What Is Equity? Equity Meaning and How to Find It

The same one-line subtraction describes the stake you hold in your house, the value sitting in your brokerage account, and a US stock market worth roughly $69 trillion. That number has a name: equity. Strip away the jargon and equity is just what you own minus what you owe. This guide walks that single idea everywhere it shows up: what equity means, the formula behind it, the main types from shares to home equity, how it differs from debt, how investors earn a return on it, and why the number matters.

What equity means: the simple definition

Equity is the value of ownership left once the debts are paid. That is the whole concept. Put another way, equity represents the slice of something that is truly yours and not the lender's. Own a thing outright? Your equity is its full value. Owe money against it? Your equity is whatever survives the claim.

So when someone asks what equity means, the honest answer fits in a line: it is the residual. It is what would actually land in your hands if you sold the asset at its market value and cleared every liability attached to it. A homeowner, a shareholder, and a startup founder all mean the same thing by the word — even though the asset underneath looks nothing alike. The asset changes. The idea never does.

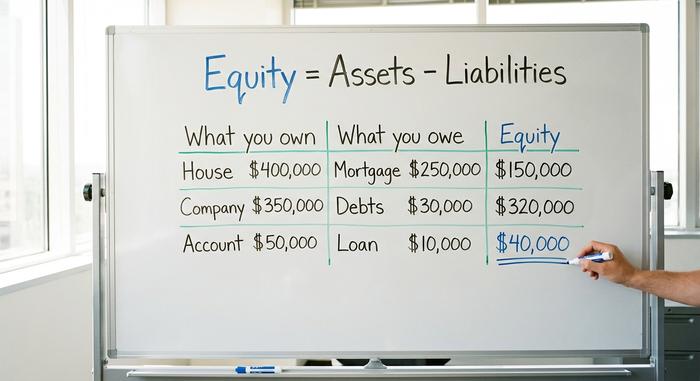

Calculating equity: assets minus liabilities

Here is the formula that holds the whole topic together. Equity equals assets minus liabilities. That is it. Everything else in this article is that one subtraction applied to a different pile of stuff.

The formula on a balance sheet

A company writes this down formally on its balance sheet. Add up everything the business owns, the total assets, then subtract everything it owes, the total liabilities. What remains is shareholder equity, sometimes called stockholders' or owners' equity. If a firm holds $350,000 in total assets and carries $30,000 in liabilities, its equity is $320,000. That figure is the owners' claim, the amount that would be returned to them if the company were liquidated and every debt settled first.

| What you own | Its value | What you owe | Your equity |

|---|---|---|---|

| A house | $400,000 market value | $250,000 mortgage | $150,000 |

| A small company | $350,000 total assets | $30,000 liabilities | $320,000 |

| A brokerage account | $50,000 in holdings | $10,000 margin loan | $40,000 |

Book value versus market value

There is a catch worth knowing early. The equity on a balance sheet is book value, an accounting figure rooted in what assets are recorded as worth. The market often disagrees. A company's stock price reflects what investors will pay for future profits, not what the accountants logged, so the total market value of its shares can sit far above or below book equity. Divide shareholder equity by the number of shares and you get book value per share, a useful floor, but rarely the price the stock actually trades at.

This gap is why a whole market can be worth far more than the assets recorded on its books. Investors are paying for brands, patents, customer loyalty, and expected growth that accounting rules never put on the page. It is also why book value matters most for asset-heavy businesses such as banks, and least for a software company whose real worth lives in things a balance sheet barely captures. Two firms with identical book equity can trade at wildly different prices for exactly this reason.

Negative equity and what it signals

Run the subtraction and the answer can come back below zero. When liabilities exceed total assets, equity is negative, and that is a real warning about financial health. A homeowner is "underwater" when the mortgage is larger than the house is worth. A company with negative equity has promised away more than it owns. Shareholders are still shielded by limited liability, so they cannot be chased for the shortfall, but the equity line going red is rarely a number anyone wants to see.

Types of equity: from shares to home equity

Same formula, different asset. That is the trick to the whole vocabulary. The word equity bolts onto several different things, and each type of equity is just that one subtraction wearing a new outfit.

Shareholder equity, common stock, and preferred stock

Buy a share and you buy a unit of shareholder equity. Most shares are common stock: voting rights, plus a claim on profits through dividends and price growth. Preferred stock is the other flavor. It usually pays a fixed dividend and stands ahead of common shares if the company is wound up, but it tends to give up the vote. Both are ownership. They just sit in different seats.

Where does that equity come from? Two places. Paid-in capital is the cash investors handed over when they bought shares straight from the company. Retained earnings are the profits the business kept and reinvested instead of paying out. Decades of reinvested profit add up fast. A long-established firm often shows a huge equity line built mostly from earnings it never distributed, dwarfing whatever its founders first put in.

Home equity: your stake in your house

Home equity is the version most people meet first. Take the property's market value, subtract the mortgage balance, and the difference is yours. Buy a $400,000 home with $250,000 still owed and you hold $150,000 in home equity. That stake grows two ways: as you pay down the loan, and as prices climb. You can even borrow against it through a home equity line of credit without selling. And the aggregate is staggering. US households held about $34.15 trillion in home equity in the fourth quarter of 2025, north of 70 percent of everything their real estate is worth.

