SMCI Stock: Can You Trust Super Micro Computer on Nasdaq?

Super Micro grew its revenue roughly 2.7 times in two years, and SMCI stock still fell over the past year while rivals Dell and HPE soared. Stranger still, Wall Street's average price target sits below where the shares already trade. A company riding the biggest technology boom in a generation, posting record sales, and the market says hold and the analysts say it is worth less than today's price. That contradiction is the whole story, and it is the part the quote pages never explain. The number that grows here, revenue, is not the number that matters. Two others are: the margin, which collapsed, and the trust, which broke.

What Super Micro Computer Actually Does

Super Micro Computer is the picks-and-shovels supplier of the AI gold rush. It does not design the scarce chips everyone wants. It turns them into the machines that run them, and that single role explains both its explosive growth and its stubbornly thin profits.

AI servers built around Nvidia GPUs

At its core, Super Micro takes Nvidia's GPUs and builds them into complete, high-performance servers and storage systems for artificial intelligence data centers and cloud computing providers. Its edge is speed and customization: it ships new server designs fast, and it was early to direct liquid cooling, the plumbing that keeps dense racks of AI chips from overheating. That makes it a favored partner when a customer needs Nvidia's latest silicon turned into a working system quickly. It also makes the company partly hostage to decisions made in Santa Clara, because when Nvidia controls who gets chips and when, Super Micro's growth rides on that allocation.

A high-volume, thin-margin business

Here is the catch built into the model. Assembling servers is closer to a commodity business than a technology monopoly. Super Micro adds real engineering value, but it competes on price and speed, not on a software moat. The result is a gross margin that has run in the low double digits at best, a fraction of what a chip designer earns. The company also sells storage, server management software, and support services, but the center of gravity is hardware, and hardware at scale is a grind. High revenue does not automatically mean high profit, and SMCI is the clearest example on the market. It is worth sitting with that, because it inverts the usual instinct. Most investors see revenue almost tripling and assume the profits must be following. With a hardware assembler racing to win share, the opposite can happen: chasing volume on big AI contracts often means accepting thinner margins to land the deal, so the faster the top line grows, the more pressure builds on the bottom line.

The San Jose company behind the boom

Super Micro Computer, known to many investors simply as Supermicro, was founded in 1993 and is based in San Jose, California, long before AI made it a household ticker. For most of its life it was a quiet, founder-led maker of efficient server platforms. The AI buildout dragged it into the spotlight, turning a steady technology supplier into one of the most volatile names on the Nasdaq, with all the scrutiny that attention brings. That scrutiny cuts both ways: it powered the share price to extraordinary heights, and it also meant that when questions arose about the company's accounting, they were examined far more harshly than they would have been for a quiet small-cap nobody was watching.

SMCI vs Nvidia: Clearing Up the Confusion

A common search is whether SMCI is better than Nvidia, and the question slightly misreads what each company is. They are not competitors; they are links in the same chain. Nvidia designs the GPUs and earns gross margins above 70%, because almost nobody else can make what it makes. Super Micro buys those chips and builds servers around them, earning a gross margin closer to 8 to 11%, because plenty of firms can do roughly what it does. One sells the scarce ingredient; the other cooks the meal. That difference is why Nvidia is the most valuable company on earth and SMCI stock, despite similar revenue growth rates, trades at a small fraction of the price-to-sales multiple. The market is not being irrational here. It pays up for the part of the chain that is hard to replace and pays down for the part that is not. If you want the AI chip story, you are really talking about Nvidia. SMCI is a leveraged, lower-margin bet on the same demand, with more ways to disappoint and a thinner cushion when it does.

Why SMCI Stock Is in Trouble: Margins and Trust

This is the section every quote page leaves out, and it is the reason the consensus rating is a cautious hold. The growth is real. So are two problems that growth cannot paper over.

The margin collapse

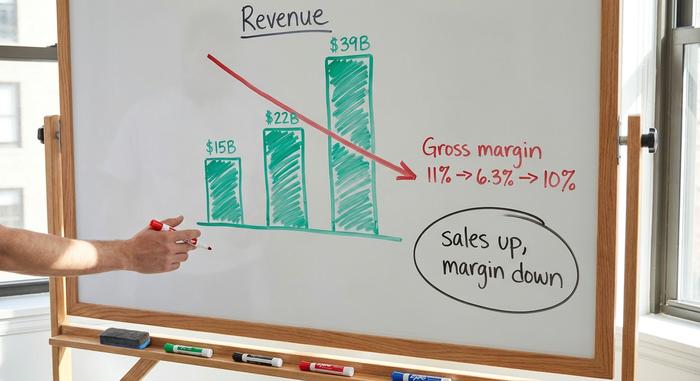

Start with the good news. Fiscal 2025 sales hit about $22 billion, up roughly 47% in a year, and management has guided fiscal 2026 toward $39 to $40 billion. Stunning numbers. Now the bad news. The gross margin, already thin near 11% in fiscal 2025, cratered to about 6.3% in the second quarter of fiscal 2026 before clawing back to around 10% on a non-GAAP basis in the third quarter, when revenue landed near $10.2 billion, per its SEC filing. Read those two facts together. Sales nearly tripling over two years, and the profit that actually reaches shareholders barely moved. A few points of gross margin sound trivial until you multiply them across tens of billions of dollars. At that scale, the drop from 11% to 6% quietly wiped out most of a year's profit while the headlines still shouted growth. Revenue grew. The number that pays shareholders did not. That is the cleanest reason SMCI stock wears a discount even as the AI buildout roars.

