Merchant Payment Meaning: Services, Process & Benefits

Tap a card, click "Pay now," scan a QR code — each of these triggers a merchant payment. Most business owners take it for granted. But if you've ever wondered why a transaction gets declined, why funds show up three days late, or why your processing bill keeps climbing, the merchant payment meaning is where those answers live. Behind every sale is a chain of systems, accounts, and agreements that most merchants never see — and rarely think about until something breaks.

What Is a Merchant in the Payment Ecosystem?

The word sounds old, like someone selling spices off a cart. But in payment terminology, "merchant" has a very specific meaning: the person or business on the receiving end of a payment transaction. You sell something, someone pays you — you're the merchant.

Three types show up most often:

- Retail merchants — physical stores taking in-person payments via POS terminals

- Online merchants — e-commerce businesses processing payments through web-based gateways

- B2B merchants — companies invoicing other businesses via bank transfers, virtual terminals, or procurement systems

What they all share is dependence on the same underlying network. Every sale — whether a coffee tap or a $50,000 B2B invoice — runs through banks, card networks (Visa, Mastercard, UnionPay), payment processors, and various tech intermediaries before money lands in anyone's account. You don't see most of it. But it's all running in the background on every transaction you complete.

Merchant Payment Meaning: The Core Concept

Here's the short answer: a customer pays you, you get money. But the merchant payment meaning is really about the journey funds take to get from their bank to yours — and that journey looks different depending on how the customer pays.

Credit card and debit card payments run through Visa or Mastercard. The issuing bank approves the charge. The acquiring bank eventually receives the settlement. Days later, it's in your account. Bank transfers cut the card networks out entirely — one account moves money directly to another, often preferred for B2B deals or large invoices. Then there are digital wallets: Apple Pay, Google Pay. They don't transmit real card data at all, just encrypted tokens. And crypto sits at the opposite end of the spectrum — peer-to-peer on a blockchain, no banking infrastructure involved whatsoever.

