BTDR Stock: Bitdeer Technologies Group on Nasdaq

Most pages about BTDR stock show you a price, a chart, and a "buy or sell" button, and tell you almost nothing about the company underneath. That is a problem, because Bitdeer Technologies Group is one of the harder stocks to understand on the Nasdaq. It is the second-largest Bitcoin miner in the world by computing power. It is the only public miner that designs and builds its own chips. And despite both of those facts, it trades for a fraction of what its peers are worth. This article explains what Bitdeer actually does, what the numbers say, and whether that discount is a bargain or a warning.

What does Bitdeer Technologies Group do?

Let me start with the question most investors should ask first, because the price pages never answer it: what are you actually buying? Bitdeer is not a single business. It is four of them stacked together, which is exactly why the market struggles to put a clean value on the stock.

The company is headquartered in Singapore and runs proprietary mining datacenters across the United States, Norway, Bhutan, and Alberta. Its controlling shareholder is Jihan Wu, who owns roughly 25% and who co-founded Bitmain, the largest mining-hardware maker on the planet. That detail matters more than it looks, and I will come back to it.

Self-mining and cloud hash rate

The first business is self-mining. Bitdeer runs its own machines and keeps the Bitcoin they generate. As of April 2026 its average self-mining hashrate was about 65.1 EH/s, up roughly 466% in a year, which makes it the second-largest public miner behind Marathon. In the first quarter of 2026 it mined 2,033 BTC but held only 31 on its balance sheet, a sign that Bitdeer sells almost everything it mines to fund growth rather than sitting on a Bitcoin treasury like some rivals do. The second business is cloud hash rate and hosting. Instead of only mining for itself, Bitdeer rents out compute and rack space to other people through hash rate sharing and one-stop hosting plans. That turns its datacenters into a platform, not just a mine.

The datacenter and HPC footprint

Underneath both sits the thing that actually has value: power. Bitdeer controls about 3,003.5 MW of total power capacity, with around 1,744 MW energized and the rest in the pipeline. Only about 58% of that capacity is switched on today, which means a meaningful part of Bitdeer's value is a promise to build rather than a plant already humming. Secured, grid-connected power at that scale is scarce, and it is the same asset that the artificial intelligence buildout is desperate for. Bitdeer wants to point some of it at high-performance computing rather than only at Bitcoin. The strategy is sound. The delivery, as we will see, is further behind than the headlines suggest.

SEALMINER and the BTDR stock moat

Here is the single most important fact about BTDR stock that a quote page will never tell you. Bitdeer does not buy its mining rigs from Bitmain or MicroBT like everyone else. It designs and manufactures its own chips, under the SEALMINER brand. That vertical integration is a real competitive moat, and almost no other public miner has it.

The SEALMINER chip roadmap

A mining chip lives or dies on efficiency, measured in joules per terahash, or J/TH. Lower is better, because electricity is a miner's biggest cost. Bitdeer's SEALMINER A4 Ultra Hydro, launched on April 7, 2026, runs at 9.45 J/TH and 886 TH/s per unit, a new efficiency record for the company. The A4 Pro sits at 10.9 J/TH. The next-generation SEAL04 chip is targeting 6 to 7 J/TH, with mass production planned for the third quarter of 2026. Each step down in J/TH means more Bitcoin mined per dollar of power, and Bitdeer controls that roadmap itself rather than waiting in line for a supplier.

Selling chips versus using them

The chips are also a second revenue engine. Bitdeer sells SEALMINER hardware to third parties, and those sales reached $23.4 million in the fourth quarter of 2025, up about 105% from the quarter before. That puts Bitdeer in direct competition with Bitmain, the company Jihan Wu helped build. Owning the chip design also means Bitdeer is not exposed to the supply shortages and price spikes that hit miners who depend on a third party's order book. When demand for efficient machines surges, Bitdeer can ship to itself first and sell the surplus to everyone else. A miner that can sell shovels during a gold rush, and undercut the incumbent shovel-maker on efficiency, is a different animal entirely from a company that only digs. Whether the market gives it credit for that is another matter.

BTDR stock price, market cap and key data

The stock has already had a strong year. BTDR trades around $19.63 as of June 4, 2026, up roughly 75% year to date, inside a wide 52-week range of $6.92 to $27.80. It is a high-beta name, swinging more than twice as hard as the broad market, and it has no earnings to value it on. You are paying for growth and for the chip story — not for profit.

| BTDR key data | Figure (as of June 4, 2026) |

|---|---|

| Stock price | ~$19.63 |

| 52-week range | $6.92 – $27.80 |

| Market cap | ~$4.78 billion |

| Shares outstanding | ~243.3 million |

| Beta | 2.45 |

| P/E ratio | n/a (no positive earnings) |

| Dividend | None |

The figures come from stockanalysis.com's BTDR page and move daily. The beta of 2.45 is the number to respect here: this stock can fall as fast as it rises, and it has done both inside the last year. The 75% year-to-date gain also masks a bumpy path, with the shares round-tripping large swings along the way, which is what a beta above two feels like in a real portfolio.

BTDR stock and the revenue-vs-margin gap

Revenue is growing at a pace very few companies can match, and that is the bull's favorite chart for BTDR stock. Trailing twelve-month revenue hit about $739 million, up 146%. First-quarter 2026 revenue was $188.9 million, up 169% from a year earlier, according to Bitdeer's Q1 2026 results. Full-year 2025 revenue came in near $620 million. The climb was steady rather than a single spike, rising quarter by quarter through 2025, from roughly $70 million in the first quarter to $224.8 million in the fourth.

