Monzo vs Revolut: Which Digital Bank Wins in 2026?

Monzo and Revolut started in the same place — same year, same city, same target customer fed up with their legacy bank. Pick either card up now and you'll notice how different they've become. Revolut is a multi-currency trading app that also does banking. Monzo is a bank that happens to have a great app. Choosing the wrong one for your situation isn't catastrophic, but it costs you: on ATM fees, savings rates, and features you expected to be there. This monzo vs revolut breakdown covers each category so you can work out which one actually fits.

Monzo and Revolut: Two Challengers, One Big Question

They started in the same lane. Monzo concentrated on the UK, got its banking licence in 2017, and spent the years since building out current accounts, credit tools, and budgeting. Revolut went the other direction — pushing into 50+ countries, bolting on crypto trading, stock investing, and multi-currency wallets, before eventually picking up its UK banking licence in 2024.

Here's where both stand today:

| Monzo | Revolut | |

|---|---|---|

| Founded | 2015, London | 2015, London |

| UK customers | ~14 million | ~10 million |

| Global users | UK-focused | ~70 million |

| UK banking licence | Since 2017 | Since 2024 |

| FSCS protection | Yes (£85,000) | Yes (£85,000) |

| Free tier | Yes | Yes |

| Paid tiers | 3 (Extra, Perks, Max) | 4 (Plus, Premium, Metal, Ultra) |

| Crypto trading | No | Yes (100+ coins) |

| Countries available | UK + select expansion | 50+ countries |

The banking licence gap is worth spelling out. Until 2024, Revolut ran as an e-money institution, not a bank. Your deposits sat in safeguarded accounts but had no FSCS coverage at all. Revolut's 2024 licence changed that, and now both banks protect balances up to £85,000. Most articles on this topic skip over that history entirely.

Account Plans and Monthly Fees Compared

Both run a free current account with paid tiers on top. The structures differ more than they look at first glance.

Monzo tiers:

| Plan | Monthly fee | Key features |

|---|---|---|

| Standard | Free | Current account, debit card, budgeting tools, pots |

| Extra | £3 | 2 additional pots, cashback on selected retailers |

| Perks | £7 | Discounts and cashback on brands, higher savings rates |

| Max | £17 | Travel insurance, phone insurance, cashback, highest savings rate |

Revolut tiers:

| Plan | Monthly fee | Key features |

|---|---|---|

| Standard | Free | Multi-currency account, crypto trading, instant transfers |

| Plus | £3.99 | Priority support, event ticket protection |

| Premium | £7.99 | Travel insurance, higher ATM limits, overseas medical cover |

| Metal | £14.99 | RevPoints, lounge access, cashback, concierge, metal card |

| Ultra | £45 | Top-tier perks, highest limits, exclusive rewards |

Revolut's premium account tier goes much higher — Ultra at £45 a month is nearly three times what Monzo charges for Max. Monzo's Max at £17 undercuts Revolut Metal at £14.99 by a small margin but includes travel insurance and phone insurance that Revolut only adds at higher tiers.

Start on the free plans. Both work well without paying a penny. Move up only when a specific paid feature solves a real problem in your life, not because a longer feature list sounds appealing.

