EBITDA Explained: Earnings Before Interest and Calculation

December 2024. The bitcoin miner CleanSpark posts its best fiscal year ever. Revenue $378.9 million, up 125%. Adjusted EBITDA of $245.8 million. The same release also discloses a GAAP net loss of $145.8 million. Two months later, Coinbase reports FY 2024 numbers of its own — $6.6 billion in revenue, $3.3 billion in Adjusted EBITDA, $2.6 billion in actual net income. Two very different financial stories. One headline metric ran across both releases. EBITDA.

That is the core puzzle. EBITDA stands for Earnings Before Interest, Taxes, Depreciation and Amortization. It shows up in every earnings release, every IPO filing, every leveraged buyout deck. It is also the metric Warren Buffett refuses to look at; he has called it pernicious in print, in different words, at least twice. The pages below walk through what EBITDA actually measures, the two formulas analysts use, what counts as a good margin, how Coinbase and Robinhood and the bitcoin miners actually report it, and where the famous critique starts to bite.

What EBITDA is and what it actually measures

EBITDA is a non-GAAP profitability metric. It sits outside the generally accepted accounting principles framework. The metric strips four specific items out of a company's earnings to exclude effects that have nothing to do with business operations. The acronym itself: Earnings Before Interest, Taxes, Depreciation, and Amortization. Each removal serves a purpose. Interest comes out to level the field between firms with different debt loads. Taxes come out to neutralise different jurisdictions. Depreciation and amortization are non-cash accounting charges, so taking them out moves the number closer to operating cash generation.

The origin story is unusually specific. John Malone, the cable executive who ran Tele-Communications Inc. through the 1970s and 1980s, popularised EBITDA to argue that capital-intensive cable systems threw off real cash even when reported net income was poor. Malone used the metric to push banks and to nudge Wall Street analysts off GAAP earnings. EBITDA then crossed into the mainstream during the 1980s leveraged buyout boom, where it doubled as a rough proxy for repayment capacity on highly indebted deals. The New York Times first referenced the acronym in print around 1991, describing it then as the most liberal cash-flow definition used by money-losing firms.

Today the metric is everywhere — every public-company income statement, every S-1, every LBO model. It still is not GAAP. The SEC restricts how public filers can present it under Regulation G, but the metric itself is not going anywhere. EBITDA sits between operating income and net income on the conceptual spectrum, and answers one specific question: how is the core business doing once financing decisions, the tax bill, and asset depreciation are taken off the table.

What EBITDA does not measure is the part most people skim over. It does not capture capital expenditure. For capex-heavy industries that is the whole game. It does not capture changes in working capital. It says nothing about how much cash arrives in the bank account at the end of the quarter. A company can post a positive EBITDA number and still be burning cash, missing payments, and on the road to default. The metric is a lens. The financial statements are the building.

How to calculate EBITDA: formulas with a worked example

There are two standard EBITDA formulas, and they should produce the same answer if the inputs are clean.

The bottom-up formula starts at net income and adds back the four removed items, so you do not subtract anything else from the line.

> EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

The top-down formula starts at operating income (also called EBIT, earnings before interest and taxes; closely related to earnings before taxes) and only adds back depreciation and amortization, since the two stand for items not yet deducted at that line.

> EBITDA = Operating Income + Depreciation and Amortization

Both calculations show up in different parts of the income statement. The first is what most beginners see in an Investopedia article. The second is cleaner for analysts because EBIT already excludes interest and tax, so only D&A remains to add back.

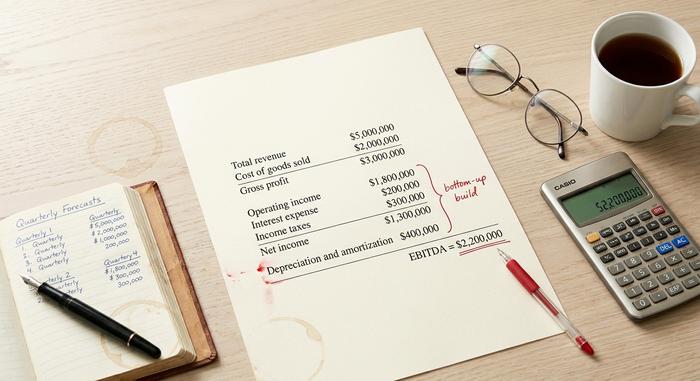

A short worked example. Imagine a small tech business reports the following on its annual financial statements:

