IonQ Stock: What You Get Buying IONQ Inc in 2026

Start with one number that should give any buyer pause. As of June 3, 2026, IonQ stock traded around $68.23, while the average price target from the analysts who cover it sat near $67.64. The crowd has already paid more for the shares than the people whose job is to forecast them think they are worth. That gap is the whole question in miniature: when you buy IONQ, are you buying a quantum-computing leader with real momentum, or a sentiment trade that has run ahead of its own story? Both readings are defensible, and that tension is exactly what makes this one of the most interesting and dangerous names on the market.

What IonQ Inc Actually Does for a Living

IonQ stock is not a meme with a ticker. It is a real company that sells access to real quantum computers and books real revenue for it. It is also tiny, deeply unprofitable, and selling a technology most customers cannot yet use at production scale. Holding both of those facts at once is the only honest way to read the stock.

Trapped-ion quantum computing, in plain terms

A classical computer stores information in bits that are either zero or one. A quantum computer uses qubits, which can hold a blend of both until measured, and that property is what could one day let these machines solve problems no normal computer can touch. IonQ builds its qubits from individual charged atoms held in place by electromagnetic fields, an approach called trapped-ion. The company reports a two-qubit gate fidelity of 99.99%, and it markets its progress through a metric it calls #AQ, or algorithmic qubits, which tries to measure how large a useful algorithm a machine can actually run rather than just counting raw qubits. The trapped-ion route trades some speed for accuracy, which is the bet IonQ is making against the superconducting designs that rivals like IBM and Google favor.

How IonQ makes money

The revenue comes from a few places. IonQ sells cloud access to its quantum computers through Amazon Braket, Microsoft Azure, and Google Cloud, so a developer can rent time on a machine without owning one. On top of that sit direct contracts, often with government and defense customers such as the Air Force Research Laboratory, plus consulting work tied to building quantum computing systems. The company was founded in 2015, spun out of research at the University of Maryland, and is headquartered in College Park, Maryland. It is increasingly pitching its hardware as infrastructure for the AI era, where certain optimization and chemistry workloads could favor quantum machines.

It is worth being clear-eyed about scale, though. The cloud-access model means a researcher might spend a few thousand dollars running an experiment, not the millions a finished enterprise system would command. Much of today's revenue leans on government, defense, and research contracts rather than a broad base of paying commercial customers. That is normal for a frontier technology, but it means the customer base is narrow, and a single large contract slipping can swing a quarter.

The roadmap and the M&A spree

IonQ is not waiting quietly. It has been buying its way up the stack, agreeing to acquire the British qubit specialist Oxford Ionics for roughly $1.075 billion and moving to buy chipmaker SkyWater in a deal valued near $1.8 billion. The logic is vertical integration: own the fabrication, the qubits, and the cloud layer instead of renting them. If it works, IonQ controls its supply chain and its costs in a way a pure cloud vendor never could. The ambition is real. So is the cost, and most of it is being paid in stock, which brings us to the part of the story the quote pages tend to skip.

IonQ Stock Price, Revenue and the 2026 Numbers

Here the story splits in two. The revenue line is genuinely impressive. The profit line is not, and one quarter's headline figure is close to fiction.

