Debt Consolidation Options: Calculator for Credit Card Debt

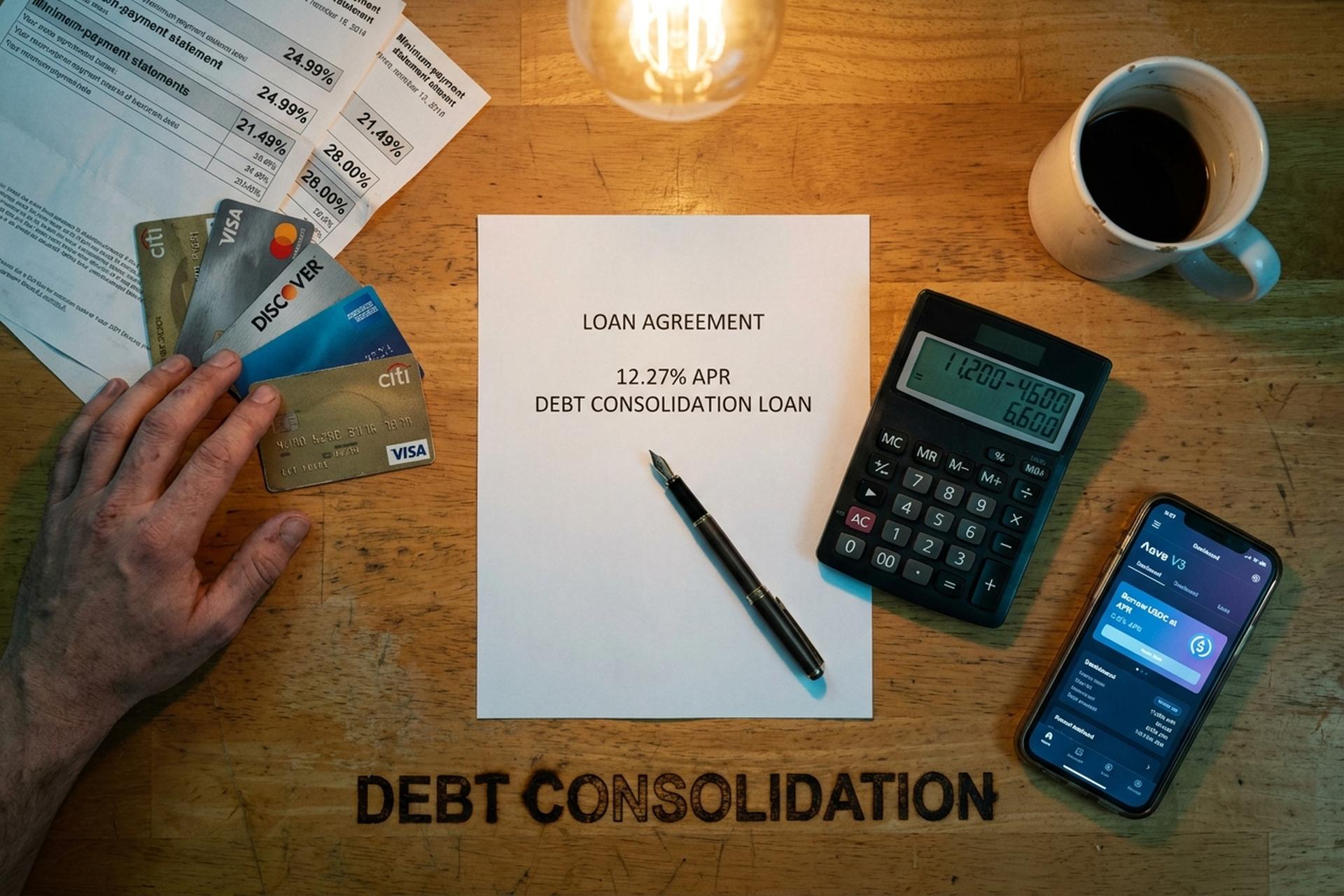

A bartender in Phoenix had three credit cards and a couple of car loans last June. Card one: $4,200 at 24.99%. Card two: $6,800 at 21.49%. Card three: $2,400 at 28%. Roughly $310 a month vanished into minimum payments and almost none of it touched the principal. By February of 2026 she'd rolled all three balances and her car loans into one consolidation loan at 12.27% APR, combining multiple debts into one payment, and her monthly outflow dropped to $185. That spread, the gap between the average revolving credit card APR and what a consolidation loan actually costs, is the entire reason debt consolidation became a top-search money topic in 2026.