| Line item | Amount |

|---|---|

| Total revenue | $5,000,000 |

| Cost of goods sold | $2,000,000 |

| Gross profit | $3,000,000 |

| Operating expenses | $1,200,000 |

| Operating income | $1,800,000 |

| Interest expense | $200,000 |

| Income taxes | $300,000 |

| Net income | $1,300,000 |

| Depreciation and amortization | $400,000 |

Bottom-up EBITDA calculation: EBITDA = $1,300,000 + $200,000 + $300,000 + $400,000 = $2,200,000. The amortization and depreciation lines are the only non-cash adjustments here. Top-down: $1,800,000 + $400,000 = $2,200,000. Same answer, two routes.

EBITDA margin is a simple extension. EBITDA margin = EBITDA / Total Revenue. In this example, $2,200,000 / $5,000,000 = 44%. EBITDA margin is the cleanest metric for cross-company comparisons because it normalises for size and lets you put a $50 million startup and a $50 billion incumbent on the same chart. Investors use EBITDA margin as a quick read on financial health and operating efficiency before they go any deeper.

Adjusted EBITDA goes one step further. The company adds back items it considers non-recurring or non-cash — stock-based compensation, M&A costs, restructuring charges, litigation, impairments, and sometimes crypto fair-value remeasurement. These adjustments are not GAAP-defined, which is exactly why they invite criticism. The SEC requires every public company that presents Adjusted EBITDA to reconcile it back to net income.

What is a good EBITDA margin in practice?

A good EBITDA margin varies by industry. Software at scale runs 30-40%, with the best of them above 45%. Grocers and most retailers live with 5-10%. Oil and gas sits closer to 15-25%. Crypto exchanges blew past most of those benchmarks in 2024-2025: Coinbase landed near 50% on FY 2024 revenue of $6.6 billion. Robinhood was 26.5% the same year, which is strong for a regulated US broker, and the company doubled it again in 2025.

The rough rule of thumb. Above 20% is solid for most industries. Above 30% is excellent. Above 50% either signals a software-like business with real network effects, or a metric that has quietly stopped counting real costs. Bitcoin miners are the cleanest example of the second trap.

EBITDA in crypto: exchanges, miners and FASB ASU 2023-08

In crypto, almost every public-company report leads with Adjusted EBITDA. The reason is partly genuine and partly spin. The genuine part is that crypto businesses carry digital assets on balance sheets and the GAAP treatment of those assets has been violently noisy. The spin part is that Adjusted EBITDA flatters miners whose ASIC fleets need replacing every three years.

Take the 2024-2025 picture across the industry.

| Company | Period | Adjusted EBITDA | Revenue | Margin |

|---|---|---|---|---|

| Coinbase (COIN) | FY 2024 | $3.3 billion | $6.6 billion | ~50% |

| Coinbase (COIN) | Q3 2025 | $801 million | $1.9 billion | ~42% |

| Coinbase (COIN) | Q4 2025 | $566 million | n/d | n/d |

| Robinhood (HOOD) | FY 2024 | $613 million | ~$2.31 billion | 26.5% |

| Robinhood (HOOD) | FY 2025 | $2.5 billion | n/d | n/d |

| MARA Holdings | Q4 2024 | $794 million | n/d | n/d |

| Riot Platforms | FY 2024 | $463 million | n/d | n/d |

| Riot Platforms | FY 2025 | ~$13 million | $647 million | ~2% |

| CleanSpark (CLSK) | FY 2024 | $245.8 million | $378.9 million | ~65% (with $145.8M GAAP net loss) |

| Bitfarms (BITF) | FY 2024 | $31 million | ~$135 million | 23% |

| Block (XYZ) | Q4 2024 | $757 million | n/d | n/d |

Two patterns jump out. Robinhood's growth is the clearest fundamental story, with Adjusted EBITDA up roughly 300% in 2024 to $613 million and another 76% to $2.5 billion in 2025. Coinbase remains the EBITDA-margin king at the exchange level, hitting around 50% in FY 2024. The miners are messier. CleanSpark printed $245.8 million in Adjusted EBITDA and a $145.8 million GAAP net loss in the same year, which is exactly the gap Buffett's critique was built for. Riot Platforms went from $463 million to roughly $13 million between FY 2024 and FY 2025, which shows how fragile EBITDA is when bitcoin price, hash rate and difficulty all shift at once.

