How Stablecoins Are Revolutionizing iGaming Crypto Payments 2026

An iGaming operator processing a $100 deposit through Visa loses anywhere from $5 to $9 of it before a single bet hits the casino floor. Stake.com handled an estimated $10 billion in monthly bets during 2024 against roughly $4.7 billion in annual gross gaming revenue. Almost none of that volume touched a card processor. The operator runs on stablecoin rails by default. The shift is no longer a curiosity. It is the dominant route for a tier of operators that books billions in handle. Total stablecoin supply crossed $320 billion in May 2026. More than half of crypto-casino wagers now settle in stablecoins rather than volatile assets, per industry data compiled by BSN. This piece looks at iGaming through the operator's profit-and-loss statement, not the player onboarding screen. It walks the operator-economics rewrite layer by layer: the fiat cost stack, the stablecoin replacement, the chargeback math, settlement and treasury impact, the regulatory patchwork, the geo-arbitrage that fiat rails cannot reach, and a six-step integration playbook.

The fiat cost stack hidden inside every iGaming deposit

Every fiat deposit at a regulated online gambling site triggers a multi-layer charge structure that operators pay invisibly before they see net revenue. The base layer is the Visa or Mastercard interchange and processor fee for merchant category code 7995, the high-risk code assigned to online gambling. That fee alone runs 3 to 5 percent per transaction, according to iGaming Payment Solutions data published through 2026. On top of interchange, the acquiring bank applies a high-risk markup typically in the 2 to 4 percent range, depending on the operator's licensing footprint and dispute history.

The third layer is the rolling reserve. Acquirers holding high-risk gambling accounts withhold 10 to 15 percent of monthly card volume for six to twelve months as protection against chargeback exposure, per documentation analysed by the Coinmonks publication on Medium in 2025. That is working capital the operator has booked but cannot deploy. The fourth layer is the chargeback fee itself, $20 to $50 per dispute on top of the reversed transaction, and disputes are not rare; gambling sits at the worst end of the merchant population for chargeback frequency.

The fifth layer is the failure rate. Card decline rates for MCC 7995 transactions average 30 to 40 percent at the issuing bank level, versus 5 to 10 percent for standard e-commerce. Roughly 55 percent of declined players never return to attempt the deposit again, which is a near-total loss of acquired traffic for the operator who already paid the marketing cost.