The accounting saga, in dates

Then there is trust. Here the timeline does the talking. It opened in August 2024, when short-seller Hindenburg Research published a report alleging accounting problems. Super Micro delayed its annual 10-K. Bad sign. Worse followed on October 24, 2024, when its auditor, Ernst & Young, resigned, as disclosed in an SEC filing. Auditors rarely walk away from a healthy client, and when they do, the market assumes the worst. For a stretch, a Nasdaq delisting looked like a real possibility. Then the company fought back. It hired a new auditor, BDO, and a special committee dug through the issues. The committee found no evidence of fraud, the delayed financials were filed, and Super Micro regained Nasdaq compliance on February 25, 2025, according to Super Micro. So the formal crisis is over. But here is the catch that still bites: BDO signed off with an adverse opinion on the company's internal financial controls. Investors read a qualification like that exactly the way the old disclosure bargain says they will, as information. They price the doubt. And doubt, once it is in the price, fades far slower than it arrived.

Concentration and export scrutiny

Two more risks stack on top. Customer concentration is severe: a single unnamed data center customer accounted for about 27% of revenue in the third quarter of fiscal 2026, so the loss of one buyer could dent a whole quarter. And Super Micro has acknowledged working with Taiwanese authorities to help prevent the illicit diversion of its server technology, a reminder that export-control scrutiny now shadows every AI hardware maker. Neither risk is fatal. Both are the kind that look minor in a boom and obvious in a bust.

SMCI Stock Price and Analyst Ratings

The price action and the analysts flatly disagree, and that gap is the whole trade. As of June 4, 2026, SMCI stock changed hands near $45.72 on heavy daily trading volume, inside a wild 52-week range of $19.48 to $62.36, adjusted for the 10-for-1 split back in October 2024. Lately it has ripped: up more than 50% for the year, over 60% in a single month. Momentum traders love a chart like that. But zoom out and it sours. The stock is still down about 24% over the past year. Dell, in the same window, rose roughly 112%; HPE, about 89%. Same boom, same Nvidia chips, three very different outcomes. When a stock lags this badly during the best stretch ever for AI hardware, the problem is not demand. It is the company itself.

The analysts are not hiding their caution. The consensus is a hold, blended from a mix of buy, hold, and sell calls across roughly 18 desks, and the average price target sits near $37.63, per StockAnalysis as of June 2026. Notice what that means. The target is below the price. On average, the pros see downside from here, not upside. Now add short interest near 15.7% of the float and implied volatility around 84%, and the shape of the thing is clear: a battleground, not a quiet compounder. With that many traders betting against it, every earnings report and every fresh headline can set off a violent squeeze higher or a rout lower. That is the stock you would be buying. Loud, fast, and contested.

| SMCI snapshot (as of June 4, 2026) | Figure |

|---|---|

| Share price | ~$45.72 |

| 52-week range (post-split) | $19.48 – $62.36 |

| Market cap | ~$27.5 billion |

| Forward P/E | ~14–15x |

| Price/Sales | ~0.8x |

| Gross margin | ~8–11% |

| Consensus target | ~$37.63 (downside) |

| Analyst rating | Hold |

Is SMCI Cheap? Valuation vs Dell and HPE

By the numbers, SMCI screens genuinely cheap, and the cheapness is the discount for everything above. It trades around 0.8 times sales and roughly 14 to 15 times forward earnings, with a PEG ratio below one. For a company growing revenue this fast, those are bargain-bin multiples; a typical AI-themed name trades far higher. The catch, again, is that the market is not pricing the growth. It is pricing the margin and the trust.

Set against its closest peers, the gap is stark. Dell and HPE also build AI servers, also run thin hardware margins, and also depend on Nvidia, yet both trade richer and both delivered far better one-year returns. The difference is not the business; it is the baggage. Investors will pay more for a server maker whose books never went through an auditor resignation. That is the price of trust, and Super Micro is still paying it. The cheapness, in other words, is the market doing its job: demanding a discount for risk it can see clearly, rather than a bargain it somehow overlooked. The bull case is that the discount has grown too large; the bear case is that it is exactly right. Both sides can point at the same 0.8 times sales on SMCI stock and tell a completely different story.

| AI server stock | 1-year return (approx.) | Note |

|---|---|---|

| Super Micro (SMCI) | ~−24% | cheapest on sales; trust discount |

| Dell (DELL) | ~+112% | broader franchise, clean books |

| HPE | ~+89% | enterprise base, steadier margins |

Is SMCI Stock a Buy in 2026? The Verdict

Here is my honest read. The growth is real and the stock is genuinely cheap, but cheap is the price of two problems that do not vanish on a good quarter: structurally thin margins, and a governance discount that heals in years, not weeks. The fact that the shares trade above the average analyst target tells you the market is already more hopeful than the people paid to model it. Buying SMCI stock is a bet that margins normalize toward the low double digits and that trust slowly returns as clean filings stack up under the new auditor. The investment case is defensible, but it is a bet, not a sure thing. If you take it, size it for a stock that can swing wildly, and treat the cheap multiple as payment for real risk rather than a gift. For a patient investor who can stomach the volatility and is genuinely convinced the worst is behind the company, that payment may be worth making. For everyone else, a cleaner AI-hardware name is sitting nearby. The question to settle first is simple, and no spreadsheet answers it for you: do you believe the next set of books?