Revenue is real and accelerating

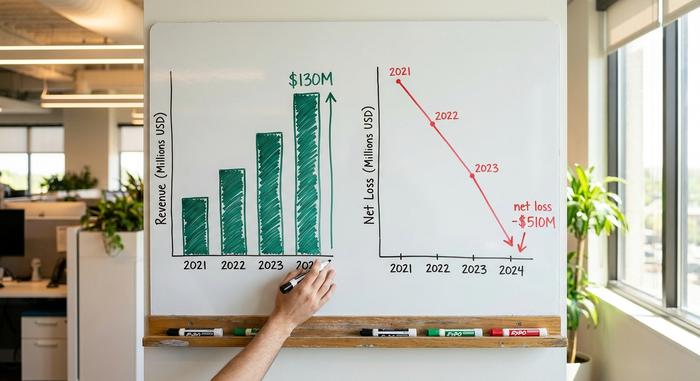

This is the part bulls are right about. First-quarter revenue for 2026 came in at $64.7 million, up about 755% year-over-year, according to IonQ's investor relations. Full-year 2025 revenue was $130 million, up roughly 202% from the year before, and management raised 2026 guidance to a range of $260 to $270 million. Remaining performance obligations, a rough proxy for booked future work not yet recognized as revenue, reached $470 million, up more than 550%. Revenue growth at that pace is not nothing, and the rising backlog suggests demand is not a one-quarter fluke. For a company this young, it is a real signal that customers are paying, and paying more each quarter. The honest caveat: growing 755% off a small base is far easier than sustaining it, and the law of large numbers will bite as the figures climb.

The profit that isn't

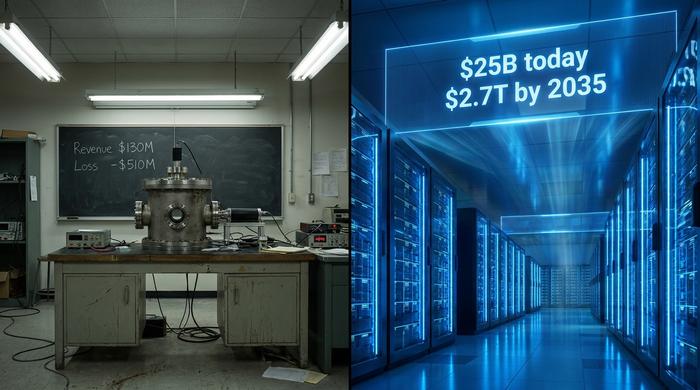

Now the other side. Full-year 2025 brought a net loss of $510.4 million, per IonQ's annual 10-K filing. You may have seen headlines about a roughly $805 million net income in the first quarter of 2026. Ignore it. That number is almost entirely a non-cash accounting swing from revaluing warrants, not money the business earned. Strip it out and the core operating loss for the quarter was about $271.5 million. Even on an adjusted EBITDA basis, which flatters most growth companies, IonQ still runs a loss. Stock-based compensation alone ran near $128 million in the quarter. The company is spending far more than it earns to grow, which is normal for the stage, but the GAAP profit that flashed across screens was an illusion, and almost none of the quote pages covering this stock will tell you that.

Cash and dilution

The good news is that IonQ is not about to run out of money. It held roughly $3.1 billion in cash and investments after a $2 billion equity raise in October 2025. The bad news is how it got there and how it pays for acquisitions: by issuing shares. Shares outstanding have climbed to around 373 million, and every stock-funded deal and capital raise spreads ownership thinner. Think of it this way: even if the business doubles in value, your slice of it can shrink if the share count keeps growing at a similar pace. That is the quiet cost behind the exciting headlines, and it is why dilution belongs at the center of any IONQ thesis, not in a footnote. The stock trades on the NYSE under the ticker IONQ, not on the Nasdaq, and it is a U.S.-listed common share, not a fund.

| IONQ snapshot (as of early June 2026) | Figure |

|---|---|

| Share price | ~$68.23 |

| Market cap | ~$25.5 billion |

| 52-week range | $25.89 – $84.64 |

| FY2025 revenue | $130M (+202% YoY) |

| Q1 2026 revenue | $64.7M (+755% YoY) |

| FY2025 net loss | $510.4M |

| Cash & investments | ~$3.1 billion |

| Shares outstanding | ~373 million |

What Analyst Ratings Say About IONQ

Read the analyst picture carefully, because it contradicts itself. The consensus rating across roughly 13 analysts is "Strong Buy," which sounds like a green light. Yet the average price target, near $67.64, sits just below where the stock already trades. In plain terms: the same analysts who rate it a strong buy do not, on average, see much upside from today's price, with the consensus figures compiled by data trackers like StockAnalysis as of June 2026. That usually means the price has sprinted ahead of the published models, and the ratings are lagging behind a fast-moving chart. It is a reminder that a "Strong Buy" label and a real margin of safety are not the same thing; here you are getting the label without the cushion.