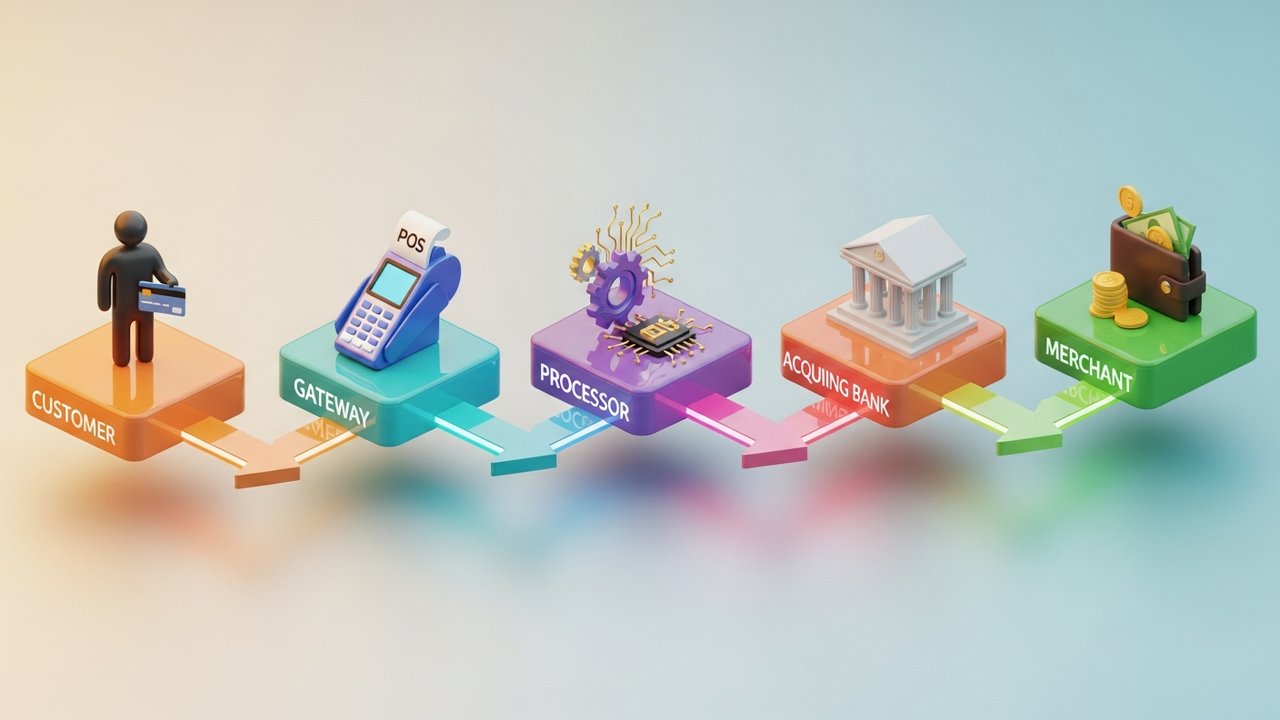

Regardless of method, five parties are always present. The customer. You, the merchant. A payment processor routing the data. An acquiring bank holding funds before settlement. A card network enforcing the rules. Pull any one of those out of the chain and the transaction either fails or freezes.

How Merchant Payment Processing Works

Two seconds. That's how long a card tap takes from the customer's perspective. Internally, it's a small miracle of coordinated systems.

Credit card swipe, debit card tap, digital wallet tap — the payment process runs the same sequence either way:

- Initiation — Customer presents payment. Terminal or gateway captures the data.

- Transmission — Encrypted data goes to the payment processor, routed to the appropriate payment network.

- Authorization — Card network forwards it to the issuing bank. Bank checks funds and fraud signals, replies with approval or decline.

- Capture — Merchant captures the approved funds. Happens immediately in most cases, delayed in others (pre-authorizations, for instance).

- Settlement — Processor batches the day's transactions, sends settlement files to the acquiring bank. Funds leave the issuing bank and land in the merchant's bank account — usually T+1 to T+3 business days later.

People often treat authorization and settlement as one event. They're not. A card payment gets authorized (money reserved) without being captured yet. Hotels do this constantly. So do car rental companies and subscription platforms with trial periods.

The Baymard Institute tracked this: 18% of online sales fail because of checkout friction alone. Not a broken product, not a bad price — just a clunky payment process. That's real revenue lost.

Types of Merchant Payment Services Explained

Merchant services covers every tool a business uses to accept and manage payments. Which ones make sense depends on your sales channels, transaction volume, and the payment methods your customers actually use.

| Service Type | Best For | Common Examples |

|---|---|---|

| POS System | Retail, restaurants, hospitality | Square, Clover, Stripe Terminal |

| Online Payment Gateway | E-commerce, SaaS, subscriptions | Stripe, PayPal, Braintree |

| Mobile POS (mPOS) | Field sales, pop-ups, events | SumUp, iZettle, Square Reader |

| Virtual Terminal | Phone orders, B2B invoicing | PayPal Here, Authorize.net |

| Buy Now Pay Later (BNPL) | High-ticket retail, fashion, electronics | Klarna, Afterpay, Affirm |

| Crypto Payment Gateway | Global e-commerce, digital goods, gaming | Plisio, BitPay, CoinGate |

Most businesses end up using more than one. A Shopify store might use Shop Pay checkout for domestic buyers who want fast checkout, and a crypto gateway for international customers who'd rather pay in Bitcoin or stablecoins.

Merchant Account vs. Payment Gateway: Key Differences

These two get confused constantly. They're not the same thing, and understanding the difference saves headaches when something goes wrong.

| Feature | Merchant Account | Payment Gateway |

|---|---|---|

| What it is | A holding account for incoming funds before settlement | Software layer that authorizes and routes payment data |

| Operated by | An acquiring bank or payment facilitator | A technology provider (often bundled with a processor) |

| Purpose | Holds funds between transaction and settlement | Encrypts and transmits transaction data securely |

| Required separately? | Not always — PSPs bundle it | Often included with merchant account |

| Setup time | Days to weeks (traditional banks) | Minutes (modern PSPs) |

Old-school setup meant applying to a bank for a merchant account: underwriting, a credit check, monthly minimums, the works. Modern payment service providers cut all that. Stripe, Square, and similar aggregators hold a master account and let businesses operate underneath it. Setup takes minutes, not weeks.