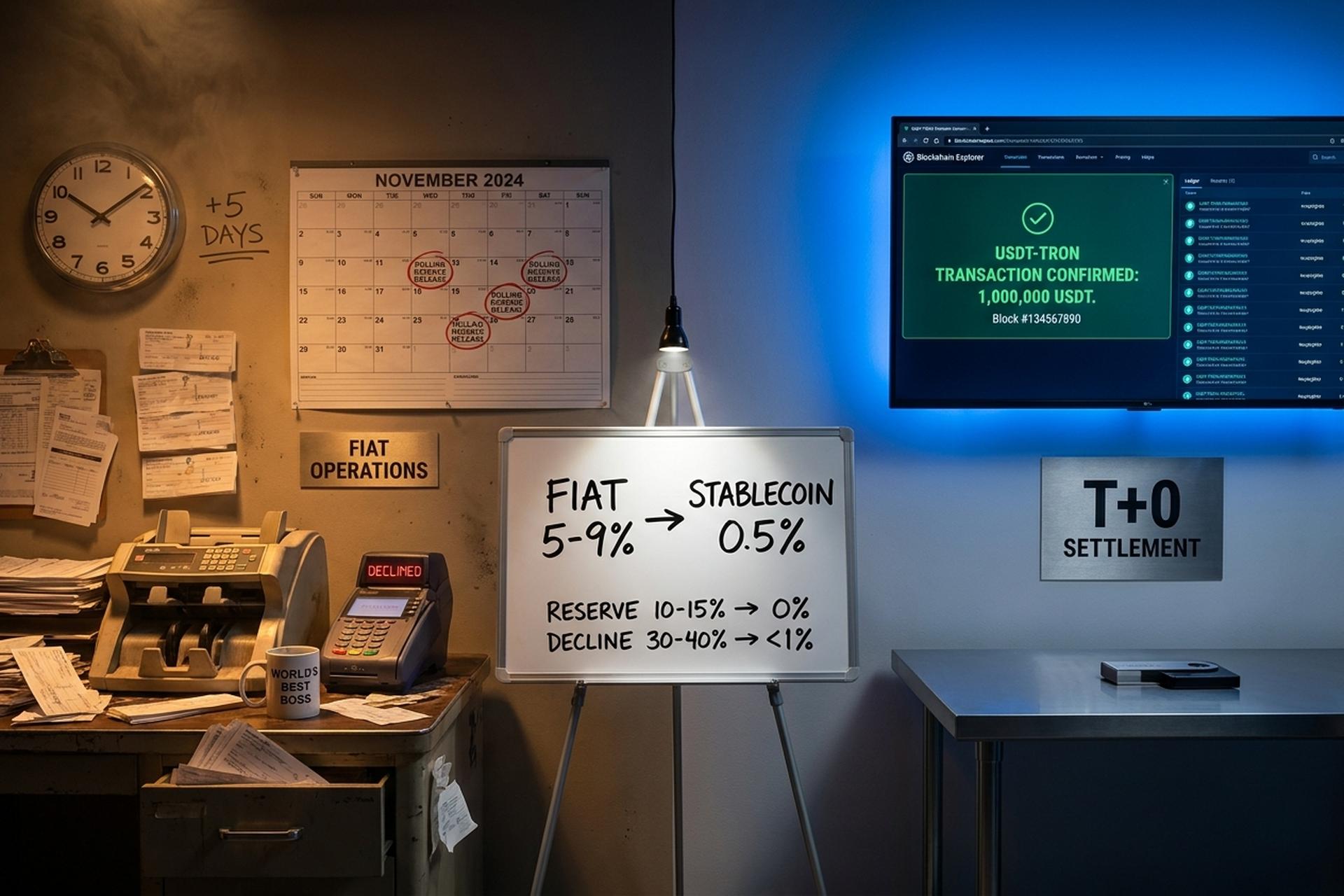

A regulatory layer was added in late 2025. Visa's Acquirer Monitoring Program, known as VAMP, came into force on October 1, 2025. Mastercard runs a similar Acquirer Chargeback Monitoring Program. Its threshold sits at 100 disputes per merchant per month, or a 1.5 percent rate, whichever triggers first, per Chargebacks911 and Moneris notes. Operators who tolerated high dispute rates while surcharges were dormant are now flagged into excessive-chargeback programs. The fiat stack adds up to a blended 5 to 9 percent per dollar deposited — before the player has bet anything.

How stablecoin payments rewrite iGaming operator margins

When the cost stack collapses from 5 to 9 percent down to roughly 0.5 percent with no rolling reserve and no chargebacks, the operator's per-deposit gross margin shifts by six to ten percentage points. Apply that gap to a $100 million annual deposit volume and the savings buy an entire marketing budget. The math is not subtle, and operator case data confirms it: PayRam reported 60 to 70 percent processing cost reduction across the operators it surveyed after crypto adoption in 2025.

The processor side of the comparison is concrete. Plisio publishes a flat 0.5 percent gateway fee on its public pricing page, with instant settlement, zero rolling reserve, and no chargeback exposure by construction. Transaction fees vary by chain: USDT on Tron settles at roughly $0.20 per transaction, USDT on Solana at less than one tenth of a cent, and USDT on Ethereum at $2 to $10 depending on gas conditions, per Eco.com's 2026 fee comparison. For deposit-scale traffic, Tron and Solana dominate; Ethereum is structurally too expensive at the unit-economic level for casino-scale flow.

A worked back-of-envelope makes the contrast unmistakable. A $100 fiat deposit lands at $91 to $95 of net revenue to the operator — and only after six to twelve months of locked reserve. The same $100 deposit in USDT-Tron lands at $99.30 net within 30 seconds, with no reserve and no settlement delay. At $50 million in monthly deposit volume the per-month difference is in the range of $2.25 million to $4.25 million in immediate cash before reserves are even factored in.

Margins improve beyond the headline percentage for three reasons operators often understate. First, no chargeback reserve means capital is liquid the same day. Treasury can deploy it now rather than wait a quarter for the acquirer to release it. Second, the decline rate falls toward zero. There is no issuing bank to block the deposit at the MCC level. That recovers the 55 percent of declined fiat players who would otherwise vanish. Third, marginal cost is fixed and predictable. The operator can price bonuses against a known floor instead of a Visa scheme rate the network can adjust mid-quarter.

| Cost layer | Fiat card rail | Stablecoin gateway |

|---|---|---|

| Processor / interchange | 3-5% (MCC 7995) | 0.5% (e.g. Plisio) |

| Acquirer high-risk markup | 2-4% | 0% |

| Rolling reserve | 10-15% held 6-12 months | 0% |

| Chargeback fee per dispute | $20-50 + transaction reversal | None (immutable) |

| Decline rate | 30-40% | <1% |

| Settlement time | T+1 to T+5 | 30 seconds (Tron) |

Chargebacks and crypto: the silent iGaming GGR leak

Chargebacks are not a fee. They are a directional cash flow that reverses revenue weeks after it was booked. For an iGaming operator with 30 to 40 percent decline rates and disputed-deposit rules at every issuing bank, this is the silent leak that digital asset settlement eliminates by design rather than by mitigation.