The other 2024-2025 wrinkle is FASB ASU 2023-08. The Financial Accounting Standards Board issued the rule in late 2023, and it took effect for fiscal years beginning after December 15, 2024. It requires companies to mark digital assets to fair value through net income, replacing the legacy ASC 350 impairment-only model. For Strategy (formerly MicroStrategy), the change has flipped GAAP earnings into wildly volatile territory, which is why the market now reads its software-segment Adjusted EBITDA separately from the bitcoin mark-to-market line. Cumulative pre-FASB BTC impairment under the old rule had reached $2.27 billion. The new rule fixed that, and made Adjusted EBITDA the metric that survives the noise.

EBITDA also shapes how the equity market values miners. As of 2025, Hashrate Index data shows MARA trading around 9x EV/EBITDA, TeraWulf at 24.2x because of its AI/HPC pivot on roughly 430 MW of capacity, and HIVE near 1.3x on a BTC-adjusted basis. The same metric, applied to the same industry, produces a 19x spread depending on how you treat the bitcoin holdings on the balance sheet.

Adjusted EBITDA, EBITA and other variants

The EBITDA family keeps growing. EBITA is EBITDA without the depreciation add-back, used in industries where amortization is the only non-cash charge that matters. EBITDAR adds rent back on top of EBITDA, common in restaurants, casinos and airlines that lease most of their assets. EBITDAC was a brief 2020 invention by the German engineering firm Schenck Process for "Earnings Before Interest, Taxes, Depreciation, Amortization and Coronavirus", a serious lender pitch that briefly became a finance Twitter joke.

Adjusted EBITDA is the version every public crypto company actually reports. The standard adjustments include stock-based compensation, M&A and restructuring costs, litigation expenses, asset impairments and, increasingly, crypto fair-value remeasurement. The exact list is company-specific. It is a non-GAAP measure, which is why the SEC requires a reconciliation to GAAP net income whenever a public company presents it. Reconciling Adjusted EBITDA back to net profit is the part where serious investors do their work — and it is what every analyst should look at before they look at EBITDA itself. The headline number is the marketing.

EBITDA in business valuation: EV/EBITDA multiples

Valuation is where EBITDA gets the most reps. The standard multiple is EV/EBITDA. Enterprise value (market cap, plus debt, minus cash) sits in the numerator. EBITDA sits in the denominator. The ratio strips out leverage and lets you put two acquisition targets side by side.

Quick example. Two grocery chains in New York. Similar revenue. Reasonable margins. Company A: EV $200M, EBITDA $10M, multiple 20x. Company B: EV $300M, EBITDA $30M, multiple 10x. Same industry, half the multiple. The buyer pays less per dollar of earnings at Company B, all else equal. That is the whole game.

Typical EV/EBITDA bands run 5x to 15x. Software and high-growth names trade higher. Capital-intensive cyclicals trade lower. Lenders watch debt to EBITDA on top of all this; anything above 4-5x usually flags as overlevered for a non-financial firm. Crypto exchanges and brokers have moved in the 8x to 20x band when EBITDA was positive. Bitcoin miners broke that pattern in 2025, with the WULF and HIVE spread showing investors valuing an AI hosting story on top of the underlying mining cash flow. EBITDA opens that conversation. It never closes it.

Why Buffett hates EBITDA — and what critics get right

Warren Buffett has been disagreeing with EBITDA in print for twenty-five years. His 2000 Berkshire shareholder letter asked, in a now-famous phrase, "Does management think the tooth fairy pays for capital expenditures?" His 2002 letter went further, calling EBITDA "a particularly pernicious practice" because it implies depreciation is not a real expense. His 2024 letter, released in February 2025, summarised the position in a sentence: "EBITDA, a flawed favorite of Wall Street, is not for us." Charlie Munger called it bullshit earnings.

The legitimate point inside the polemic is real. EBITDA hides capital expenditure, and for asset-heavy businesses capex is the actual cash cost. A bitcoin miner that depreciates a $300 million ASIC fleet over three years has to spend another $300 million every three years to stay competitive after the next halving, and Adjusted EBITDA tells you nothing about whether that future capex is funded. I keep coming back to the CleanSpark example for that reason. The metric is useful, the headline can mislead, and the audited cash-flow statement is still where the truth lives.