Oklo Stock 2026: AI Power Bet, Altman Risk, Zero Revenue

Oklo stock has been one of the loudest trades on the NYSE for two years and one of the strangest. The company has not sold a kilowatt-hour to a paying customer. It does not yet have a single operating reactor. Its combined operating license application with the Nuclear Regulatory Commission is still pre-submission. And the market cap sits north of $11 billion. The cleanest way to make sense of OKLO in 2026 is to track three threads at once: the artificial-intelligence power thesis pulling the price up, Sam Altman's conflict of interest pulling the governance story sideways, and a pre-revenue valuation gap pulling skeptics in. This guide walks through each of them and shows how they connect to the headline numbers.

What Oklo is and how OKLO got listed

Oklo Inc was founded in 2013 in Santa Clara, California by Jacob DeWitte and Caroline Cochran, both MIT-trained nuclear engineers. The company designs a sodium-cooled fast-spectrum reactor it markets as the Aurora Powerhouse, with target output ranging from roughly 1.5 to 50 megawatts electric per unit. Aurora is intended to ship as a factory-built, modular fission power plant, sited near the customer rather than on a traditional utility grid. Oklo went public on May 9, 2024, through a merger with AltC Acquisition Corp, the SPAC vehicle sponsored by Sam Altman. The transaction generated $306 million in gross proceeds and carried an aggregate deal value of about $875 million at closing. The combined company began trading on the NYSE under the ticker OKLO that same week. The SPAC structure matters because it set the share count and capital base that the company has been diluting against ever since.

Oklo stock price action 2024–2026

The Oklo stock price chart reads less like a line and more like three regimes stitched together. SPAC pricing sat around $10 at the May 2024 closing. By September 9, 2024, the stock had drifted to an all-time low of $5.35 amid post-merger redemption pressure. Then the AI-power narrative took over. OKLO climbed steadily through late 2024, accelerated through 2025, and printed an all-time high of $193.84 on October 15, 2025, roughly a 36-fold move in 13 months. The recent stock quote in late May 2026 sits around $67 to $69, off about 65% from the high but still up 6x to 7x from the SPAC price. The 52-week range is $44.88 to $193.84. Market capitalization sits between $11.5 billion and $11.8 billion depending on intraday print and source. Shares outstanding are roughly 174 million after a 28% increase over the trailing twelve months, almost all of it from at-the-market equity issuance. Average weekly price swing is around 14%, which puts OKLO in the most volatile quartile of the US market.

The AI power thesis: where the bull case actually lives

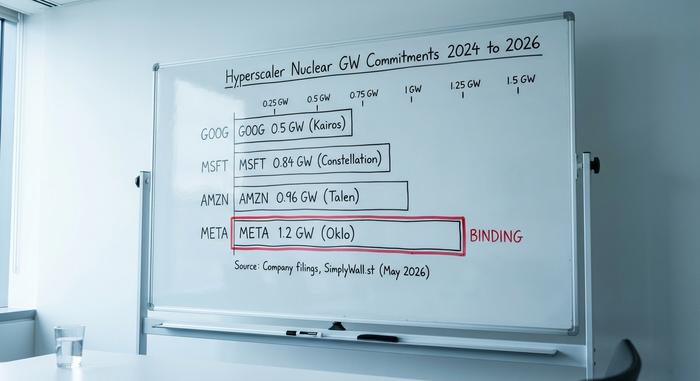

The Oklo bull case is not "nuclear is back". It is a specific bet that hyperscaler data-center electricity demand, measured in steady gigawatts rather than peak megawatts of electricity, will pull forward the commercial timeline for small modular reactors and deliver firm energy at scale half a decade earlier than utility planners expected. The supporting data points are concrete, and they have arrived fast.