Private equity and brand equity

Two more forms round it out. Private equity is ownership in companies that never list on a public exchange, bought by funds that aim to fix a business up and sell it on. Globally those funds sat on roughly $3.8 trillion in unrealized value across about 32,000 companies in 2025. Brand equity is the strange one. It is the intangible premium a famous name commands beyond the physical assets behind it. No clean formula, but real money all the same. Coca-Cola's name and Apple's logo are worth tens of billions for one reason: people pay more for the same product once it wears the label.

| Type of equity | Where it lives | The rough formula | Real-world scale |

|---|---|---|---|

| Shareholder equity | A company balance sheet | Total assets − total liabilities | US public equity ~$69T (Jan 2026) |

| Home equity | A house | Market value − mortgage | US households $34.15T (Q4 2025) |

| Private equity | Unlisted companies | Owners' stake, not publicly priced | $3.8T unrealized value (2025) |

| Brand equity | A brand's reputation | No fixed formula (intangible) | Priced only when a brand is sold |

Equity vs debt: two ways to fund and own

Every business that needs money hits the same fork, and it lands on our two words. Equity financing means selling a piece of ownership for cash. Nothing to repay, but the slice you sold is gone for good, and the new owners now share the upside and the decisions. Debt means borrowing. You keep all the ownership, but you owe fixed repayments with interest, and the lenders get paid first when things go wrong.

Neither is free. Equity costs you control and a cut of every future profit. Debt costs you cash flow and stacks a liability ahead of you in the queue. The choice comes down to one question: how much dilution can you stomach versus how much repayment can you afford? Picture it. Raise $1 million by selling 20 percent and you have just priced the whole company at $5 million and signed away a fifth of every dollar it will ever make, with nothing to pay back. Borrow the same $1 million and you keep every share, but now you owe the lender on a schedule whether you turn a profit or not. One path gives away the upside. The other has to outrun the downside. Across the whole US market, debt does most of the lifting: companies raised roughly $222.9 billion in equity against $10.4 trillion in debt in 2024, about 47 to one.

Equity as an investment and return on equity

In everyday speech, buying equity means buying stock. What you are really buying is a claim on a company's future profits, and that claim has paid. US equities returned about 9.8 percent a year on average from 1928 through 2025, measured by the S&P 500. That is not a gift. It is the price of risk, the extra reward investors demand for holding stocks instead of safe government bonds. As of January 2026 that premium sat near 4.23 percent, right around its historical norm. An equity investment, in short, is a bet on profit — paid for in volatility.

The reward shows up two ways. Dividends are the slice of profit a company hands back to shareholders. Capital gains are the rise in the stock price as the business grows more valuable. Equity investors have pocketed both across a century of cycles. And the premium exists for a blunt reason: equity holders are last in line. If a company fails, lenders and bondholders get paid first; shareholders split whatever is left, which is often nothing. That risk is precisely what the extra return buys.

So how hard is a company's equity working? Return on equity answers it. ROE divides annual profit by shareholder equity. Earn $20 million on $100 million of equity and you post a 20 percent ROE, meaning every dollar of ownership threw off twenty cents of profit that year. Investors lean on the number to compare firms, because a high, durable ROE says management is turning the owners' stake into real earnings rather than letting it sit.

Why equity matters: financial health at scale

Equity is the scoreboard of ownership, and people read it at every size. A lender checks a household's home equity before extending more credit. An analyst watches the debt-to-equity ratio, which weighs what a company owes against what its owners hold, as a quick gauge of risk; the more debt stacked on a thin slice of equity, the more fragile the firm. Equity used this way is less a single fact than a lens on financial health.

Zoom out, and equity markets put that same lens over entire economies. The world's listed companies were worth about $151.94 trillion in equity at the end of 2025, up more than 18 percent in a single year. Set the big equity pools side by side and each one rivals a national economy.

| Equity pool | Size | As of | Source |

|---|---|---|---|

| Global stock market cap | $151.94 trillion | End 2025 | World Federation of Exchanges |

| US stock market cap | $69.0 trillion | Jan 2026 | Siblis Research |

| US household home equity | $34.15 trillion | Q4 2025 | Federal Reserve |

| Global private-equity unrealized value | $3.8 trillion | 2025 | Bain & Company |

Examples of equity in everyday life

Translate the headlines back to the formula and they stop being intimidating. A neighbor with a paid-down house has equity equal to the home's value minus what is left on the mortgage. A founder offered "5 percent equity" is being handed five percent of the ownership, and whatever it is worth depends entirely on the company's value. "$100k in equity" in a home means the house would clear $100,000 after the loan is repaid. A 401(k) or brokerage account full of stock is a stack of small equity stakes in real businesses. Same subtraction, every time.

What to remember about the word equity

What I keep coming back to is how much ground one subtraction covers. Once you read equity as "what is left after the debts," the word stops being intimidating and starts being arithmetic. A market cap, a home value, a cap-table slice, a balance-sheet line: each one is the same subtraction pointed at a different asset. So the next time a number lands in front of you labeled equity, do not take it on faith. Ask what is owned, ask what is owed, and do the subtraction yourself.