The mechanic is simple and operationally brutal. A Visa or Mastercard chargeback is a consumer-protection reversal that the cardholder can initiate up to 120 days after the transaction. For gambling, the disputer can frame a losing bet as unauthorised or not as described. The operator pays back the deposit amount, owes a $20 to $50 dispute fee, and loses the in-game balance the player already wagered against the house. The Merchant Risk Council estimates that chargeback fraud accounts for around 70 percent of online-business fraud losses overall, and iGaming sits at the heavy end of that distribution.

Stablecoin transactions do not chargeback because the underlying ledger is the receipt. Once a USDT transfer confirms on Tron or USDC confirms on Solana, the operator owns the funds and the player cannot reverse the transaction at the protocol level. There is no Visa scheme rule to invoke, no acquirer to sit between the dispute and the merchant.

The counter-argument from compliance teams is that crypto somehow weakens know-your-customer obligations. That misreads the trade. Stablecoins do not replace KYC; regulated operators still onboard players through full AML screening, sanctions checks, and source-of-funds review. What changes between the two rails is the disputability of a settled transaction. Finality is the feature here, and anonymity has nothing to do with it.

Settlement speed, rolling reserves, and treasury impact

Instant settlement reads first as a player-side UX feature, but the bigger consequence sits inside treasury. It changes the operator's working capital profile, and the real-time finality of on-chain transfers is what makes that shift permanent rather than provisional. A $50 million monthly book that previously sat in T+1 to T+5 settlement plus a 10 to 15 percent rolling reserve frees up roughly $5 to $6 million of liquidity each month once the rails switch.

The settlement numbers are concrete. Fiat card processing for high-risk merchants typically settles on a T+1 to T+5 cycle, and the rolling reserve adds six to twelve months of holdback on top, per iGaming Payment Solutions and Coinmonks analyses. USDT on Tron settles in roughly 30 seconds at a network fee around $0.20. USDC on Solana settles in under a second at sub-cent fees, and USDT on Ethereum settles within a minute or two but at $2 to $10 per transaction depending on gas, per Eco.com data. For deposit-scale traffic the Tron and Solana variants dominate; Ethereum exists for institutional-size flows where the fee tail is amortised.

The treasury implication is that the same flow is now deployable. The operator can convert end-of-day USDC into fiat for opex, hold USDC for payout liquidity, or sweep into yield-bearing instruments that the acquirer's rolling reserve previously denied them.

MiCA, GENIUS Act, and the stablecoin regulation patchwork

The 2025-2026 regulatory wave is splitting global iGaming into three operational tiers: compliant-USDC, compliant-EMI-stablecoin, and offshore-USDT. Each tier sits inside a different regulatory framework governing stablecoin issuance, reserve requirements, and financial services licensing. Operators have to pick a stack matched to their gaming license, because the wrong combination triggers de-banking risk that no margin saving can offset.

In the European Union, MiCA is fully in force. Circle holds an Electronic Money Institution license in France. That makes USDC the default MiCA-compliant choice for any operator in an EU jurisdiction. Tether's USDT does not yet meet the same bar, so MiCA-licensed operators lean toward USDC. In the United States, the GENIUS Act final rules are due in July 2026. They will set federal reserve and disclosure standards for US stablecoin issuers. Circle and Paxos have already restructured ahead of the deadline, per KuCoin's 2026 regulation tracker. The act treats stablecoins as regulated payment instruments under federal oversight rather than as ambiguous money-transmitter products.

Gambling-licensing regimes are tracking on their own clocks. The UK Gambling Commission, under chief executive Andrew Rhodes, has shifted from a five-year horizon on crypto-payments policy to an 18 to 24 month window, per the iGaming Business industry briefing. Curacao's revamped license now requires proof-of-reserves disclosure for stablecoin balances on the operator side. The Netherlands Kansspelautoriteit bans crypto payments outright. Estonia, under tightened AML, allows them subject to standard licensing review. Brazil's central bank banned cross-border stablecoin and crypto settlement for retail-facing operators in October 2025, per CoinDesk. That redirected operator integration toward local off-ramp partnerships.