So far, so good. Now the part the growth headline hides. That same first quarter produced a gross loss of $39 million, a gross margin of negative 20.7%. The business is selling more than ever and still losing money before overhead even enters the picture, because the April 2024 halving cut miner rewards in half and the cost of hashing did not fall as fast. The reported net loss of $159.5 million looks alarming, but most of it is a non-cash accounting charge on the fair value of derivatives, not real money leaving the building. Adjusted EBITDA was actually positive at $14.4 million. The honest read sits between the two: the cash bleed is smaller than the GAAP loss, but the negative gross margin is real — and that is the number I would watch every quarter.

The bull case for BTDR stock investors

The bull case for BTDR stock is simple to state. Bitdeer is the highest-quality mining business trading at the lowest price among the majors. It has the second-biggest hashrate, the only in-house chip program, and a $4.78 billion market cap that looks tiny next to peers with less computing power. If SEALMINER keeps cutting J/TH and even part of the AI datacenter plan lands, the room to re-rate toward its peers is large.

There is also a margin-of-safety argument in the chip business. Even when Bitcoin's price is flat, selling efficient hardware to other miners brings in cash that pure miners do not have. Bitdeer holds about $297.7 million in cash to fund the build, and analyst sentiment leans bullish. On the multiples, the stock trades near 7.5 times sales and about 5.3 times book value, which is rich in absolute terms but unremarkable for a company growing revenue at triple-digit rates. For an investor who believes the moat compounds, the discount looks like an opportunity rather than a verdict. The catch is that the market may be discounting it for good reasons, which is where the bear case earns its hearing.

Analyst ratings and the bear case for BTDR

Analysts are mostly positive on the stock, but a price target is not a risk assessment, and the risks here are concrete. The first is debt. Bitdeer has raised money through three convertible note offerings in under a year: $300 million in June 2025, $400 million in November 2025, and $325 million in February 2026, leaving roughly $1.9 billion in total debt. The company used capped calls to limit dilution, which helps, but convertibles still convert, and that overhang is real. Servicing the debt is cheap for now, with coupons between 4% and 5%, yet the notes mature in 2031 and 2032, and refinancing $1.9 billion becomes a very different conversation if Bitcoin is in a downturn when the bill arrives.

The second risk is the gap between the AI story and the AI revenue. Bitdeer talks up high-performance computing constantly, yet actual AI revenue in the first quarter of 2026 was only $3.7 million, against management's claim of a run-rate above $69 million annualized. The Tydal site in Norway, a 180 MW conversion targeting completion in December 2026, is the real catalyst to watch, not the press releases. A third, quieter drag is that Bitdeer is a Singapore-based foreign issuer, and US investors tend to apply a discount to those.

| Firm | Rating | Price target |

|---|---|---|

| Rosenblatt | Buy | $25 |

| B. Riley | Buy | $23 |

| KBW | Hold | $17 |

| Cantor | Hold | $15 |

| Consensus (11-13 analysts) | Buy lean | ~$21.52 – $24.50 |

The spread, from $14 at the low to $40 at the high, per MarketBeat's analyst data, tells you how unsettled this name is.

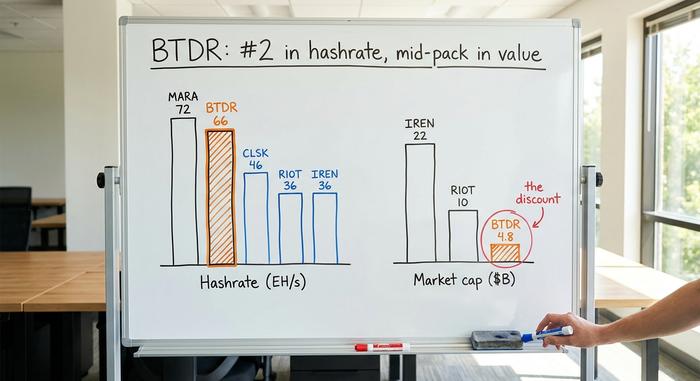

How BTDR stock compares to other miners

This is where the BTDR stock discount becomes impossible to miss. On raw computing power, Bitdeer is near the top of the public miners. On market value, it sits mid-pack. Something does not add up, and both the bull and the bear point to this same table to make opposite arguments.

| Miner (2026) | Hashrate | Market cap |

|---|---|---|

| MARA | 72.2 EH/s | ~$10B+ |

| Bitdeer (BTDR) | 65.5 EH/s | ~$4.78B |

| CleanSpark (CLSK) | 46.2 EH/s | mid-cap |

| Riot (RIOT) | 36.4 EH/s | ~$10.4B |

| IREN | 36.0 EH/s | ~$22.1B |

Sources: bitcoinminingstock.io and company filings. Look at IREN: barely half of Bitdeer's hashrate, roughly four times the market cap, because the market already pays IREN for its AI datacenter pivot. The bull says Bitdeer should close that gap as its own HPC and chip stories mature. The bear says the gap reflects Bitdeer's debt, its thinner margins, and its foreign-issuer status, and that those things are not going away soon. Marathon is the other tell: barely more hashrate than Bitdeer, yet more than twice the market value, helped by being a US-domiciled, index-eligible name. Plumbing and geography move these valuations as much as machines do. Both camps are looking at the same numbers and reaching honest, opposite conclusions.

Is BTDR stock a good investment in 2026?

I will give a verdict rather than a shrug. BTDR is the most interesting Bitcoin-mining stock on the market and also one of the riskiest. You are buying the best hardware, the second-largest hashrate, and a real chip moat, at the cheapest valuation of the big miners. You are also buying $1.9 billion of debt, a negative gross margin, and an AI story running well ahead of its revenue. For an investor who believes the SEALMINER advantage compounds and the Norway buildout lands, the discount is the whole appeal. For everyone else, the question to settle first is simple: do you trust the chips to outrun the debt?