This guide walks through what debt consolidation is and how to consolidate your debt, the calculator math that decides whether it's worth doing, the menu of debt consolidation options to pay off your debt and get out of debt, and the newer crypto and DeFi rails that compete with the traditional refinance, personal-loan, and balance transfer credit playbook. We'll cover personal loan vs balance transfer vs HELOC vs debt management plan vs settlement vs bankruptcy, the credit score impact each carries, and where Aave, Nexo, Ledn, USDC and stablecoin borrowing actually fit (and don't) when the goal is paying off credit card debt without making things worse.

What Is a Debt Consolidation Loan and How It Works

Debt consolidation combines multiple debts into a single new loan or new credit card account, ideally at a lower interest rate. Taking out a loan to consolidate means you use one loan to pay off your existing balances, and from there you owe one lender instead of juggling four or five, with one monthly payment instead of several. The math only works if the new loan carries a meaningfully lower APR than the weighted average of your existing debt. That's where the savings actually come from: a lower interest rate. Bundling multiple debts into a single account reduces the amount of interest you pay over time.

A debt consolidation loan is the most common version. A bank or credit union, or a fintech that offers debt consolidation loans, writes you a fresh loan. You take the proceeds, you pay off credit card balances at each issuer, and now you owe the bank instead of the credit card companies. The monthly payment lands on a fixed schedule (usually two to seven years) at a fixed rate that doesn't drift the way a card's APR can. Loan payment amounts stay predictable for the life of the loan. A single new loan could cut total interest paid by thousands. Credit unions, online lenders, and most major banks offer debt consolidation loans now, and interest over time depends mostly on your credit profile.

Why does this product even exist? The spread between average interest on cards and a personal loan is enormous. The Federal Reserve's G.19 release pegs the average APR on credit-card accounts accruing interest at 21.52% in early 2026, and LendingTree's tracker of new-card offers averages 23.75%, climbing as high as 27.40% for thinner credit profiles. Bankrate's April 22, 2026 personal-loan survey puts the average personal loan APR for a 700 FICO borrower at 12.27%. Roughly half the cost of revolving on the average credit card. Stretch that gap over a $15,000 balance for four years and you're looking at four-figure savings even after origination fees. The right loan to pay off high-interest credit will reduce your interest rate and pay down your balance debt faster.

When to Consolidate Debt: Credit Score and Debt Amount

Not everyone benefits from consolidating. It works when three things line up: the new APR is meaningfully below the weighted average of what you owe today, you have steady income to actually repay the debt on schedule, and you've fixed the spending behavior that created the debt in the first place. Skip that third one and you'll be back here next year, just with bigger numbers.

Credit score is the hinge. North of 740 FICO, you can realistically grab a personal loan at 6-9% from credit unions and prime-tier fintechs. Between 670 and 739, you're looking at 12-18%, still better than cards but with less upside. Below 670, you're often staring at 25-36%, which can be worse than the cards you wanted to consolidate. For the "good credit" tier (690-719) NerdWallet pegs the April 2026 average personal loan rate at 14.48%. Still a solid drop from 22% on a card.

Debt amount matters too. Under about $5,000, the origination fees and time spent applying often eat the savings, and the smaller amount of debt may not justify combining multiple balances at all. Over $50,000, lenders get pickier and tend to push you toward a HELOC or debt-management plan. The sweet spot for an unsecured debt consolidation loan: roughly $5,000 to $40,000 of high-interest credit card balances. Discover's own example walks through a $15,000 consolidation loan at 11.99% APR for 72 months running about $293 a month. Cleanly inside what a personal loan handles well.

One quick filter. If your debt-to-income ratio is above 50%, no consolidation lender will approve you on decent terms; a DMP or settlement is the realistic path. Under 35%, you have leverage to shop around and let lenders compete.

