Nebius Group NBIS Stock 2026: Yandex Exit, $44B AI Backlog

Nineteen months ago, NBIS stock did not exist as a Nasdaq ticker. The Yandex N.V. shares that became Nebius had been frozen on the exchange since February 2022. Today the same Dutch-incorporated company is profitable at the EBITDA line, sits on $9.3 billion in cash, and carries roughly $44 billion in signed five-year customer commitments from Microsoft and Meta. The stock has run from a $13.65 relisting open to $208 in nineteen months, a roughly fifteenfold move that puts NBIS among the most extreme post-relisting performances in recent tech history. This guide walks through what Nebius actually is and how it reached Nasdaq under a new identity, where the AI-infrastructure thesis sits versus CoreWeave on unit economics, what the Nvidia anchor investment and the Microsoft and Meta backlog mean in revenue terms, and what the $20–25 billion FY2026 capex guidance does to the financing and dilution story.

What Nebius is and how NBIS reached Nasdaq

Nebius Group N.V. is the Dutch-incorporated company that until August 2024 was known as Yandex N.V. The original parent IPO landed on Nasdaq on May 24, 2011 at $25 per share, raising $1.3 billion. The Russia-Ukraine war triggered a Nasdaq trading suspension in February 2022, which froze the equity for two-and-a-half years.

The restructuring closed on July 15, 2024, when Yandex N.V. sold all Russia-based operations to a Russian investor consortium for approximately $5.4 billion in cash and own-share consideration. What stayed with the Dutch parent was a portfolio of global businesses with no Russian operating exposure: the Nebius cloud and AI-infrastructure platform, Avride (the former Yandex Self-Driving Group), Toloka (crowdsourced data labelling), and TripleTen (edtech bootcamps). On August 16, 2024, the holding company was renamed Nebius Group N.V. On October 21, 2024, the shares resumed trading on Nasdaq under the new ticker NBIS. The retained cash from the Russia divestment, roughly $2.95 billion, funded the AI buildout pivot. That single transaction is the reason Nebius started its public life under the new name with a fortress balance sheet, while every other AI-infrastructure challenger had to lever up or raise dilutive equity to fund the same construction.

NBIS stock price 2024–2026: from $13 relisting to $208

The NBIS stock price chart is one of the most extreme post-relisting performances in recent tech history. Open on October 21, 2024 at roughly $13.65. Drifted through the $30s and $40s into early 2025. The 52-week low printed at $34.72 during the Q1 2025 capex-disclosure pullback. The 52-week high reached $233.73 in May 2026. The current stock quote in late May 2026 sits at $208.37. Market capitalisation is $53.35 billion. Shares outstanding are 256 million, up from roughly 196 million at the relisting date, which is a 30% increase in eighteen months from a combination of equity raises, convertible note conversion, and customer-side share issuance. Short interest stands at 17.82% of float, or roughly 45 million shares, and is up 1,186% since the relisting date. The combination of a fifteen-fold rally and a four-tenths-of-the-float short position creates one of the more interesting positioning dynamics on Nasdaq in 2026.

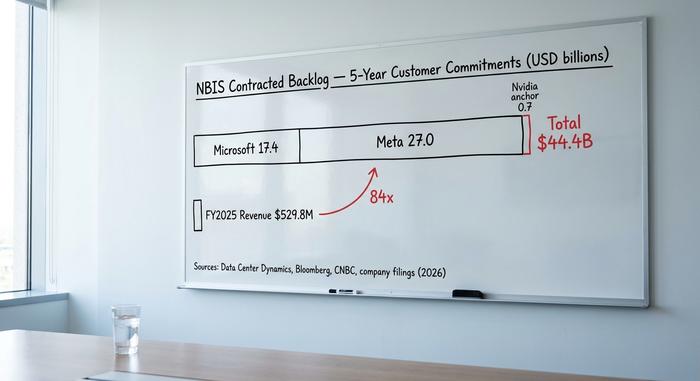

The $44 billion backlog: Microsoft, Meta, and Nvidia

Most NBIS coverage treats the Microsoft deal and the Meta deal as separate news items. They are the same revenue story unfolding in stages, and the Nvidia anchor investment from December 2024 is the precondition for both.