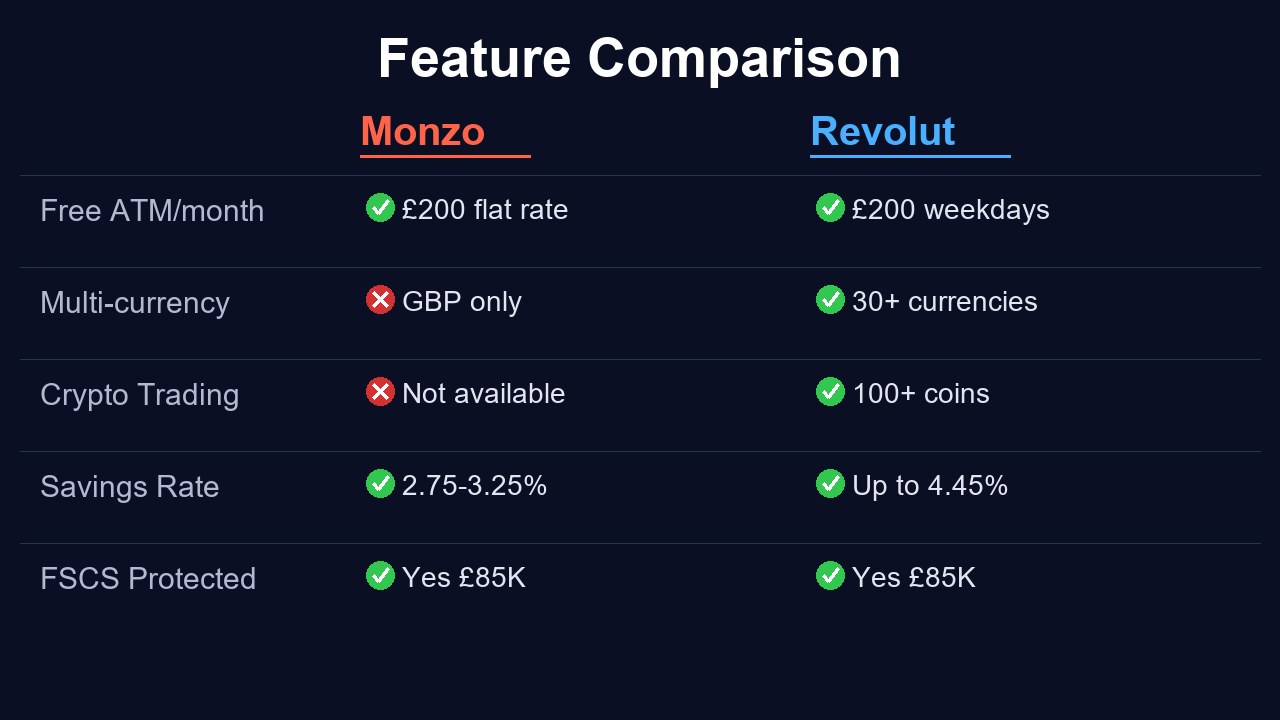

ATM Withdrawals and Cash Access Rules

Free ATM withdrawals sound identical across both banks. They're not, and the difference catches people out on holiday.

Monzo gives you £200 per month fee-free, whether you're in the UK, the EEA, or somewhere further afield. After that it charges 3%. The Mastercard exchange rate applies every day of the week with no markup.

Revolut also gives you £200 free per month on Standard, then charges 2% with a £1 minimum after the limit. Two percent sounds better than three, but Revolut adds a weekend FX markup of 0.5–1% on currency conversions, ATM withdrawal included. Pull cash on a Sunday in Lisbon and you're paying the headline rate plus that markup on top.

| Monzo Standard | Revolut Standard | Revolut Premium | Revolut Metal | |

|---|---|---|---|---|

| Free ATM/month | £200 | £200 | £400 | £800 |

| Fee after limit | 3% | 2% (min £1) | 2% (min £1) | 2% (min £1) |

| Weekend FX markup | None | 0.5–1% | 0.5–1% | 0.5–1% |

| Max free withdrawals | 5/month (Standard) | Unlimited to limit | Unlimited to limit | Unlimited to limit |

The weekend markup is the number most travellers find out about after the fact. If you're spending foreign currency on a Saturday or Sunday with Revolut Standard, build that extra cost into your expectations.

Spending Abroad and Currency Exchange

The monzo vs revolut fight gets loudest here, mostly because of that weekend FX issue.

Card payments abroad are fee-free on the standard plan of either bank. Both use Mastercard's exchange rate as the base rate. Where they split is currency conversion.

Revolut lets you hold 30+ currencies in the app. Load up euros before a trip and your spending draws from that balance directly, no conversion at the point of sale. On weekdays, Revolut uses the interbank rate, which is tighter than Mastercard's. On weekends, it applies that 0.5–1% markup.