Debt Consolidation Options: Personal Loan vs Balance Transfer

The mainstream consolidation menu has six items. They differ on who lends, how much they lend, what collateral they want, and what happens to your credit score on the way through.

| Method | Typical APR (2026) | Setup cost | Best for | Downside |

|---|---|---|---|---|

| Personal loan | 12.27% avg (700 FICO); 6-36% range | 1-9.99% origination | $5K-$40K of unsecured debt, steady income | Subprime borrowers pay 25-36% |

| Balance transfer card | 0% intro 12-21 mo, then 20%+ | 3-5% transfer fee | Smaller balances payable in 12-21 months | Reverts to high APR after promo |

| Home equity loan / HELOC | 7.09-7.37% avg | Closing fees $750-$6,685 | Homeowners with $30K+ equity | Your house is the collateral |

| Debt management plan (DMP) | ~8% (creditor concession) | $37 setup, $26/month | Steady income, multiple cards | 3-5 years of strict budget |

| Debt settlement | N/A (negotiated 50% reductions) | 15-25% of enrolled debt | Severe hardship, can't repay full | Tanks credit score, taxes due on forgiven amount |

| Crypto-backed loan | 2.9-11.5% (Nexo, Ledn) | Variable; zero-fee on some platforms | Borrowers holding BTC/ETH/stablecoin | Liquidation risk on collateral |

A personal loan delivers a fixed payoff schedule. A balance transfer card gives you a window. The longest current 0% balance-transfer offers run 21 months (Wells Fargo Reflect, Citi Simplicity), with the average sitting at about 13.05 months per Bankrate, plus a 3-5% transfer fee. If you can clear the balance inside the promo, balance transfer beats almost everything. If you can't, the post-promo rate snaps back to 20%+ and erases the savings.

A home equity loan or line of credit averages 7.09% on a HELOC and 7.37% on a fixed-rate equity loan. Cheaper than any unsecured option. The risk is that if you default, the lender forecloses on your house, a trade-off worth thinking very hard about before signing.

Debt Consolidation Calculator: Use Our Debt Consolidation

A debt consolidation calculator answers one specific question: will the new loan actually save money against your current debt amount, the existing debt, the interest rate stack, the total amount of your debt? Use our debt consolidation framework as a starting point, or grab any reputable online tool from Discover, Bankrate, or NerdWallet. Feed it three inputs per existing debt (balance, APR, monthly payment), plus the new loan APR and term.

A debt consolidation loan calculator runs that math and spits out two numbers: the new monthly payment ("see what your monthly payment would be") and the total interest paid over the life of the loan. There's a trick most borrowers miss. Stretching the repayment term lowers the monthly payment but cranks up total interest. A four-year loan beats a seven-year one on total cost, every time, even if seven years feels easier each month.

Worked example, with our Phoenix bartender. Three card balances: $4,200 at 24.99%, $6,800 at 21.49%, $2,400 at 28%. Total $13,400, weighted average roughly 23.5%. Roll into a 60-month loan at 12.27%. New monthly payment lands around $300, versus $310 in minimums today. Total interest paid over the life of the loan: about $4,600, versus an estimated $11,200 if she'd just kept paying minimums on the cards. May pay more in interest if you stretch the term too long, so balance term against payment. That's the math behind the whole consolidation pitch. Savings come from a lower interest rate, not from consolidation itself.

A calculator won't tell you three things. One: origination fees of 1-9.99% come off the principal at funding, so a "$13,400 loan" might mean $12,800 actually arrives in your account. Two: applying for new credit may hurt your credit slightly. Your score might drop 5-10 points temporarily from the hard inquiry and the new credit account showing up on the report. Three: if you keep swiping the original cards after consolidating, you stack new debt to pay on top of what you already owe. Consolidating my credit card debt only worked when the cards actually stopped getting used.

Each Type of Consolidation: HELOC, DMP, and Settlement

These three less-common paths each have a specific shape, and matching the type of consolidation to your situation is most of the decision.

Home equity loan or HELOC. A home equity loan hands you a lump sum at a fixed rate, with Bankrate pegging the national average at 7.37% on April 22, 2026. A HELOC operates more like a line of credit secured by the equity in your home, currently averaging 7.09%. Both turn unsecured card debt into secured mortgage-style debt. Closing costs land between $750 and $6,685. The payoff math is great. The risk math is awful. Lose income, can't repay, and the bank takes the house. If you have a stable W-2 and a chunk of equity, it's often the cheapest legal option. If you're self-employed or commission-based, the variability of income makes this dangerous in a way most lenders don't warn you about.

Debt management plan (DMP). Here a nonprofit credit counseling agency (NFCC-affiliated nonprofit credit counselors are the standard) does the negotiation work for you. It calls each card issuer, gets the rates dropped (often to around 8%), and rolls your monthly debt payments into a single monthly payment that goes to the agency. The agency pays each creditor on your behalf. Among formal options for credit counseling, this is usually the cheapest by a wide margin. The numbers: about $37 one-time to set up, about $26 a month after that. It runs three to five years. You're not borrowing anything new. You're just riding out the existing debt at much lower rates. The trade-off is that most cards in the program have to be closed, which hurts your credit utilization for a while.