Microsoft announced its Three Mile Island restart through Constellation in September 2024, contracting 835 megawatts for roughly $1.6 billion over twenty years. Amazon went vertical the same year with a 960 MW colocation deal at Talen's Susquehanna plant. Google signed a 500 MW SMR power purchase agreement with Kairos Power in October 2024. Meta ran an open nuclear request-for-proposal through early 2025 and, according to SimplyWall.st's reporting, has since put a 1.2 GW binding agreement in place with Oklo specifically. That last data point is the single most consequential one in the Oklo investment case.

Oklo's broader pipeline, framed as a 14 GW order book, is mostly something else. The headline Switch deal, signed December 18, 2024, is a 12 GW non-binding Master Power Agreement targeting first deployment in 2029 at the earliest. Equinix put down a prepayment that has not been traced cleanly to a primary SEC filing. The Vertiv collaboration covers power-and-cooling solutions for hyperscaler sites but is a development partnership, not a purchase order. And the US Air Force selected Oklo in June 2025 for an Eielson AFB pilot covering up to 75 MW on a 30-year firm-fixed-price PPA, with target online date 2028. This is Oklo's second attempt at Eielson after the 2023 award was cancelled.

The distinction that retail investors keep missing is which of those headline gigawatts will actually convert to revenue and when. The binding capacity is probably 1 to 2 GW — anchored by Meta and the Air Force pilot. The remaining 12+ GW lives in framework agreements that can be expanded, modified, or quietly walked away from. The gap between the binding column and the headline column is the entire bull-bear debate compressed into one number.

Sam Altman's conflict and why he resigned the chair

Most secondary coverage treats Sam Altman's April 24, 2025 resignation as a governance correction. The available reporting suggests the opposite. NucNet and other primary outlets framed the departure as "clearing the way for supply talks with AI companies", which is a direct acknowledgement that the conflict was blocking, not enabling, a commercial transaction.

The mechanics are worth slowing down on. Altman was chairman of Oklo from the AltC SPAC closing through April 2025, while simultaneously serving as CEO of OpenAI. A related-party transaction between two entities the same person controls cannot close cleanly: independent directors on both sides have to negotiate, fairness opinions have to be obtained, and disclosure obligations under Item 404 of Regulation S-K force the executive's involvement into the prospectus. The cheapest fix is for the executive to step back from one side. That is what Altman did.

The reframing matters for the equity. Under the standard "Altman left because of governance pressure" reading, his departure is a neutral-to-positive signal. Under the actual reading, where the conflict was a commercial blocker, his departure is a leading indicator that a specific revenue contract was being shaped at the time. If that contract is the OpenAI–Oklo supply deal that supply-chain reporters have hinted at since mid-2025, the value-creating event for OKLO is the deal landing on paper. The value-destroying event is the deal failing to land once the path was cleared. Either outcome will move the stock more than any analyst price target. I am not sure most retail buyers of OKLO understand that they are pricing a binary.

Altman's actual ownership percentage as of May 2026 is not publicly confirmed; the most recent fully reported figure is the SC 13G/A filing tied to the AltC SPAC closing. The current 2026 number will surface in the next proxy circular.

Pre-revenue valuation: what does $11.5B on $0 sales actually price

Oklo's market capitalisation in late May 2026 sits in the $11.5 billion to $11.8 billion range. Revenue on a trailing-twelve-month basis is essentially zero. Net loss TTM is $128.9 million. Operating loss for fiscal year 2025 came in at $139.3 million per the 10-K filed February 2026. Cash on hand is $2.54 billion following the $1.18 billion ATM offering completed in May 2026, which gives roughly seven to eight years of runway at the current burn rate.