On December 2, 2024, Nebius announced an oversubscribed $700 million strategic equity financing, 33.3 million shares at $21.00, with anchor commitments from Nvidia, Accel, and Orbis Investments. The transaction was the market's first signal that Nebius was being treated as a strategic AI-compute node, not a Russian-spinoff holding company. Nvidia's participation in particular signalled allocation priority on Blackwell-class GPU supply, which is the gating constraint for every AI infrastructure operator in 2026.

Microsoft contracted backlog: $17.4 billion over five years, signed in late 2025 / early 2026 per Data Center Dynamics reporting. The deal covers multi-year GPU-capacity reservation across Nebius sites, with Microsoft routing certain Azure AI workloads through Nebius rather than building incremental capacity itself.

Meta contracted backlog: up to $27 billion over five years, signed and disclosed on March 16, 2026 (Bloomberg, CNBC, Nebius investor release). Meta is using Nebius capacity to expand Llama and AI-agent training workloads outside its own gigawatt-scale construction pipeline.

Combined contracted backlog: roughly $44.4 billion. That figure is the largest signed AI infrastructure customer commitment outside the hyperscalers themselves. It is also visible on the balance sheet: $2.3 billion of the $9.3 billion Q1 2026 cash position is customer prepayments. Microsoft and Meta paid upfront for capacity, which is unusual in cloud-infrastructure contracting and reduces Nebius's working-capital strain through the buildout.

The structural read for retail is that Nebius is no longer competing on cost or general-purpose cloud. It is operating as a contractually pre-sold full-stack infrastructure supplier for AI training and inference, with five-year revenue visibility. The bull case prices the backlog converting to revenue at roughly $9 billion annually by FY2027–2028. The bear case prices delivery risk against $20–25 billion of FY2026 capex.

Nebius AI infrastructure vs CoreWeave unit economics

The cleanest peer comparison for NBIS is CoreWeave (CRWV), which IPO'd in May 2024 with a similar AI-infrastructure pitch and a comparable hyperscaler customer mix. The numbers diverge in a way that explains the valuation premium.

| Company | Ticker | Market cap (May 2026) | FY2025 revenue | FY2025 net income | EBITDA profitable? |

|---|---|---|---|---|---|

| Nebius | NBIS | $53.4B | $529.8M | +$101.7M | Yes |

| CoreWeave | CRWV | ~$30B | $5.1B | –$1.2B | No |

| Applied Digital | APLD | ~$2B | ~$200M | –$100M+ | No |

| Iris Energy | IREN | ~$3B | ~$400M | –$25M | Marginal |

Nebius produced $101.7 million of net income on $529.8 million of FY2025 revenue, with Q1 2026 stepping up to $399 million revenue (+684% year-on-year), $129.5 million of adjusted EBITDA, and a 45% adjusted EBITDA margin in the AI segment. CoreWeave produced roughly $5.1 billion of revenue but with a $1.2 billion net loss and widening operating losses as it brought new gigawatts online.

The gap is structural, not narrative. Three factors explain it. First, Nebius inherited cash from the Yandex divestment, so it built initial capacity off equity rather than debt. Second, the Microsoft and Meta deals were structured with customer prepayments funding the capex, which means Nebius is constructing AI factories partly on customer working capital. Third, Nebius's first big site sits in Mantsala, Finland, where it is expanding to 75 megawatts and where power costs are some of the lowest in Europe. CoreWeave levered up faster on debt, paid different power costs across its US footprint, and exited Nvidia GPU lease commitments at a larger scale.

The valuation reflection is uncomfortable in either direction. NBIS trades around 89.6x trailing price-to-sales versus CoreWeave at 10.6x. That ratio is hard to defend on FY2025 numbers alone. It becomes less extreme when measured against the $7–9 billion year-end ARR target Nebius is guiding for December 2026.

Capex, dilution, and the $25B question

The bear case nobody puts in the bull narrative lives in the capex line. FY2026 capex guidance from the Q1 earnings call is $20–25 billion. That number is bigger than the current cash position. The funding gap will be filled, but the gap exists, and it is large.