Debt settlement. A for-profit firm negotiates with each creditor to accept partial repayment, typically aiming for around 50% of the original balance. Fees on the program: 15-25% of enrolled debt. Once those fees come out, the borrower keeps roughly 30% in real savings. Three big problems with this route: your credit score gets crushed for years, the IRS treats forgiven debt above $600 as taxable income (surprise tax bill in April), and the FTC's Telemarketing Sales Rule blocks any settlement company from collecting fees before settling at least one of your debts. National Debt Relief, the biggest US settlement firm, has helped 1.3 million-plus people, but the typical program runs 24-48 months. Last-resort tool. Don't reach for it first.

Bankruptcy. When nothing else works. The US Courts release on February 4, 2026 reported 574,314 filings in calendar 2025, an 11% jump from 2024. Chapter 7 (liquidation) was 356,724 of those, up 14.8%. Chapter 13 (court-supervised repayment plan) was 207,889. A Chapter 7 erases most unsecured debt within months, but it stays on credit reports for ten years. Chapter 13 builds a 3-5 year repayment plan that you complete under court supervision, and it sticks to your credit for seven years. Both are heavy. Filing fees plus attorney costs run thousands. And you don't always qualify: the means test screens higher-income filers out of Chapter 7 entirely.

Crypto-Backed Loans and Stablecoin Refinancing

This is the genuinely new chapter. Drop BTC, ETH, or a similar asset as collateral on a lending platform. Borrow stablecoins (USDC, USDT) against it at whatever loan-to-value ratio (LTV) the platform allows. Use those stablecoins to clear your high-interest cards. You keep upside if the crypto rises, and you don't sell, so most jurisdictions don't tax it as a capital-gains event.

Centralized crypto lenders are the easy on-ramp. Nexo lists rates starting at 2.9% APR, up to 50% LTV on Bitcoin and Ethereum (90% on stablecoins, tiered to NEXO loyalty). Ledn sits in the 9.99-11.49% APR band on Bitcoin-backed loans, maxes at 50% LTV, funds in roughly 24 hours. Both KYC. Both publish reserve attestations. Both rode out 2022 while BlockFi, Celsius, and Voyager went down.

Now the math. Say you have $20,000 of BTC sitting in cold storage. Pledge it as collateral, pull $10,000 of USDC at 8% APR, use that to wipe a $10,000 card balance at 24% APR. Your interest cost falls from about $200 a month to roughly $67. The BTC keeps its upside if price rises. The catch is the LTV. Drop 30% in BTC, and the platform either calls for more collateral, expects partial repayment, or sells some of your BTC at the worst possible price. Anyone who tried this just before October 2025 felt it: a single-day liquidation cascade wiped out about $19 billion of leveraged positions. Hit twice — cards they'd tried to escape from, collateral they'd just pledged.

The 2022 wreckage is the context you can't skip. Terra/Luna torched $50 billion in three days back in May 2022, and that took Celsius and Three Arrows down with it. FTX went bankrupt in November 2022, exposed an $8 billion customer-funds gap, froze BlockFi, Genesis, and Voyager. The SEC v. BlockFi consent decree (February 2022, $100M settlement) was the first formal ruling that retail-facing crypto-interest products were unregistered securities. The takeaway is short: stick with collateralized loans (you keep visibility on the asset), favor platforms with transparent audited reserves, watch the LTV, and never pledge more crypto than you'd be okay losing to a flash crash.

DeFi Lending: Aave, Compound, and Stablecoin Borrowing

DeFi takes the same idea on-chain and removes the centralized intermediary. Aave V3 is the largest DeFi lending protocol, with TVL above $26 billion as of mid-April 2026 across 14+ networks (briefly dropping to ~$20 billion during the KelpDAO incident on April 18). Compound is the second-largest. MakerDAO (now branded Sky) is the third, with its DAI/USDS stablecoin used as a borrow asset across the lending market.

DefiLlama's lending dashboard shows roughly $52 billion total parked in DeFi lending protocols as of April 2026. Galaxy Research clocked Q3 2025 crypto-collateralized borrowing at a record $73.6 billion, with DeFi lending alone up 55% year-over-year to $41 billion. This is no longer a small experiment.