The cleanest way to test whether $11.5 billion is the right price is peer comparison.

| Company | Ticker | Market cap (May 2026) | Revenue (TTM) | NRC status |

|---|---|---|---|---|

| Oklo | OKLO | $11.5B | ~$0 | Pre-application |

| NuScale Power | SMR | $4.2B | ~$25M | NRC-certified design (only one) |

| X-energy | private (IPO Apr 2026) | $9.1B at IPO | ~$0 | Pre-application |

| NANO Nuclear | NNE | ~$1.5B | ~$0 | Pre-application |

| Centrus Energy | LEU | ~$3.5B | $400M+ | HALEU fuel producer |

| BWX Technologies | BWXT | ~$11B | $2.6B | Reactor builder |

Two facts in that table do the analytical work. The first is that NuScale, the only SMR developer with an NRC-certified design, trades at roughly one-third of OKLO's market cap. That is the cleanest bear sentence available: an actually-licensed product is priced at $4.2 billion, while a pre-licensed product — Oklo — is priced at $11.5 billion. The second is BWX Technologies, an established reactor builder with $2.6 billion in real revenue, sitting at roughly the same market cap as Oklo. Either OKLO is the most-priced option on the SMR theme, or the market is implicitly discounting every other peer for not having the Altman halo.

Sell-side spread reflects the debate. Consensus 12-month price targets cluster from $88.89 (StockAnalysis, 23 analysts) up to $112.13 (SimplyWall.st aggregate, 38.7% upside). That is wide enough that the rating itself is doing less work than the assumption behind each model. The honest analyst conversation about Oklo is not about the next quarter. It is about which year the first commercial gigawatt actually flips on.

Latest Oklo news: milestones and the DOE plutonium decision

Oklo's last six months have moved faster than any prior period in its public life. The NRC Readiness Assessment was completed in early 2025. In May 2026, the NRC approved Oklo's Principal Design Criteria topical report on an accelerated timeline. This is a procedural advance, not a license, but it is the first time the agency has signalled comfort with the Aurora design framework. Q1 2026 results, reported May 12, 2026, confirmed an expanded NVIDIA partnership focused on AI-powered reactor monitoring and design simulation. On May 13, the company filed a $1.0 billion ATM equity offering, the second large ATM raise in twelve months. On May 26, 2026, the Department of Energy named Oklo as the intended awardee under its Surplus Plutonium Utilization Program, securing a path to plutonium-derived feedstock for early Aurora units. The Aurora design supports used nuclear fuel recycling, which is how the DOE's surplus inventory becomes commercially relevant fuel. Each of those milestones moved the share price by a single-digit percentage in the day session. None of them moved revenue, which remains zero.

The bear case: short interest, dilution, and the NRC clock

The bear case for OKLO does not require disliking nuclear power. It just requires reading the cap table and the regulatory timeline. Short interest stood at 18.84% of float as of May 2026, up from 10.9% in January. Insiders were net sellers of roughly $39 million over the trailing twelve months. Dilution from secondary offerings ran 28% over the same window. Analyst forecasts do not project profitability inside a three-year horizon. The independent NRC combined-license timeline that practitioners actually use does not reach a commercial deployment before 2028, and several scenarios push first power past 2030. Construction, fuel-supply, and siting risks remain stacked on top of the licensing clock. Trading OKLO around current levels is, in effect, trading a multi-year option on a regulatory and engineering schedule that has historically slipped.

How to buy Oklo stock and the practical mechanics

OKLO is listed on the NYSE and is available through every major US broker, including Fidelity, Charles Schwab, Robinhood, Interactive Brokers, and Webull. Fractional shares are supported on most platforms. Realised volatility keeps option premiums rich, so a buy-write strategy is one common way active traders position the name. OKLO is not in the S&P 500, which limits passive index exposure. Coinbase lists OKLO through its tokenised-equity feature for non-US users, which is context for international readers rather than a recommendation.

What the price chart actually prices

Oklo stock at $68 is not pricing a nuclear reactor. It is pricing an option on a nuclear-reactor decade, anchored by a binding Meta gigawatt commitment and a cleared path for an OpenAI supply contract. The option has eight years of cash runway behind it, an NRC clock in front of it, and a major shareholder structure that just removed the largest related-party blocker. The honest question for any retail buyer is which year the first commercial kilowatt-hour books revenue. The market is treating that answer as if it is 2029. The independent engineers in the room are not yet sure.