Monzo keeps everything in GBP. Each foreign transaction converts at Mastercard's real-time rate, consistently, seven days a week. There's no in-app currency exchange, but there's no weekend penalty either.

For a £1,000 holiday spend, the difference between the two approaches is a few pounds at most. For someone running payroll across currencies or paying international suppliers, Revolut's multi-currency holding is genuinely useful. Both support Apple Pay and Google Pay, so paying contactlessly is never an issue regardless of which you carry.

Savings Rates and Interest in 2026

Neither is the highest-yield savings account available in the UK. Both beat most high-street banks on instant-access rates, which is the relevant comparison for money you want available quickly.

Revolut's savings rates depend entirely on which plan you're on:

| Revolut plan | Savings AER |

|---|---|

| Standard | ~3.0% |

| Plus | ~3.5% |

| Premium | ~4.0% |

| Metal | ~4.45% |

| Ultra | ~4.45% |

Monzo's pots pay 2.75%–3.25% AER based on your tier, with Max users getting the top rate. All pots are instant access with no withdrawal penalty.

Round-up savings work on both apps: every purchase rounds to the nearest pound, with the difference moved into a pot automatically. Revolut adds shared savings vaults, which works well for couples or households with joint goals.

If you're on Revolut Standard, your savings rate is roughly the same as Monzo's. Pay for Metal and the gap widens noticeably, but that £14.99 monthly fee has to be weighed against what you'd actually earn on the balance you're keeping there.

Perks, Rewards and Premium Features

Revolut has built a loyalty programme. Monzo has built a benefits package. They reward you in different ways, and which you prefer depends on how you actually spend.

Monzo paid tier perks:

- Cashback at selected retailers (Perks and above)

- Partner discounts (cinema, gym, entertainment)

- Travel insurance for the account holder (Max)

- Phone insurance (Max)

- Higher interest on savings pots

Revolut Metal perks:

- RevPoints earned on every purchase (redeemable for travel, experiences, or vouchers)

- Cashback on purchases (0.1% standard, up to 1% on Metal)

- Travel insurance and overseas medical cover

- Airport lounge access (Smart Delay: triggered when your flight is delayed 1+ hour)

- Concierge service

- Physical metal card

RevPoints is Revolut's version of a travel rewards programme. You earn points on everyday spending and redeem them for flights, hotels, or experiences through the app. It's not as rich as a dedicated airline card, but it's more than most banks offer.

Monzo's cashback at specific retailers is useful, but it's transactional rather than accumulative. You don't build up a balance to redeem; you get money back on purchases you'd have made anyway. No points to track, no expiry to watch.

Paying £14.99 for Metal and regularly travelling? Revolut has the edge. Want to know exactly what you're getting each month without managing a rewards account? Monzo Max is less work.

Security, FSCS Protection and Safety

Both banks now carry FSCS protection up to £85,000. The road to that status was different.

Monzo got its full UK banking licence in 2017. Deposits have been protected since the start.

Revolut ran as an e-money institution from launch until its UK banking licence came through in 2024. Before that, customer funds sat in safeguarded accounts, legally separate from the company's own money but not covered by FSCS. The licence changed that entirely.

Security features both offer:

- Biometric login (fingerprint and face ID)

- Instant card freeze via the app

- Virtual card numbers for online shopping

- Real-time transaction notifications

- Location-based security (disable the card outside your home country)

Revolut has built anti-fraud AI that flags unusual spending patterns and offers disposable virtual card numbers for one-off online purchases. Monzo runs Monzo Flex, a buy-now-pay-later product with spending controls built in and a cleaner repayment tracker than most BNPL services.

On customer support, Monzo pulls ahead. Trustpilot scores at time of writing: Monzo around 4.3, Revolut around 4.1. User reports back this up — Monzo tends to handle disputed transactions and fraud claims faster, with actual human agents rather than automated first responses. Revolut's support has improved since the banking licence landed but still draws more complaints.

Monzo vs Revolut for Business Accounts

For freelancers and small businesses, the monzo vs revolut comparison looks quite different. These are not the same product serving different scales — they target different types of business entirely.