The gateway handles the front end: capturing, encrypting, forwarding the payment data. The merchant account handles the back end: holding the money until settlement. Both have to function for a payment transaction to clear.

Benefits of Merchant Payment Services for Business

Accepting digital payments does more than let customers pay conveniently. The ripple effects matter.

- More customers. 73% of consumers prefer contactless or card payments (ONBE, 2023). A business that can't take electronic payment is invisible to most buyers before they even walk in the door.

- Faster cash flow. Digital payments settle in T+1 to T+3 days. Compare that to chasing checks or waiting on wire transfers that may or may not arrive.

- Fraud protection. Card networks and processors include built-in fraud detection, 3D Secure authentication, and chargeback handling. That coverage comes standard.

- Real data. Modern merchant service providers give you dashboards showing sales by channel, geography, payment method. That's inventory and marketing information, not just accounting.

- Scalability. A good payment stack doesn't need to be renegotiated every time your revenue grows.

Small businesses that accept digital payments grow twice as fast as those that don't — that's from Mastercard's 2024 research. Add crypto and the advantage extends further: lower interchange costs, borderless transactions, zero chargeback exposure on crypto rails.

Merchant Service Provider Fees: What to Expect

Every merchant payment has a cost attached to it. The fee structure isn't complicated, but it stacks.

| Fee Type | Typical Range | Notes |

|---|---|---|

| Interchange fee | 0.2%–2.0% per transaction | Set by Visa, Mastercard, and other networks; non-negotiable |

| Processing/markup fee | 0.5%–1.5% | Added by the payment processor on top of interchange |

| Monthly account fee | $0–$50/month | Varies; some PSPs waive it for high-volume merchants |

| PCI compliance fee | $50–$200/year | Required for any business storing or transmitting card data |

| Chargeback fee | $15–$100 per dispute | Charged when a customer disputes a transaction |

| Cross-border fee | 0.5%–2.0% | Applied to international card transactions |

Blended, most merchants pay 1.5% to 3.5% per card transaction. Credit card transactions cost more than debit card payments on interchange, especially for premium rewards cards. Ignore PCI compliance and fines can hit $500,000 — that's not a hypothetical.

When shopping for a merchant service provider, the headline rate is just the start. Interchange-plus pricing shows you exactly what goes where. Flat-rate pricing is simpler but often costs more at volume. Visa and Mastercard set the interchange — that's fixed — but everything the processor adds is negotiable.

Crypto removes most of this. No interchange, no network markups, no chargebacks. The transaction settles and it's done.

How Crypto Is Changing Merchant Payments

The traditional payment process was designed around banks and physical cards. Crypto runs on completely different logic — and that logic solves real merchant problems.

What actually changes when you accept cryptocurrency:

- No intermediaries. Buyer's wallet to merchant's address, directly. No acquiring bank, no payment network sitting in the middle taking a cut.

- Faster settlement. Cards take days. Crypto confirms in seconds to minutes depending on the network. That's a material difference for cash flow.

- Built-in global reach. A merchant in Europe gets the same transaction as a buyer in Southeast Asia. No cross-border fees, no currency conversion mess.

- No chargebacks. Blockchain transactions don't reverse. Once confirmed, the funds belong to the merchant. Full stop.

- Stablecoins as a middle ground. Not comfortable with price volatility? Accept USDC or USDT instead. You get the speed and cost benefits of crypto without the exposure to price swings.

For practical implementation, Plisio is a payment gateway supporting 30+ cryptocurrencies with simple API integration. You can accept fixed-amount crypto payments without creating a new invoice every time, or add specific chains like TON cryptocurrency payments as your audience expands.

Crypto isn't replacing cards anytime soon. But for international sellers, digital goods businesses, and anyone with a Web3 customer base, it's a genuine operational advantage.

Merchant payment meaning isn't just a definition to memorize. It's the framework for making better decisions about your payment stack — which tools to choose, what fees to push back on, where crypto saves you money, and why checkout speed directly affects revenue. Understanding how merchant payments actually work puts you in a better position on all of it.

Exploring crypto? Plisio runs a payment gateway with no monthly fees, 30+ supported coins, and integrations that take hours, not weeks. Worth a look if you're accepting credit cards through a traditional merchant account and want to see what else is possible.