The other numbers explain the wild ride in IonQ stock price. IONQ carries a beta above 3, meaning it tends to move roughly three times as hard as the broad market in either direction. Short interest has run near 20% of the float, so a fifth of tradable shares are bet against, which can fuel sharp squeezes higher and brutal drops. A single piece of IonQ news — a contract win or a sector headline — can move the quote 10% in a session. This is not a quiet quote you check once a quarter.

The Valuation: Is IonQ Stock Too Expensive?

By every traditional yardstick, IONQ is expensive to the point of absurdity. The bull case concedes the yardsticks are accurate and bets they simply cannot price an option on a market that may be worth trillions.

100x sales, and the peer basket

There is no earnings multiple here, because there are no earnings, so price-to-sales is the rough gauge. On 2025 revenue, IONQ trades near 109 times sales; on a trailing basis some data providers show it above 130. For comparison, a mature software firm might trade at 10 to 15 times sales. IonQ's peers are even more stretched, with Rigetti and D-Wave having traded at multiples several times higher on far smaller revenue. That tells you the market is pricing the whole sector on hope, not cash flow. It also explains why these names move together: quantum stocks have traded as a single basket since late 2023, lifted and dumped as a group by sentiment, and quantum-themed ETFs amplify the swings by buying the whole shelf at once.

The prize the bulls are pricing

So why pay 100 times sales for a company losing half a billion a year? Because of the size of the prize. McKinsey's 2026 quantum technology analysis estimates the technology could create between $1.3 trillion and $2.7 trillion of economic value by 2035, and notes that sector investment hit $12.6 billion in 2025, more than six times the prior year, according to McKinsey. If quantum computing becomes as foundational as the bulls believe, and IonQ stays near the front, today's market cap could look small. That is the entire investment case, and it rests on a payoff a decade out.

The bear's reply is just as simple. A decade is a long time for a technology that still has not delivered a clear commercial killer application, the lead in qubit count and fidelity can shift to a better-funded rival overnight, and a multiple above 100 times sales leaves no room for the stumbles every hard technology hits. You are not buying a discounted cash flow; you are buying a story about 2035, and paying a 2035 price for it today. Whether that is brilliant or reckless depends entirely on a future nobody can yet measure.

| Quantum peer | Price/Sales (approx.) | Market cap (approx.) |

|---|---|---|

| IonQ (IONQ) | ~109x | ~$25.5B |

| Rigetti (RGTI) | several × higher | smaller |

| D-Wave (QBTS) | several × higher | smaller |

Does IonQ Stock Pay a Dividend?

No. IonQ pays no dividend, and it should not. The company is burning cash to fund growth and acquisitions, and every available dollar goes back into research, hardware, and deals. A young, pre-profit technology company paying a dividend would be a warning sign about its priorities. The practical takeaway for an investor is simple: your entire return from IONQ depends on the share price rising. There is no income cushion to soften a bad year, and given the volatility, bad years are part of the deal.

Is IonQ Stock a Buy in 2026? The Verdict

Here is my honest read. IonQ is a serious company with a genuine technology lead and revenue that is growing fast, which already puts it ahead of most of its quantum peers. But it is priced for near-perfection, it dilutes shareholders relentlessly, its headline GAAP profit is an accounting mirage, and it trades as part of a sentiment basket that can halve in weeks. If you buy IonQ stock, buy the multi-year business thesis with money you can leave alone for years, and size it as the volatile speculation it is, not as a core holding. The question to settle before you click buy is whether you are investing in quantum computing or just renting a fast-moving chart.