The operator playbook is now jurisdiction-by-jurisdiction. A Curacao-licensed brand can run USDT-Tron natively at scale. A Maltese-licensed operator should default to USDC under MiCA. A UKGC-licensed brand can experiment within sandbox parameters but not at the deposit volumes that move the unit economics yet.

| Jurisdiction | Regulatory frame | Stablecoin status for iGaming |

|---|---|---|

| European Union | MiCA in force | USDC compliant (Circle EMI France); USDT not aligned |

| United States | GENIUS Act (final rules Jul 2026) | Circle, Paxos pre-aligned; broader operators staging |

| United Kingdom | UKGC review window | Sandbox-only at this stage |

| Curacao | Revamped license + proof-of-reserves | USDT-Tron permitted with operator-side disclosures |

| Netherlands | KSA prohibition | Crypto payments not allowed |

| Brazil | Central bank ban Oct 2025 | Cross-border closed; domestic OTC routes |

Geo-arbitrage: where stablecoins unlock iGaming markets

Stablecoins solve markets where fiat-rail iGaming is structurally impossible. The blocker is rarely tech and almost always banking. Fiat moves through correspondent banks that can simply refuse gambling settlement. Cross-border payments in USDT or USDC skip that layer entirely. An operator who routes a $20 deposit from São Paulo at 0.5 percent beats the one who routes the same deposit through Visa Brazil at 7 percent against a 35 percent decline rate.

Brazil after October 2025 illustrates the dynamic. The central bank's cross-border crypto settlement ban closed the front door for retail-facing operators using stablecoins as a direct funding rail. The functional workaround is local OTC integration: the player buys USDT from a Brazilian exchange in BRL, then deposits the stablecoin into the operator. The grey-but-functional rail keeps the market open while compliance teams update their banking relationships.

India is the cleaner example. UPI, the national real-time payments rail, blocked gaming-related merchant category codes through a 2024 directive. Domestic fiat rails are functionally closed for online gambling. USDT-Tron remains the only working deposit rail at scale, and the operator who masters off-ramp partnerships there captures a market the licensed Indian payments stack has structurally exited.

Sub-Saharan Africa runs on a similar pattern. Visa acquiring for gambling merchants is rare. M-Pesa-to-USDT bridges through local exchanges become the integration of record. In Latin America more broadly, Mastercard research cited by BVNK in 2025 found about a one-in-three chance that an adult consumer has already used stablecoins for ordinary payments. That shifts the work: user education is mostly done, and the operator's job is rail integration rather than market creation.

Turkey and Argentina add a fourth pattern. Currency volatility makes USDT itself the deposit currency in real economic terms, not just the rail. Players hold a US dollar-pegged stablecoin to preserve purchasing power between bets, and the operator who accepts it natively avoids the FX leakage that a fiat-only flow would book.

Operator playbook — integrating stablecoin payments cleanly

Stablecoin integration is a six-step procurement decision, not an engineering project. Programmable payouts and automated treasury sweeps are byproducts of the architecture, not the primary goal. The failure mode is to sign with a non-licensed gateway and inherit the gateway's AML exposure into the operator's gaming license.

First, choose the chain mix. USDT on Tron plus USDC on Solana covers roughly 80 percent of deposit volume at fees low enough to ignore. Ethereum stays in the stack for institutional flows only. Second, pick a licensed gateway whose footprint matches the operator's gaming license. Plisio, BVNK, and BitPay-tier processors publish their license registry. Compliance should validate it before commercial terms are signed. Third, map the Travel Rule and AML duty: who screens, who reports, who owns suspicious-activity filings. Fourth, build the off-ramp so end-of-day USDC sweeps into fiat opex if treasury policy requires it. Fifth, update player terms to acknowledge crypto-finality: no chargebacks, no reversals, and an attribution model that ties deposits to wallet addresses. Sixth, run a 90-day shadow period alongside the existing fiat stack before flipping any volume. That tests the integration against real player traffic at low risk.

Conclusion: stablecoin economics already won the iGaming math

The operator economics math is not subtle. A 5 to 9 percent cost stack with chargeback exposure does not survive a 0.5 percent alternative that settles instantly. This is how stablecoins are revolutionizing iGaming at the infrastructure level — not as a player-facing feature but as a margin-redistribution event running through the operator's profit-and-loss statement. The gaming industry is adapting jurisdiction by jurisdiction, traditional payments are losing share to borderless stablecoin rails, and the playbook is starting to look standard rather than experimental. The unit economics already shifted.