boring portfolio is the one you actually hold through a crash, and holding through the crash is where most of the long-run return is won or lost.

The risks blue-chip stocks still carry

Stability is not the same as safety, and pretending otherwise is how beginners get hurt. Blue chips carry real costs.

The obvious one is lower growth. A company already worth half a trillion dollars cannot easily double; the explosive gains live in smaller, riskier names. The second is valuation. When everyone wants safety, blue chips get bid up, and a great company bought at a rich price is still a mediocre investment. Third, no blue chip is immune to economic downturns. Plenty of them fell hard in 2008 and 2020, and a few have cut dividends that once looked untouchable. Finally, size makes companies slow. The blue chip roster is littered with former giants, names like General Electric or Intel in its long decline, that ruled their era and then failed to adapt. Today's leader is not guaranteed tomorrow's, which is the strongest argument for owning a basket rather than betting the farm on one venerable ticker. A famous name guarantees nothing; what protects a company is durable cash flow and the ability to keep adapting. Treat the blue chip label as a starting filter, then keep checking that the business behind the name is still the leader it used to be.

Blue-chip ETFs versus index funds

For most beginners, buying the basket beats picking ten names by hand. A fund spreads your money across dozens of blue chips in a single trade, and the cheap ones cost almost nothing to own.

A plain S&P 500 index fund already holds every blue chip in the country, weighted by size. If you want a tilt toward dividends, dedicated funds do the screening for you. The largest dividend-growth exchange-traded funds have become huge precisely because investors want this exposure without the homework.

| Ticker | Focus | Yield | Expense ratio |

|---|---|---|---|

| SCHD | Dividend-quality blue chips | ~3.27% | 0.06% |

| NOBL | S&P 500 Dividend Aristocrats | ~2.21% | 0.35% |

| DGRO | Dividend growth | ~2.3% | 0.08% |

A low-cost exchange-traded fund or mutual fund tracking these baskets gives you instant diversification. The trade-off is that you own the laggards along with the leaders, which for most people turns out perfectly fine.

How to buy blue-chip stocks the smart way

The mechanics of buying blue-chip stocks take five minutes. Open a brokerage account, search the ticker, choose a market or limit order, and buy. The decisions around the mechanics are what matter. Decide first whether you want individual names or a fund, because that determines how much research you are signing up for. Turn on dividend reinvestment so each payout buys more shares automatically. Size the position for a long holding period, not a quick trade. And because nobody can time the market, add to your portfolio steadily over time rather than betting it all on one entry price. A fixed amount invested every month does the averaging for you and takes the emotion out of the decision. None of this requires special skill or a trading screen you watch all day. The whole appeal of blue chips is that the smart move is also the boring one: buy quality, reinvest the income, and leave it alone.

The bottom line on blue-chip stocks

Blue chips are the ballast, not the engine. You own them for the dividends that compound quietly and for the way they hold up when the exciting stocks are falling apart. They will not win you the cocktail-party bragging rights that an AI moonshot might. They will, more reliably, still be standing when the moonshot is not. Pair a core of blue chips with whatever growth your stomach allows, reinvest the dividends, and let the slow math do its work.