Monzo Business:

- Free tier and Pro (£5/month)

- GBP-only accounts

- Integrations with Xero and FreeAgent for accounting

- Overdraft available on application

- Simple invoice tracking within the app

- Batch payments up to 200

Revolut Business:

- Four tiers: Basic (free), Grow (£19/mo), Scale (£79/mo), Enterprise

- Multi-currency accounts in 30+ currencies

- Bulk payments up to 1,000 per batch

- API access for automation

- Corporate cards with spend controls

- International transfers at interbank rates

Monzo Business is clean, well-integrated, and suited to UK-focused businesses that want solid accounting sync and a straightforward current account. Revolut Business is closer to a treasury tool — it makes sense for companies paying international suppliers, managing payroll in multiple currencies, or processing high transaction volumes.

Neither handles crypto payment acceptance from customers. If your business needs to accept Bitcoin, Ethereum, or stablecoins, you need a dedicated cryptocurrency payment gateway running alongside your bank account. Neobanks deal in fiat; crypto payment infrastructure sits on a separate layer entirely.

| Monzo Business | Revolut Business | |

|---|---|---|

| Free tier | Yes | Yes (Basic) |

| Multi-currency | No (GBP only) | Yes (30+ currencies) |

| Accounting integrations | Xero, FreeAgent | Xero, QuickBooks, others |

| Batch payments | Up to 200 | Up to 1,000 |

| API access | Limited | Yes |

| Overdraft | Yes | No (on lower tiers) |

| Best for | UK SMEs, freelancers | International businesses |

Which Is Better for Travelling Abroad?

This was the original selling point for both products. It's still where many people first discover them.

Where Revolut wins:

- Multi-currency accounts let you lock in rates before a trip

- Higher ATM limits on paid tiers (up to £800/month free on Metal)

- Airport lounge access on Metal and Ultra (via Smart Delay)

- Wider acceptance globally due to 50+ country availability

Where Monzo wins:

- No weekend FX markup — Mastercard rate applies 24/7

- Simpler experience: no currency management needed

- Better customer support if something goes wrong abroad

- Accepted everywhere Mastercard is (which is everywhere)

Recommendation by traveller type:

- Occasional UK holidaymaker — Monzo Standard or Revolut Standard; both work equally well for a week in Spain or Greece

- Frequent international traveller — Revolut Premium or Metal for better ATM limits, travel insurance, and multi-currency holding

- Long-term nomad or expat — Revolut for its global footprint, but keep a Monzo account for UK payments and direct debits

- Business traveller with FX exposure — Revolut Business for multi-currency accounts and interbank transfer rates

Either way, don't use a standard high-street bank account abroad. The savings on fees compared to a traditional UK bank's foreign transaction charges are real from day one.

Monzo or Revolut — Which Should You Choose?

A lot of people use both at once, and that's a perfectly sensible approach. Monzo as the main UK current account, direct debits, and customer service backup. Revolut for travel, FX, and investment features. Running both free tiers costs nothing.

If you're picking one:

| Use case | Winner |

|---|---|

| Daily UK banking and direct debits | Monzo |

| Travel spending and currency exchange | Revolut (Premium+) |

| Best savings interest rate | Revolut (if on Metal/Ultra) |

| Business — international operations | Revolut Business |

| Business — UK SME and freelancers | Monzo Business |

| Customer support quality | Monzo |

| Crypto trading in-app | Revolut |

| Simplest experience overall | Monzo |

| Most features per pound | Revolut Metal |

Try the free tier that matches your main use case. Give it 30 days. Upgrade only when a specific paid feature solves something you're actually running into.

For businesses that need capabilities neither bank offers — particularly accepting crypto payments from customers — a dedicated solution is the right tool. If you're working through the options, how to choose a cryptocurrency payment gateway is a useful starting point. Plisio supports 100+ cryptocurrencies with low fees and a straightforward API, covering what Monzo and Revolut leave open for merchants.

The monzo vs revolut question doesn't have one right answer. Both are good. The one that fits is the one that matches how you move money day to day — not the one with the longer list of features on the pricing page.