Aave USDC borrow rates run typically 3-8% during normal market conditions. They can spike above 15% when stablecoin demand outstrips supply (after a deleveraging event, for example, when traders want to repay loans and dollar-pegged stables get scarce). The mechanics: connect a self-custody wallet, deposit ETH or wstETH or another supported collateral, set the borrow amount within your health factor limits, and the protocol mints USDC into your wallet. From there you swap to fiat through a centralized exchange, withdraw to a US bank, and pay off a credit card.

DeFi has three advantages over centralized lenders. No KYC (in most cases). No platform-risk overhead — your collateral sits in a smart contract you control, not on a company's balance sheet. Fully transparent rates and liquidations, on-chain in real time. The disadvantages are real too. Smart-contract risk (audits help but don't eliminate it). Wallet-management risk (lose your seed phrase, lose your collateral). Gas fees that can wipe out savings on smaller positions, especially on Ethereum mainnet (cheaper on Base, Arbitrum, or Polygon). And the same liquidation cascades that hit centralized loans hit DeFi twice as fast, because liquidation bots run automatically the moment the health factor breaks.

For most consumer borrowers consolidating credit card debt, a CeFi platform like Nexo or Ledn is more practical than DeFi. For crypto-native users with self-custody habits, Aave on Base or Arbitrum is the cheapest collateralized loan available anywhere.

How to Repay the Debt and Boost Your Credit Score

Getting consolidated is the easy step. Actually repaying the debt and not sliding back is harder. A few rules separate the success stories from the people who end up a year later with the original card debt plus a fresh consolidation loan.

Rule one: freeze the old cards. Don't close them all immediately, since closing reduces total available credit and tanks your utilization ratio. Lock them in a drawer or freeze them in the issuer app instead. Once the consolidation loan disburses and the cards are paid off, that newly available credit becomes a temptation. The case-study data from credit counseling agencies is harsh: borrowers who keep swiping the cards while paying down the consolidation loan typically double their debt within nine months.

Rule two: automate the new payment. Set up autopay for at least the minimum on the consolidation loan. Even better, set it up for an extra $50-$200 above minimum each month. The point is to remove the decision. Behavioral economics beats financial math here.

Rule three: watch the credit-score curve, but don't read too much into the early dip. A new account knocks 5-10 points off in the first 60-90 days from the hard inquiry and the drop in average account age. Once on-time payments start showing up, the score climbs 20-50 points over six to nine months as utilization on the closed cards drops toward zero. After 18-24 months of clean debt repayment, most borrowers land 50-100 points above where they started. It's a U-curve, not a straight line. Expect the dip.

What hurts your credit score most? Missing a payment on the consolidation loan (one miss can knock 60-110 points off), running balances back up on the original cards, applying for new credit during the repayment window. What helps? Paying on time, every time. Pushing utilization on the consolidated cards under 10%. Not opening anything else for at least a year.

Risks: Volatility, Liquidation, and BlockFi Lessons

A few warnings worth saying out loud. Debt consolidation does not reduce debt. It restructures it. The borrower still owes roughly the same amount; the rate is lower, the schedule is fixed, and the path to zero is clearer. None of that means the underlying spending pattern has been fixed.

Three specific risks bear flagging. The first is the "consolidate then re-borrow" trap. About a third of borrowers who consolidate credit card debt run the cards back up within 18 months, ending up with double the original debt. The cure is behavioral, not financial.

The second is variable-rate exposure. HELOCs are usually variable-rate. If the Fed hikes (and the Fed hiked twice in 2025), your HELOC rate climbs. A debt that looked cheap at 7% can be uncomfortable at 9.5% if you're on a tight budget.

The third is crypto liquidation. Anyone using BTC or ETH as collateral for a consolidation loan is exposed to a flash-crash margin call. The October 2025 cascade liquidated $19 billion in long positions in a single day. Combine that with a fixed credit card payment cycle and the worst-case scenario is losing both the crypto and still owing the card. Use conservative LTV (under 40%), keep buffer collateral, and never pledge more crypto than you can afford to lose entirely.

The 2022 BlockFi case sets the regulatory floor. The $100 million SEC settlement (split $50M federal, $50M to 32 states) ruled retail crypto interest accounts to be unregistered securities. Any consumer signing up for a "yield" account in 2026 should assume the SEC will scrutinize it. Centralized lenders that survived (Nexo, Ledn) have generally moved to fully collateralized loan products and away from interest-bearing deposits to dodge that precedent. EU readers operate inside MiCA, which has been fully applicable since December 30, 2024 with grandfathering for legacy crypto-asset service providers running until July 1, 2026. The rules are tighter, but enforcement is more predictable.