In April 2026, Nebius priced $2.75 billion of upsized 2.75% convertible senior notes. That issuance was the second large capital raise after the December 2024 equity round. Cash position at Q1 2026 is $9.3 billion, of which $2.3 billion is customer prepayments earmarked for capacity delivery and roughly $7 billion is free cash for general capex deployment. Against $20–25 billion of FY2026 capex, the implied incremental financing need is $10–15 billion in 2026, almost certainly raised through a combination of additional debt, further customer prepayments, and equity. Shares outstanding have already grown from approximately 196 million at relisting to 256 million today, a 30% dilution in eighteen months.

The 17.82% short interest reflects this math. A 1,186% increase in short interest since the October 2024 relisting is a positioning signal that institutional desks see asymmetric downside if AI capex demand softens, if GPU supply tightens further, or if customers like Microsoft and Meta accelerate their own owned-capacity construction at the expense of Nebius routing.

Benzinga aggregates a sell-side forecast consensus around $190, with Goldman Sachs on the bullish side, B. Riley more cautious, and several mid-cap desks at hold. The aggregate target sits below the $208 print, which suggests the rally has run ahead of formal models. I am not convinced most retail buyers at current levels have priced the next equity raise into their entry math.

What sits inside the rest of Nebius Group

NBIS is not a single-product technology company. The rest of the portfolio is under-discussed in coverage and worth a paragraph. Avride, the autonomous-driving business spun out of the former Yandex Self-Driving Group, received a strategic investment commitment of up to $375 million from Uber and Nebius in 2025 to expand autonomous robotaxi pilots. Toloka, the crowdsourced data-labelling platform, supports LLM training data pipelines for large AI labs and has been quietly compounding customer count. TripleTen, the edtech bootcamp business, is profitable on a standalone basis but smaller in scale. Sum-of-the-parts work on the bank-research side assigns $2 to $5 billion of aggregate value to the non-AI portfolio. The AI compute business carries the remaining $48 to $51 billion of the $53.4 billion market cap, which is the appropriate framing for any NBIS valuation question.

Bull and bear case scorecard for NBIS

The cleanest summary of the NBIS investment debate fits on one page. Bull: $44.4 billion contracted customer backlog, EBITDA profitable from Q1 2026, $9.3 billion in cash, Mantsala power-cost advantage, anchor Nvidia investment from December 2024, customer-prepayment funding model that pulls capex off Nebius's own balance sheet, AI factory campus capacity buildout under way in Finland and Kansas City. Bear: $20–25 billion of FY2026 capex against $7 billion of free cash creates a $10–15 billion financing gap; 30% dilution since the relisting; 17.82% short interest reflects institutional skepticism; concentration risk because Microsoft and Meta together represent the vast majority of contracted backlog; AI capex cycle risk if generative-AI demand growth slows; residual geopolitical noise from the Yandex origin story. The two cases use the same data and reach opposite conclusions, which is why the analyst spread is wide and the stock moves on every earnings print.

How to buy NBIS and option mechanics

Any investor looking up the NBIS stock quote and live data will find NBIS listed on Nasdaq under "Nebius Group NV" and available at every major US broker, including Fidelity, Charles Schwab, Robinhood, Interactive Brokers, and Webull. Fractional shares are supported on most platforms. Realised volatility keeps option premiums elevated, which makes covered-call writing a common active-trader approach on long positions. NBIS is not in the S&P 500 yet but is included in the Nasdaq Composite, and a secondary listing trades on the Frankfurt exchange under a separate code for European retail.

What NBIS at $208 actually prices

NBIS at $208 is pricing successful execution against a $44.4 billion customer backlog and a $20–25 billion FY2026 capex year. The bull case is the backlog converting to roughly $9 billion of annual revenue by FY2028, with EBITDA margins holding above forty percent through the ramp. The bear case is dilution and delivery risk — power siting in Finland and Kansas City, Blackwell-class GPU supply timing, and customer counter-construction by Microsoft and Meta themselves — while that conversion is supposed to happen. The honest question for any retail buyer is whether they think Nebius can deliver power, GPUs, and operating uptime against what is now the largest construction project in commercial AI cloud history. The market is currently pricing yes. The short side is pricing not so confidently, and that disagreement is what keeps NBIS stock trading around $200 instead of $300 or $80.